The new year is almost upon us, which makes right now a great time to comb through your portfolio and make any changes where needed. Perhaps you'll find a losing investment that you can sell to take advantage of tax-loss harvesting. Or maybe you have some money lying around that you can use to top off your annual IRA contribution.

Image source: Getty Images.

Regardless of where the money comes from, if you are looking to invest, you're going to need a few stocks to buy. Here's a closer look at three stock ideas -- CVS Health (CVS 3.39%), Paycom Software (PAYC 2.74%), and Illumina (ILMN 2.51%) -- that I think are great choices as we head into 2017.

Down, but not out

2016 was a rough year to be an investor in retail pharmacy giant CVS Health. The company's shares were slammed after management stated that it expects to lose 40 million retail prescriptions next year due to competitive pressure. The news caused management to forecast 2017 guidance that was a bit below Wall Street's expectation.

There's no doubt that the volume loss will sting, but I think the market is missing the bigger picture. CVS should still be able to grow revenue and profits in the years ahead on the back of new-store openings and the continued rollout of MinuteClinics. The company is also making good progress at growing its presence in assisted-living and long-term-care facilities. Plus, 10,000 baby boomers are retiring every day, so the overall demand for pharmacy services is bound to steadily increase.

Image source: CVS Health.

In total, CVS Health is poised for a bright future, which is why its management team is projecting that it will grow its profits by double digits in the years ahead. That's a strong growth rate for a company that is trading for only about 13 times next year's earnings estimates.

Give your paycheck a boost

The technological shift to cloud computing has been a disruptive force in many industries, and the payroll-processing market is one of the areas that has seen its effect. Paycom Software is an emerging leader in the space, and the company's easy-to-use software offering is attracting small and medium-size businesses to its platform in droves.

Paycom gets its foot in the door with new customers by focusing on payroll processing, but its platform can offer help with a number of mission-critical HR functions. These include everything from background checks and scheduling to Affordable Care Act compliance and performance management. What helps separate Paycom from the rest of the pack is that the company's single sign-on system allows HR teams to track these functions in one place, which greatly simplifies their workload.

Image source: Getty Images.

What makes Paycom such a great investment opportunity is that payroll-processing and HR costs are ongoing expenses. That means that once a client signs on, it has to keep on paying to use the company's platform. In fact, 98% of Paycom's revenue is recurring, which gives the company a predictable base of revenue to grow from.

Paycom's revenue is expected to grow by more than 45% in 2016, and another 28% in 2017. The company's scalable business model should ensure that profit growth follows suit. While the company enjoys a premium valuation, this is one growth stock that I think is worth paying up to own.

