It can be hard for growth investors to decide what stocks to buy because innovation means that today's winners might not be tomorrow's winners. Instead of gambling by focusing on the latest fad, consider building a long-term portfolio that's anchored by Apple Inc. (AAPL +0.13%), Amazon.com (AMZN +0.44%), Celgene (CELG +0.00%), Facebook (FB +1.08%), and Alphabet (GOOGL +1.02%). All five could have what it takes to sidestep competitive threats and dominate their markets in the coming years.

Fiercely loyal consumers

Mounting competition from Samsung and low-cost device makers in China had some people thinking that Apple's best days were behind it. However, those predictions haven't panned out -- especially after Samsung's reputation took a big blow when it was forced to recall its Note last year because of defective batteries.

IMAGE SOURCE: GETTY IMAGES.

Apple's iPhones, iPads, and Macs remain best-in-class options for innovation-hungry consumers. Apple's long track record of advancing technology has inspired impressive loyalty that's allowed it to build a profit-friendly ecosystem of services, such as iTunes.

After sluggish demand last year, iPhone demand is growing again, and with product refreshes on tap, there's plenty of reason to think that billions of Apple devices will provide a steady source of demand for Apple's app store.

Given that Apple has $246 billion in cash on the books, it's got the firepower to invest in R&D to maintain its lead. And since it's generating $65 billion in annual cash flow that can support dividend hikes and buybacks, it's hard to argue that Apple doesn't deserve a spot as a cornerstone holding in growth portfolios.

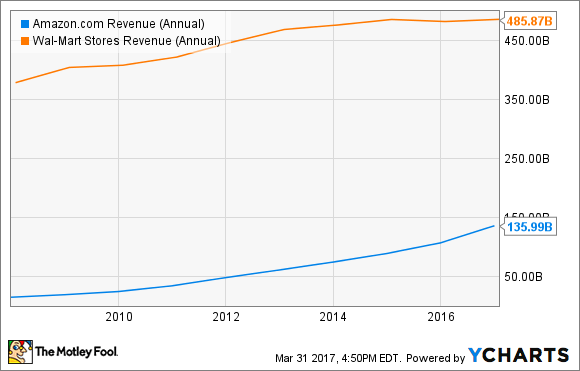

Plenty of market share left to conquer

The stacks of Amazon boxes on doorsteps last holiday season may have you thinking that Amazon is close to tapping out its market opportunity, but the numbers suggest that there's enough running room for this company to get much, much bigger.

In 2016, Amazon generated $136 billion in sales, up 27% from 2015. While that's a big number, sales would still have to triple for Amazon to match Wal-Mart's top line last year. According to the Census Bureau, online sales are increasing at a double-digit annual pace, but they only represent 8.4% of total retail sales.

AMZN Revenue (Annual) data by YCharts.

A bigger and wealthier global population offers plenty of expansion opportunity for Amazon's core business, but retail isn't the only reason why Amazon is worth owning in portfolios. Investments in information technology have allowed it to become one of the largest providers of cloud-based solutions, and its Prime service has made it a big source for consumer entertainment, too. Also, its recent push into virtual assistants means that its devices are sitting in living rooms nationwide, and that gives Amazon even more chances to connect with (and profit from) consumers. The company's Amazon Go, a checkout-less store prototype, and its AmazonFresh show it's hoping to shake up the $631 billion grocery retail market soon, too.

Expanding its markets

It's hard to find a company that's better at innovation than the biotech giant Celgene. It already markets a slate of billion-dollar blockbuster drugs, and it's enjoying a steady stream of revenue and profit growth thanks to R&D investments, acquisitions, and collaborations.

Its Revlimid is the most widely used first- and second-line therapy in multiple myeloma, and although Revlimid's sales are already $7 billion per year, R&D programs are expanding its use, and that has management targeting $8 billion in sales this year. It also markets the billion-dollar third-line multiple myeloma drug Pomalyst and the pancreatic cancer drug Abraxane, which brought in $967 million in sales last year.

In 2014, management launched the psoriasis drug Otezla, and although it's only been on the market a short time, it's already selling at a $1.2 billion clip. Otezla sales could increase to $1.7 billion or more this year. The company may also launch its first multiple sclerosis drug soon. It acquired ozanimod in 2015 when it bought Receptos for $7 billion, and following late-stage trial results that arguably position it as a best-in-class therapy, management plans to file for FDA approval soon. If approved, this could be yet another blockbuster drug for the company because the MS treatment market is worth $19 billion annually, and it's growing.

IMAGE SOURCE: GETTY IMAGES.

Celgene may also get an FDA OK to begin marketing a new leukemia drug later this year. Celgene co-developed enasidenib with up-and-comer Agios Pharmaceuticals, and a regulatory nod could come within the next few months, giving Celgene yet another intriguing source of growth.

With a stable of top sellers already and the chance for new drugs to hit the market in the coming year, this is one of my favorite growth stock picks for long-term portfolios.

Cashing in on community

Companies like Snap are attempting to challenge Facebook's dominance as the social media platform of choice, but these competitors will struggle to match Facebook's global reach.

Facebook's nearly 2 billion monthly active users are engaging in more meaningful communications with one another than ever before, and tapping into those engagements is providing Facebook with significant revenue and margin expansion opportunities.

In 2016, Facebook's revenue surged 54% to $27.6 billion, and its revenue per monthly user jumped 34% to $15.98. The ability to deliver more meaningful advertising to users and to leverage ad revenue across its fixed costs allowed Facebook's operating margin to expand 10% to 45%, and that translated into a 177% spike in net income to $10.2 billion.

Those are some eye-popping growth numbers, but what's even more impressive is that this could still be early days in Facebook's growth opportunity. Facebook's CEO Mark Zuckerberg thinks the company could have 5 billion active users someday, and as it moves toward that user goal, its investments in messaging, video, and devices could generate significant upside for investors over the next few years. For example, its messenger and WhatsApp services boast 1 billion and 1.2 billion monthly active users, respectively, and demand for those services continues to increase. Instagram continues to add advertisers, too.

Also exciting is Facebook's secretive Building 8 project that's working on next-generation hardware solutions. Building 8 hasn't announced any specific products yet, but it's only a matter of time before consumers get more insight into how Facebook plans to compete in consumer electronics.

Building better mousetraps

Eyeball-friendly simplicity has allowed Alphabet's Google to dominate search for more than a decade, and Alphabet is using its mountainous data to maintain an edge in helping people find and leverage content in increasingly helpful and informative ways.

Alphabet changed its name from Google a few years ago to better reflect its commitment to expanding beyond search, and that commitment has turned it into a leader in powering mobile consumer electronics hardware with Android. Approximately 85% of all the world's smartphones sold run on Android.

Last year, Alphabet's full-year revenue increased 20% to $89.5 billion, its free cash flow increased 55%, and its earnings per share increased 22%. That's compelling growth for a company of this size, and as consumers continue to embrace video, Alphabet's YouTube, Play, and Chromecast put it in an enviable position to continue growing.

Alphabet is using its massive financial flexibility to ingrain itself even more deeply into consumers' lives. Investments into new projects like Nest and Google Home perfectly position it to profit from the Internet of Things, and moonshots like self-driving cars and healthcare innovation via its Verily Life Sciences make it hard to argue that Alphabet doesn't deserve a spot as a core holding in growth portfolios.