What happened

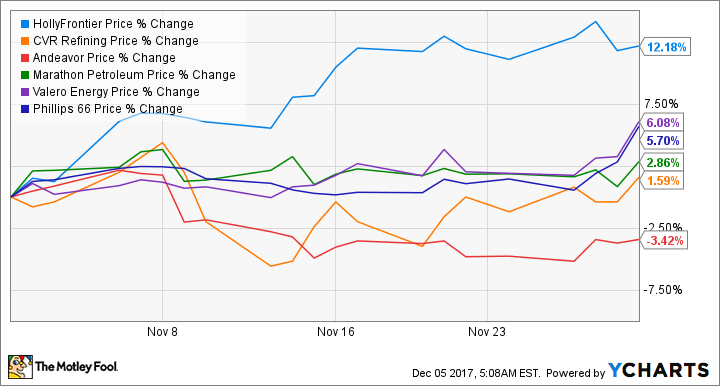

Shares of oil refiner HollyFrontier (HFC +0.00%) climbed 20% in November, outpacing many of its independent oil refining peers. The impetus for the notable gain was a respectable third-quarter earnings report and market conditions that continue to improve in HollyFrontier's favor.

So what

Let's start with the obvious catalyst: HollyFrontier's third-quarter earnings. The company reported earnings of $1.53 per share compared to $0.42 per share this time last year. Beating 2016 results isn't that impressive considering how bad that year was for refiners in general, but HollyFrontier also benefited from completing an investment plan to improve operations at its Rocky Mountain refineries, as well as the addition of the Petro-Canada Lubricant business.

Image source: Getty Images.

The other element fueling HollyFrontier's rise is that the refining market is looking much better for the company. The most significant reason for this is the wider price spread between international and domestic crude prices.

Gasoline and other refined products are internationally traded products, which means that the price of these products tends to track international crude price benchmarks -- Brent -- more than domestic crude prices. Over the past few months, the prices of domestic crudes -- America's benchmark is West Texas Intermediate (WTI), and Canada's heavy oil benchmark is Western Canadian Select (WCS) -- have become less expensive relative to international prices. In November, WTI traded at a $5-per-barrel discount to Brent, and WCS recently traded at a $12-$15 per barrel discount to WTI.

This market environment is advantageous to refiners because it means they pay less for their feedstock (crude oil) while the price of the finished product remains steady. The wider the gap between these two prices, the better for refiners.

One would assume that all refiners would benefit from this, but HollyFrontier's stock has been one of the few that has responded to this change.

One possible reason for this is that HollyFrontier's operations have a much larger exposure to Western Canadian Select than many of its peers. Over the past few years, the company has been configuring its refineries and adding infrastructure to handle the harder-to-process crudes that come out of Canada because of the significant price discount. With oil sands production increasing, it's likely that the WCS discount will remain in place for a while.

Now what

The refining industry has gone through a wave of consolidation recently as larger players have been buying some of the smaller refiners to add economies of scale and greater geographic diversity. HollyFrontier has mostly stood pat during this wave, electing instead to acquire a lubricant manufacturer and tweaking the ownership structure of its subsidiary partnership. That is par for the course with HollyFrontier's management, as it has a history of zigging when the rest of the industry zags.

With per-barrel international oil prices in the low $60s, it is encouraging North American producers to grow. Even with the wider price spreads, the price of crude is enough for many companies to turn a so-so profit. It suggests that unless the U.S. and/or Canada drastically expands its crude oil export capacity, that price spread will remain in place for a while. That should bode well for HollyFrontier in the upcoming quarters.