The future of healthcare is already here

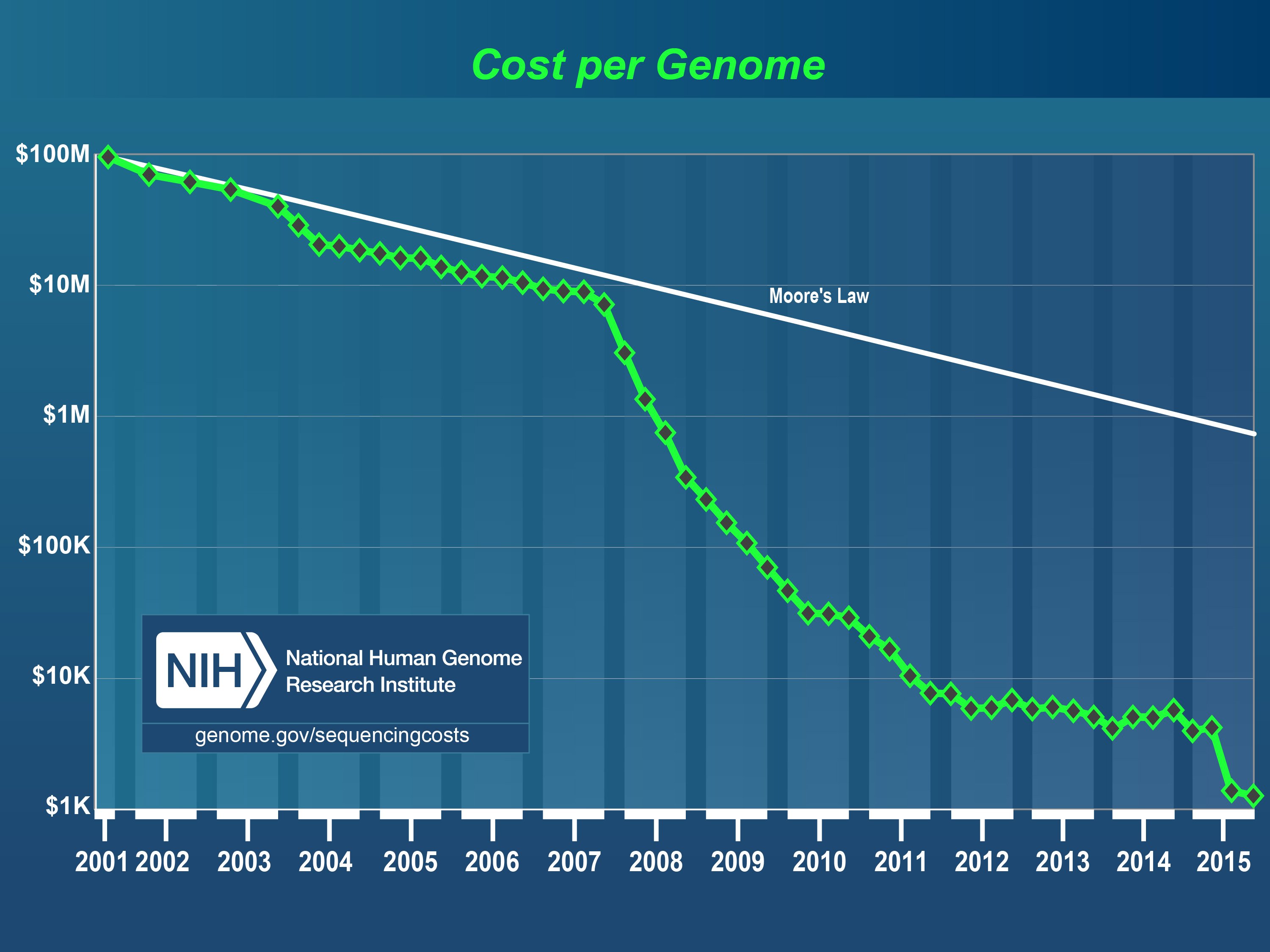

Image source: Illumina.

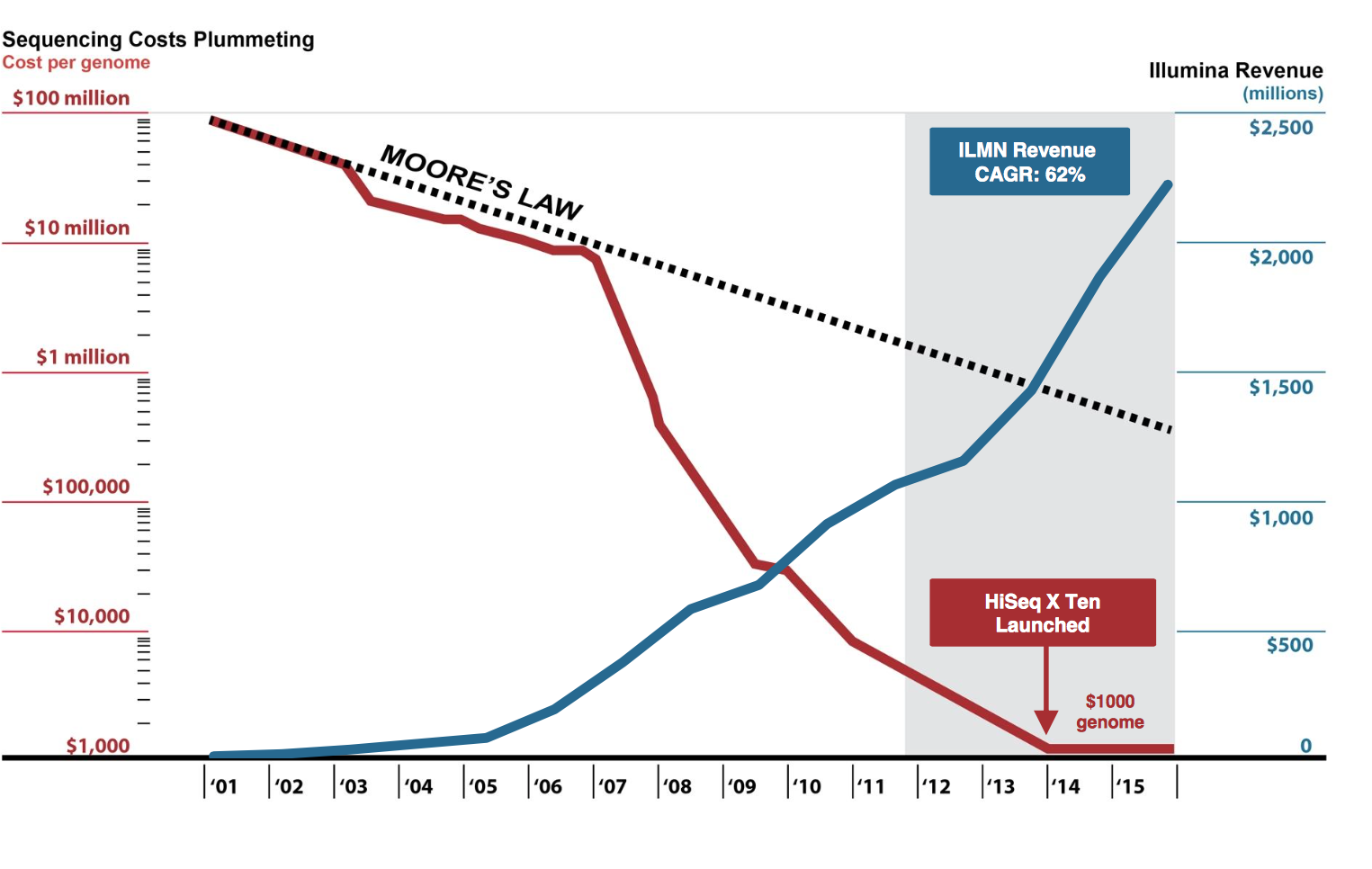

CAGR = compound annual growth rate. Image source: Illumina.