Giant integrated energy stocks was hammered by the oil downturn. That's old news now that oil price trends are starting to improve. If you have a positive outlook for the oil industry, now could be the right time to step in and buy one of these high-yield stocks. However, the downturn was a stark reminder of the risks inherent in this cyclical industry. Which is exactly why the top big oil dividend stock is ExxonMobil (XOM +1.83%).

Safety first

When you look at the integrated oil giants, ExxonMobil stands out. First, as an income investor, you'll be attracted to its streak of 34 consecutive years of annual dividend increases. Only Chevron (CVX +1.00%) comes close to that, with 29 years of annual hikes. After that, the pickings get slim. Royal Dutch Shell (NYSE: RDS-B), for example, has one of highest yields in the industry, but it hasn't increased its dividend for three years. Italian energy giant ENI (E +1.77%), meanwhile, cut its dividend during the downturn.

Image source: ExxonMobil.

So while Exxon's 3.6% yield is at the low end of the industry, it has proven to be one of the most secure payments. If you are looking for income, safety should be a key consideration. And on that score, Exxon has proven it cares greatly about rewarding its shareholders in good years and bad.

There's more to this story

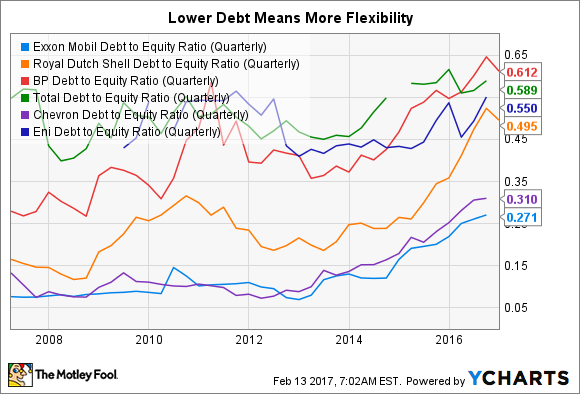

But Exxon didn't get to 34 years because it was lucky. It got there because of a conservative business model that focuses on operational excellence. For example, Exxon's debt is toward the low end of the industry. That's a trend that's been in place for years because of management's conservative bias. A modest debt load gives Exxon the flexibility to deal with adversity.

XOM Debt-to-Equity Ratio (Quarterly) data by YCharts.

Yes, debt levels rose during the oil downturn, but they remain at reasonable levels. Long-term debt, for example, made up a modest 15% (or so) of the capital structure at the end of the third quarter. The added leverage was used to protect the company's dividend and to support its capital investments during the lean years. That's an intelligent use of the balance sheet that protects investors and the company's long-term future without sacrificing safety. For comparison, Royal Dutch Shell's long-term debt makes up around 30% of its capital structure. That's not outlandish, but you can see why it hit the pause button on annual dividend hikes.

Then there's Exxon's long history of investing its shareholders' money better than its peers. The quickest way to see that is looking at return on invested capital, a metric where Exxon leads the pack year in and year out. With its low debt and smart investing, it's little wonder Exxon was able to remain in the black throughout the current downturn while many of its peers fell into the red. Note that Chevron, the only integrated oil giant with a dividend history as strong as Exxon's, was among the competitors that lost money during the downturn. Exxon really does stand out.

XOM Return on Invested Capital (TTM) data by YCharts.

The perfect combination

I'm not suggesting that Chevron, Eni, Shell, BP, or Total are bad companies. There are reasons to like them all. However, for dividend investors, Exxon stands above the pack as the best dividend stock in the oil industry. It's one of the best-run oil companies around, has a relatively low level of debt, and its history of protecting its dividend is top notch. It isn't the highest-yielding oil giant, but it's probably the safest. And if safety is as important to you as it is to me when analyzing a dividend stock, Exxon should hold the top spot on your oil short list.