There's no question that Rio Tinto plc (RIO +2.54%) is a giant miner -- one of the world's biggest, in fact. That's a desirable trait in a miner, because size can offer economies of scale. However, if you are looking for a way to invest in the out-of-favor uranium industry, then Rio is just too big. Cameco (CCJ +3.98%) is a better uranium stock. Here's why...

Too big, too small

Rio Tinto produced around 6.5 million pounds of uranium in 2017. That's a sizable figure, especially when you consider that uranium-focused Energy Fuels (UUUU +8.40%), which expects to be the largest U.S.-based producer of the nuclear fuel in 2017, is projecting production of 1.7 million pounds total that year. Rio is clearly the larger uranium miner.

Image source: Getty Images

But there's a problem here if you're looking to get specific exposure to uranium: Only about 1% of Rio's revenues come from uranium, the rest is spread across iron ore (around 45%), aluminum (roughly 25%), copper (8%), and coal (18%), among other things. Rio Tinto is a way to get broad exposure to the mining industry, but it isn't a great way to get exposure to uranium.

Uranium-focused Energy Fuels, meanwhile, is big in the United States, but not in the uranium industry. Canada's Cameco expects to produce around 24 million pounds of uranium in 2017. That's multiples of what Energy Fuels and Rio expect to produce. But, like Energy Fuels, Cameco only mines for and produces the nuclear fuel. Essentially, Cameco has scale in uranium.

This is notable today because it provides Cameco key benefits, like a global reach that smaller players lack. For example, Cameco sells the nuclear fuel to developing Asian nations like China and India. Most of the growth in nuclear power plant construction is set to come from developing nations like these, not developed markets like the United States -- Energy Fuels' primary market.

Getting through the downturn

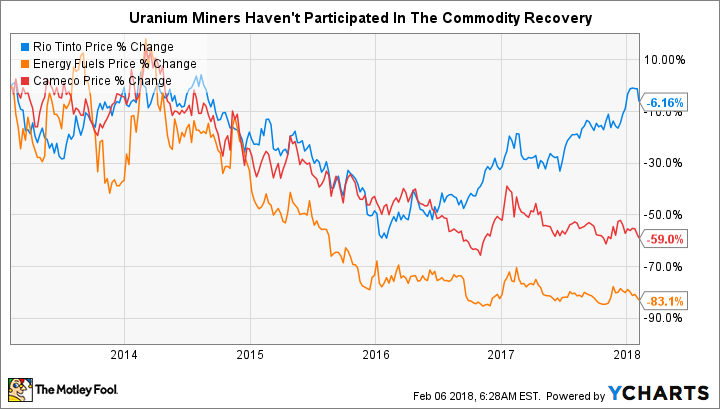

That said, part of the problem with a focused uranium miner is that uranium spot prices are hovering near their lowest point in roughly 15 years. A diversified miner like Rio has benefited from the upturn in other commodities, while both Energy Fuels and Cameco continue to struggle because of their unique focus on uranium. Which is where scale comes in again.

Cameco's size allows it to cut back production even during lean times and still sell enough uranium to satisfy its contract commitments. For example, it announced plans to shutter two mining operations in 2017. Although temporary, that move will allow it to reduce inventory so it can leave its uranium in the ground for, hopefully, better days. These two assets produced 7.8 million pounds of uranium in the first nine months of 2017. It's shutting down more production than either Rio or Energy Fuels expects to mine in 2017.

With prices so low, curtailing production makes financial sense for Cameco and the uranium market, which is oversupplied at the moment. It also aids in the effort to reduce operating costs, which is a key focus for the miner today.

However, you can't just cut production if you don't have the financial strength to support your business without the cash flow that the curtailed production produces. Luckily, Cameco has scale and has a solid financial foundation.

There are signs of life in the uranium market. Image source: Energy Fuels

For example, Cameco's current ratio at the end of the third quarter was 5.4. That suggests the miner could pay its near-term bills five times over and still keep going. Long term debt, meanwhile, is just 25% (or so) of the capital structure, a modest number for any company. It has the financial flexibility on its balance sheet to make the changes it needs to survive the downturn so it can bring production back online when the upturn comes.

Know what you're getting

Cameco is the largest pure play, publicly traded uranium miner. It has scale and financial flexibility, both of which it's using today to keep its business going through a deep industry downturn. I expect investors will be well rewarded when supply and demand start to balance out and uranium prices pick up again.

When that happens, however, is impossible to predict. Uncertainty is high here, but risk appears to be relatively low since a huge amount of bad news is already priced into the uranium sector. That said, despite the recovery potential, Cameco is still only appropriate for more aggressive investors.