When most analysts and investors think about Bank of the Ozarks (OZRK 1.18%), they think about a bank that has grown rapidly since the financial crisis by acquiring more than a dozen of its peers. Over the past five years alone, the $21 billion bank based in Little Rock, Arkansas, has quintupled the size of its balance sheet.

But while it's true that Bank of the Ozarks has grown at a torrid pace, most of that growth hasn't come from acquisitions. It has come instead from a Dallas, Texas-based unit of the bank known as the real estate specialties group, or RESG, which was established in 2003 to make large and complex commercial real estate loans.

Understanding RESG

RESG is responsible for the majority of Bank of the Ozarks' growth since 2012. At the end of the second quarter, the unit was responsible for 68% of the organically originated loans on the bank's balance sheet, as well as 93% of the $11.9 billion worth of off-balance sheet liabilities that must be funded primarily over the next three years.

*Second quarter 2017. Data source: Bank of the Ozarks. Chart by author.

RESG is such an important part of Bank of the Ozarks' growth strategy that the bank's chairman and CEO, George Gleason, recently handed off six direct reports to other executives in order to free Gleason up to spend 75% of his time overseeing the unit.

The 63-year-old longtime head of Bank of the Ozarks explained at an industry conference recently that he's shifting his responsibilities in this way because RESG is expected to continue growing at a rapid clip in the years ahead. The bank believes RESG will double in size over the next three and a half to four years, and double again in seven to nine years.

Yet, it's fair to think that other factors played into Gleason's decision as well. In the first case, the president of that unit, Dan Thomas, resigned abruptly on July 27, two weeks after selling a third of his stake in the bank's stock. Thomas had not only become the second-highest paid executive at Bank of the Ozarks by the time he resigned, he was also the bank's chief lending officer and vice chairman of the board.

Over the past five years, Bank of the Ozarks has emerged as a major financier of major construction and development projects in virtually ever major metropolitan area in the country. Image source: Getty Images.

A void of leadership

Thomas' departure left a void at RESG, given that the unit is staffed by 107 employees who, in most cases, lack banking experience. A review of approximately a third of their LinkedIn profiles reveals only three who worked at banks previously; most of the rest had previously served in different capacities in the commercial real estate industry. Moreover, the average tenure of the seven members of Bank of the Ozarks of RESG's origination's team, disclosed by the bank in a recent presentation, is only three and a half years.

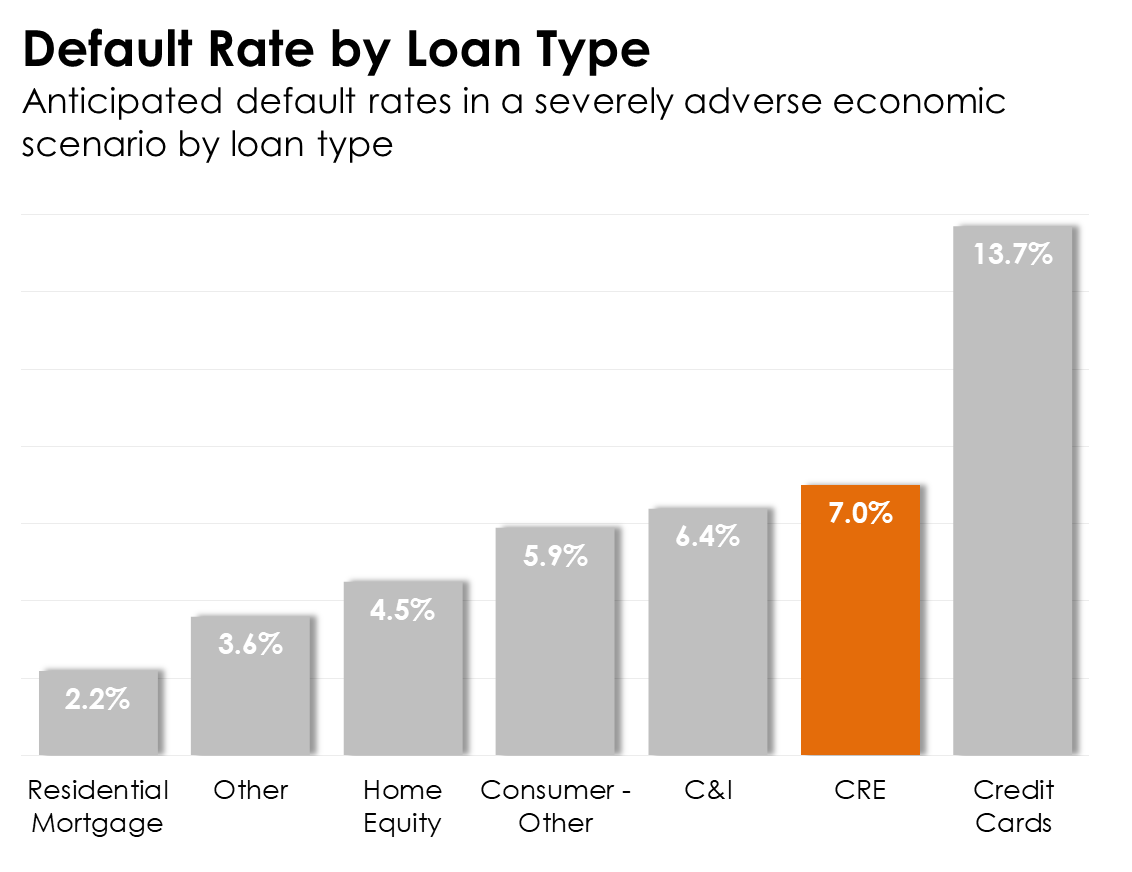

This matters because commercial real estate loans are among the riskiest types of loans banks make. To this end, commercial real estate loans are modeled each year by the Federal Reserve in its annual stress tests to experience higher default rates than all other types of loans, with the sole exception of credit cards, in a severely adverse economic scenario.

Data source: Federal Reserve. Chart by author.

This goes a long way toward explaining why commercial real estate loans played a leading role in the thousands of bank failures that swept through the industry in the 1980s and 1990s. And the same was true in the in the wake of the financial crisis, as over 70% of U.S. bank failures from 2008 to 2011 were commercial real estate lending specialists.

"Investments in commercial real estate (for example, office buildings, retail centers, and industrial facilities) at any stage of the development process have traditionally been quite risky," the FDIC explains in its History of the Eighties. "Real estate markets as a whole are traditionally cyclical, so that even the most well-conceived and soundly underwritten commercial real estate project can become troubled during the periodic overbuilding cycles that characterize these markets."

In sum, Bank of the Ozarks' heavy concentration in commercial real estate loans, coupled with the scant banking experience of RESG's origination team, is one reason to believe that the bank isn't as conservatively managed as its executives want analysts and investors to believe.