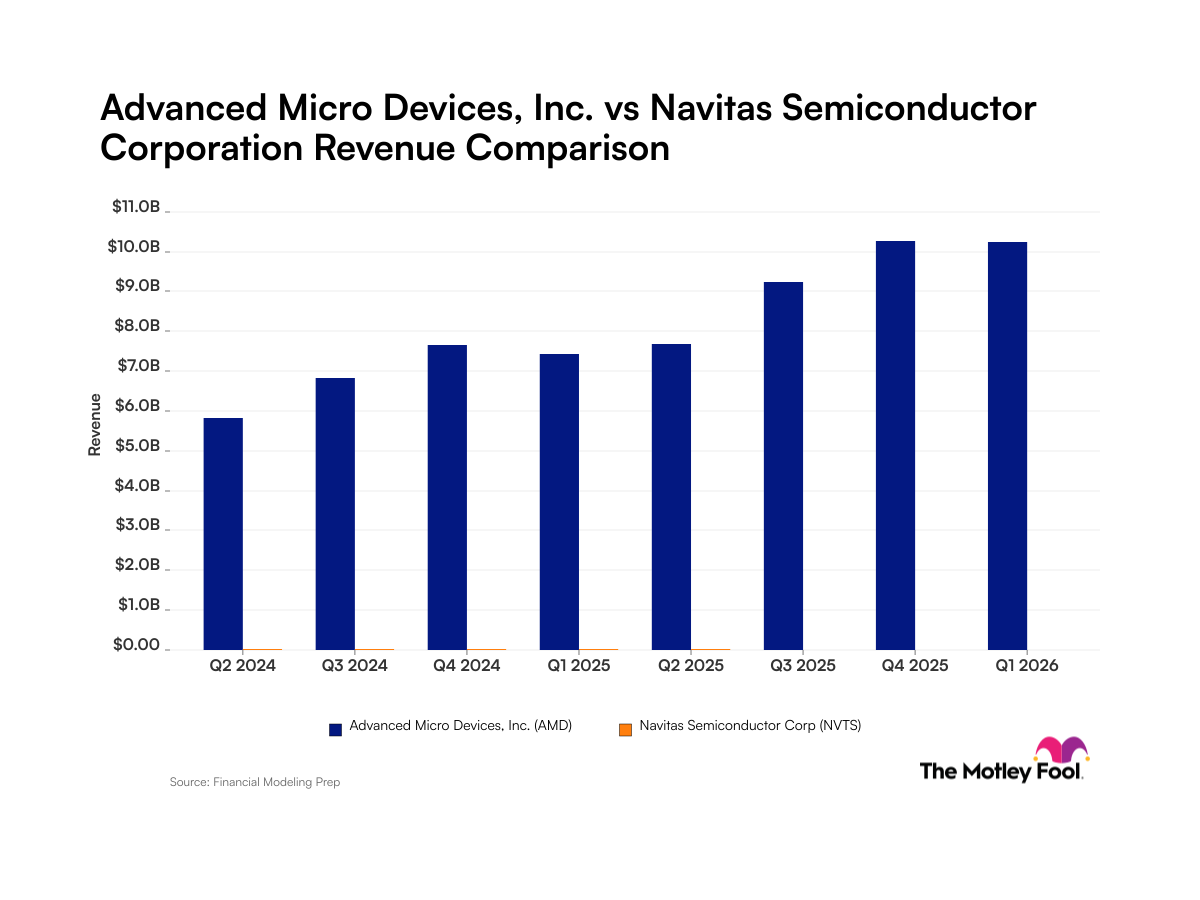

Advanced Micro Devices (AMD +4.16%) has made terrific strides in the graphics processing unit (GPU) market in recent months by poaching market share from NVIDIA (NVDA +0.96%). In fact, AMD grew its share from 20% in 2015 to 28% in 2016 as it saw a massive bump in sales of midrange GPUs priced below $299, according to estimates from Mercury Research.

Analysts, however, are now concerned with profit margins, as the company's market share gains have mostly come from low (price) hanging fruit. But investors should keep in mind that the company is taking aim at the higher end of the market with its next-generation GPU platform -- the Vega.

Why AMD wants to go high end

Internal company estimates suggest that the top-end GPU market accounts for less than 15% of sales but represents two-thirds of the margins. The company failed to break into this segment with the Polaris GPUs, which primarily target midrange desktops and below.

Image source: AMD.

Therefore, the company is missing out on the most lucrative segment of the GPU market, but it believes that the Vega will help address this opportunity.

Taking the game to NVIDIA

NVIDIA dominates the high-end GPU market, but AMD believes that its Vega GPUs are capable enough to compete against its rival's premium offerings. As it turns out, test results from the open-source Baidu DeepBench benchmark indicate that the Vega can outperform the NVIDIA P100 Tesla GPU in machine-learning applications by a fair margin.

Now, NVIDIA claims that the Tesla P100 is one of its most advanced GPUs, with the specs to substantially boost a data center's computing power while reducing costs by 60% simultaneously. NVIDIA's Tesla GPUs have already made significant inroads into the cloud-computing market, with the likes of Microsoft and Tencent using them to advance their artificial intelligence (AI) capabilities.

But AMD can make a dent in this market if Vega manages to outperform NVIDIA's top-of-the-line offering in independent machine intelligence tests. What's more, AMD isn't leaving anything to chance, as it has launched a number of open-source software solutions for developers to take advantage of its GPU accelerators.

The company's Radeon Open Compute platform is geared to support a variety of AI frameworks that include Facebook's Caffe and Google's TensorFlow machine learning library, among others. As such, it won't be surprising if the cloud-computing GPU market plays a critical role in driving results at AMD, especially since cloud data center workloads could grow at 26% a year until 2020, according to Cisco.

The potential financial impact

AMD believes that its expansion into high-end markets like cloud computing and machine intelligence will boost profit over time. The company expects gross margin to top 36% in 2018, up from about 31% last year. What's more, AMD expects further margin expansion -- to 40% or more -- by 2020 due to an improving product mix.

Of course, whether or not the company will enjoy this increased profitability depends on how its new products perform in the real world. But as something to keep investors bullish, AMD estimates the data center market alone will be a $21 billion opportunity in just a few years.

Image source: AMD.

Investors will have to wait until later this year before the launch of the new Vega GPU. If AMD can deliver with an attractive offering to tackle next-generation cloud computing, its top and bottom lines will get a shot in the arm by capturing just a small slice of this burgeoning market.