It's been a curious sort of year for investors in Rockwell Automation (ROK +1.08%). As the year has progressed, management has been lowering sales and earnings expectations on the back of a worsening economic outlook, and meanwhile the stock is up nearly 18% as I write -- significantly outperforming the S&P 500 and its peers. What's going on, and is the stock still a good value?

Rockwell Automation's 2016 so far

The following table shows how management has lowered full-year 2016 guidance through the calendar year. The current forecast for organic sales to decline 4% is at the bottom of the original range given in November 2015. Meanwhile, the midpoint of adjusted full-year EPS guidance has been reduced by 4% to $5.90 from $6.15 at the start of the fiscal year.

| Metric |

Q4 2015 |

Q1 2016 |

Q2 2016 |

Q3 2016 |

|---|---|---|---|---|

|

Sales (billions) | $6 | $5.90 | $5.90 | $5.85 |

|

Organic growth |

(4%) to 0 |

(5%) to (1%) |

(4.5%) to (1.5%) | (4%) |

|

Adjusted EPS |

$5.90 to $6.40 |

$5.70 to $6.20 |

$5.75 to $6.15 |

$5.80 to $6.00 |

DATA SOURCE: ROCKWELL INTERNATIONAL PRESENTATIONS.

However, the market has been in forgiving mode. In fact, Rockwell has outperformed industrial peers such as General Electric Company (GE +1.04%) and Emerson Electric (EMR +2.29%). General Electric Company is a useful comparison because CEO Jeff Immelt recently guided investors toward the company's hitting the bottom end of its full-year organic growth guidance for 2% to 4%. In a similar outcome, Rockwell's organic sales are now expected to be near the bottom end of its original guidance -- the difference is that Rockwell's stock has massively outperformed General Electric's in 2016.

In common with General Electric Company and Rockwell Automation, Emerson Electric -- a company often seen as a potential suitor for Rockwell -- has disappointed the market with oil and gas-derived revenue in 2016. Here again, Rockwell's stock outperformance has been notable.

Why Rockwell Automation outperformed in 2016

I see three possible reasons:

- Rockwell's attractive valuation provided a significant margin of safety for any disappointment.

- At the start of the year, many analysts were overly bearish on the automotive sector, and Rockwell, along with other industrial stocks with automobile exposure, was possibly oversold.

- Investors may have accepted near- to mid-term cyclical weakness and sought out stocks with long-term secular growth prospects, such as Rockwell with its Industrial Internet of Things (IIoT) exposure.

Rockwell's IIoT exposure, primarily through its sensors and controls, still remains in place. Indeed, peers such as General Electric Company have increased their IIoT investments in the face of a moderately growing economy.

THE AUTOMOTIVE END MARKET HAS BEEN A GOOD ONE FOR ROCKWELL AUTOMATION IN 2016. IMAGE SOURCE: GETTY IMAGES.

As for the automotive exposure, there was no shortage of analysts calling a cyclical top in the sector, but it carries on performing. Indeed, on Rockwell's third-quarter earnings call, CFO Ted Crandall disclosed that Rockwell's auto growth was 3% in the second quarter and 1% in the third quarter, and the fourth quarter is expected to be good, too. It's all a far cry from the doom and gloom many thought would envelop the industry in 2016.

Rockwell Automation's stock valuation

However, the company's valuation deserves close analysis. It's still relatively cheap when compared with other cyclically aligned industrial companies. I'm using enterprise value (market cap plus net debt) over free cash flow (FCF) as a valuation metric to reflect upon how good Rockwell is at cash conversion.

ROK EV to Free Cash Flow (TTM) data by YCharts.

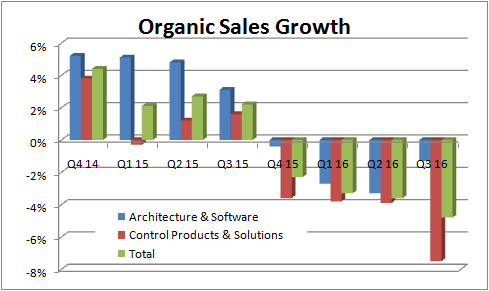

However, the problem is that its sales, earnings, and cash flow are deteriorating. For example, here's a look at total and segmental organic sales growth. It shows no sign yet of bottoming out.

DATA SOURCE: ROCKWELL INTERNATIONAL PRESENTATIONS. YEAR ON YEAR GROWTH.

Is Rockwell Automation a good value?

Turning to forward valuation, management expects to convert 100% of adjusted income into FCF, so assuming FCF of $5.80 to $6 would mean Rockwell trades on a EV/FVF multiple of around 19.7. It's not a bad valuation for a company with growth prospects, and it's certainly an attractive stock for those looking for exposure to potential upside from increased spending in heavy industry (energy, mining, transportation, and the like).

However, I would argue that the margin of safety in the stock simply isn't there anymore to justify buying it on a valuation basis only. Rockwell is now a stock for those believing in a mid-term cyclical recovery in industrial production.