When I was younger, my portfolio contained a large number of limited partnerships. I'm an income-focused investor, and the high yields this niche sector provides, coupled with other advantages, was simply too great to pass up. But I'm older now, and while I still love the dividends that limited partnerships throw off, there are other considerations that keep me out of these investments. Here's why I refuse to buy these great high-yield dividend stocks, though you might still want to own them.

Great is a strong word

The list of positives surrounding the limited partnership structure is short, but their benefits are huge for income investors. First off, the structure is specifically designed to pass income on to unitholders. That means, generally speaking, you'll find high yields throughout the MLP space. Even the largest and strongest partnerships tend to offer giant yields. For example, midstream industry bellwether Enterprise Products Partners L.P. (EPD 0.05%) currently offers investors a huge 6.1% distribution yield. Compare that to an S&P 500 Index fund's roughly 2% yield and you're sure to be smitten.

Building your nest egg requires balancing today's benefits with future costs, which is a big issue when considering a complex structure like limited partnerships. Image source: Getty Images

To make that yield even better, however, the MLP structure effectively makes you a part-owner (a partner) in the company. Limited partnerships don't pay taxes at the corporate level, they pass through all of that to unitholders on a pro rata basis, allowing tax benefits like depreciation to get passed along to unitholders. It's a little complex (more on this in a second), but the end result is that a portion of the income you receive will likely be tax-advantaged, allowing you to avoid taxes in the year you receive it. The amount of income that avoids current taxation varies from partnership to partnership and year to year, but tax-advantaged income is a nice bonus if you are trying to maximize current income (and minimize the taxes you pay).

Passing so much income on to investors does cause some problems, in that it doesn't leave much cash around for investing in expansion projects and acquisitions. Which means that MLPs often have to tap the capital markets to fund growth. However, it isn't that hard to find partnerships, like Magellan Midstream Partners, L.P. (MMP +0.00%), that manage to live largely within their means and don't overleverage themselves or dilute current unitholders to grow. Enterprise is shifting gears right now to self-fund more of its growth spending, as well, a move that will make it an even more desirable income investment once that transition is complete.

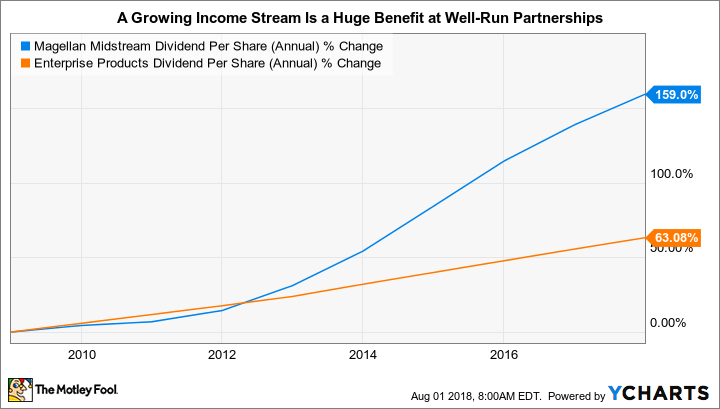

MMP Dividend Per Share (Annual) data by YCharts

Growth is important to keep in mind as an income investor because the buying power of a stagnant dividend will be eroded by inflation over time. But that's not an issue for well-run partnerships like Enterprise and Magellan, which have increased their distributions annually for 21 years and 18 years, respectively. The growth rates on those distributions, meanwhile, have easily beaten the historical growth rate of inflation over time. So these MLPs have increased investors' buying power while providing above market yields. Not all MLPs manage to achieve such long-term success, however, so you'll want to be selective when investing.

If you are an income investor like me, limited partnerships should sound pretty enticing so far. And there's more variety in the LP sector than you might realize, too. Midstream oil and gas is the largest category in the MLP sector by a wide margin, but you can find an amusement park owner, a funeral services company, mining concerns, shipping owners, energy services firms, real estate and infrastructure MLPs, and financial firms that make use of the structure, too. Not all of these are great investments, of course, but there's more diversification in the space than you might realize. Adding a high-yield limited partnership to your portfolio is not hard to do.

The fly in the ointment

In short, there are a lot of things to like about limited partnerships. Which brings us to the fact that I, sadly, no longer allow myself to buy any of these high-yield investments even though I think some (like Magellan and Enterprise) present great investment opportunities. The big-picture reason is complexity.

I'm getting to the point where my own longevity is starting to become a much more important issue to consider. Because of this, I've added a somewhat unique factor to my stock selection screen: "Would I want my wife to own this investment if I were to die?"

|

Limited Partnership |

Yield |

Market Cap |

Sector |

|---|---|---|---|

|

Enterprise Products Partners |

6.1% |

$63 billion |

Midstream energy |

|

Magellan Midstream Partners |

5.5% |

$16 billion |

Midstream energy |

|

AllianceBernstein Holding L.P. |

8.9% |

$3 billion |

Finance |

|

Alliance Resource Partners, L.P. |

11.3% |

$2.6 billion |

Mining |

|

Brookfield Infrastructure Partners L.P. |

4.6% |

$16 billion |

Infrastructure |

|

Brookfield Property Partners L.P. |

6.4% |

$14 billion |

Real estate |

|

Cedar Fair, L.P. |

5.4% |

$3 billion |

Amusement parks |

|

Teekay LNG Partners L.P. |

3.3% |

$1.3 billion |

Shipping |

Data source: Yahoo Finance

That's sounds morbid, and perhaps it is, but I don't want to leave my wife and daughter with a portfolio that they can't easily understand. And limited partnerships are not easy to understand. They are pass-through entities that result in unitholders being treated like they directly own the MLP on a pro rata basis. That's why unitholders benefit from tax shields like depreciation.

But that benefit comes at a cost and it makes April 15th a complicated affair since you have to include your share of all of the MLPs tax issues in your taxes. For starters, you have to wait for a special tax form known as a K-1 before you can fill out your taxes. That K-1 contains a jumble of numbers that break down what you, the partner, are responsible for including in your taxes. You get a different form for every MLP you own and it isn't always easy to figure out what to do with the numbers. In fact, it's probably best to get an accountant if you own LPs.

If the yearly K-1 wasn't bad enough, selling units come with their own tax headaches. Limited partnership distributions have tax advantages in the year you receive them, but you can't avoid Uncle Sam forever. A portion of your distributions are likely to be treated as a return of capital, which reduces your cost basis and, thus, increases the capital gains taxes you face when you sell. But it's not that simple (it's never that simple). Some of the reduction in your cost basis will be related to things like depreciation or appreciated inventory, which are taxed differently. These are "recapture" items that are taxed as current income. So your capital gain will end up being broken down into different categories when you pay taxes. I have a hard time getting my head around this at times, I'm certain my wife won't want to try.

I love them and I have to pass

In the end, limited partnerships are a great investment option for income investors. They offer generally high yields, tax-advantaged income, and for well-run partnerships distributions that can keep up with or exceed inflation. However, there is a downside to the structure since you are, effectively, a part-owner of these pass-through entities. They will increase the complexity of your taxes every year you own them and add an extra level of work when and if you sell. If you don't have a problem taking on that extra work and complication, they are a great option, but if you, or a loved one, aren't likely to be comfortable shouldering the extra work involved, you'll want to think twice before buying an MLP. The latter, sadly, is the camp I currently fall into.