Motley Fool contributors are constantly scouring the market for great investment ideas to share with our readers. And every once in a while, one sticks that gets us particularly excited.

This week, three of our contributors highlighted the stocks they are the most excited about. The surprising list includes Hormel Food Corp (HRL +2.68%), Wal-Mart (WMT +0.18%), and SunPower (SPWR +0.00%).

Image source: Getty Images.

Growing fond of SPAM

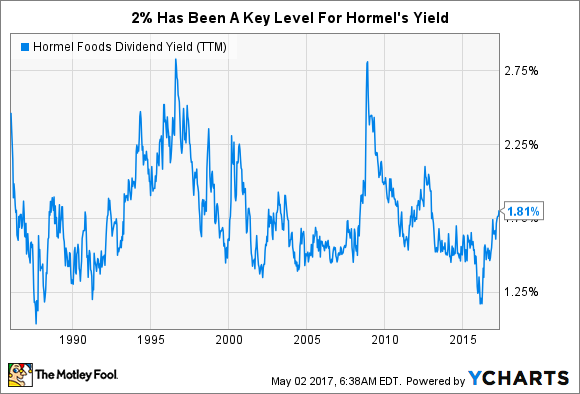

Reuben Gregg Brewer (Hormel Food Group): Hormel Food Corp isn't a name you would normally call exciting, but I'm super excited to have added it to my portfolio recently with its 2% (or so) yield. That may not sound exciting, but note that the company has increased its dividend for 51 years -- and the average annualized dividend increase over the past decade has been a massive 15%, roughly five times the historical rate of inflation! Hormel's long-term debt, meanwhile, makes up just 5% of its capital structure, putting the food maker on a rock solid financial foundation.

HRL Dividend Yield (TTM) data by YCharts

That 2% yield, meanwhile, is toward the high end of the company's historical range. It's been higher, but 2% is about the point where the stock gets interesting, valuation wise. (I'll eagerly buy more if the yield goes higher...) What's pushing the stock down, and the yield up, is the fear that packaged foods are falling out of favor with consumers. Hormel is the maker of SPAM, Hormel Chili, and Dinty Moore, among other things, so this is a real concern.

But Hormel isn't sitting still. It recently added Wholly Guacamole, Muscle Milk, and Justin's nut spreads to the portfolio, shifting into categories and brands that resonate with consumers. And its fresh meats businesses, including pork and turkey, aren't as exposed to the packaged food problem. Meanwhile, with debt at such low levels, it has plenty of financial flexibility to change with the times as needed. I'm excited because this was, in my opinion, a rare opportunity to add a great company to my portfolio at a very reasonable price. That doesn't happen very often.

An online retail growth story

Tim Green (Wal-Mart): Mega-retailer Wal-Mart is finally taking e-commerce seriously. The $3.3 billion acquisition of start-up Jet.com last year, while expensive, put Jet founder Marc Lore in charge of the company's entire e-commerce operation. The biggest move so far: free two-day shipping on all orders over $35.

This not only made Amazon Prime less attractive for those who care mainly about free shipping, but it made Amazon's non-Prime free shipping offer look stingy in comparison. Amazon's $49 minimum for free 5-to-8-day shipping has now been slashed twice, first to $35 and then to $25. Those moves were likely in direct response to Wal-Mart.

Even as Wal-Mart is aggressively going after online sales, the company's stores are performing well. Wal-Mart has enjoyed a long streak of comparable sales growth in a retail environment that has given many retailers trouble. Profits are taking a hit due to these investments, but the company is positioning itself to maintain its brick-and-mortar dominance while becoming a major e-commerce player.

With Amazon dominating online retail today, it's easy to imagine a future where the company is completely unstoppable. But retail is not a business conducive to monopoly. Even Wal-Mart, as dominant as it is, accounted for less than 6% of U.S. retail sales in 2016. Online retail changes the game, but the idea that Wal-Mart can't compete with Amazon is dead wrong.

The potential of Wal-Mart's online business makes the stock an exciting one to watch. I don't own it, but it's been on my list for quite some time. If Wal-Mart can keep up the e-commerce momentum, it could make for a great long-term investment.

The biggest financial opportunity in the world

Travis Hoium (SunPower): A recent presentation from GTM Research estimated that the solar industry would be worth $2.8 trillion between now and 2035. As disruptive as solar energy has been, if that estimate is correct it could just be getting started. And SunPower is a leader in the solar revolution.

Where SunPower made its name is with high efficiency solar cells, which allow it to pack more energy production on a roof or in a field than any other company. But the company has faced challenges as competitors from China rapidly cut costs and undercut the company's competitive advantage. 2017 will be a transitional year, but I think 2018 will allow SunPower to emerge as a healthier, better positioned company in a booming industry.

SunPower's high efficiency products are gaining traction in residential and commercial markets, where space is constrained and efficiency is highly valuable. In the power plant business, SunPower is now making a panel called the P-Series, which will leverage high efficiency commodity cells, and the "Oasis" platform, which will become a cost effective offering around the world. And 2018 is when that product should really start gaining steam.

The market has been very pessimistic about solar stocks in general lately, but the industry is improving. As power is concentrated in the hands of the best companies -- like SunPower -- it should lead to greater profits and higher returns. And that's why I'm excited about this stock in 2017 and beyond.