The agricultural technology ("agtech") and lithium industries may be two of the most important of the early 21st century. Investors interested in owning both, and who know a good BOGO sale when they see one, will want to take a closer look at FMC Corporation (FMC 1.74%) this month.

Why? Because FMC Corp. is currently the world's fifth largest agtech supplier and one of the largest lithium miners on the planet. It's also about to split into two so as to better organize operations and create shareholder value. The agtech business will stay in place as FMC Corp., while the lithium segment will become a separately listed company called Livent Corporation. The spinoff is on track to occur next month, which means investors who buy shares of the parent now will end up owning both companies later this fall.

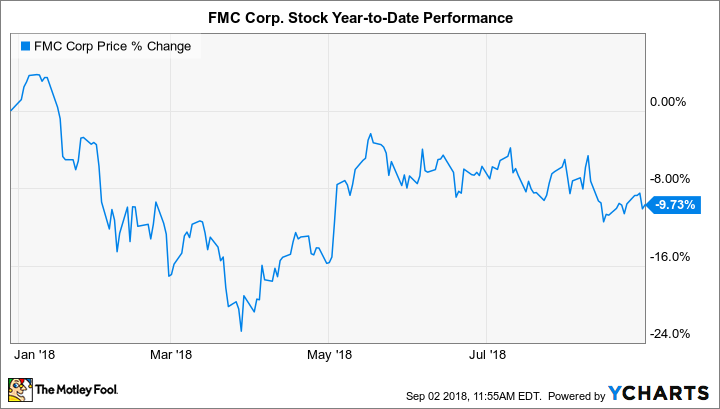

Turns out it could be a pretty good deal. FMC Corp. stock is relatively cheap following record financial performance through the first half of 2018 and a nearly 10% drop in share price since the beginning of the year. That makes it my top stock to buy in September.

Image source: Getty Images.

All-around strength

The business absolutely crushed the first half of 2018 by delivering 97% year-over-year growth on the top line and a 197% jump in segment EBITDA. Net income saw a nearly $450 million improvement from the first six months of last year. How did the business achieve nearly triple-digit improvements from the year-ago period?

Well, back in March 2017, FMC Corp. acquired certain agtech assets from DuPont in a win-win transaction. The former received a formidable portfolio of insecticides for a cool $1.2 billion -- and threw in its health and nutrition business to boot. The latter appeased regulators to gain approval for its megamerger that formed DowDuPont. FMC Corp. closed the transaction last November, so this year is the first with the new agtech products contributing. It helped. A lot.

The agricultural solutions segment -- what will remain after Livent Corporation gets kicked from the nest -- delivered $700 million in EBITDA in the first half of 2018 on $2.5 billion in sales. While the global agriculture markets from fertilizers to seeds to herbicides to grains are in a multi-year struggle, insecticides -- the specialty of FMC Corp. -- remain in high demand. Over half of segment revenue comprised insecticide sales in the opening half of the year.

That has helped the agtech leader to exceed even its own ambitious targets. At the time of the acquisition, the agricultural solutions segment was expected to achieve $3.8 billion in revenue in 2018. The latest guidance calls for $4.2 billion in sales this year.

That's not to suggest the lithium segment is weak. Rather, it means both major businesses of FMC Corp. are firing on all cylinders right now. In the first half of 2018, the lithium segment reported 51% higher revenue and 90% higher EBITDA than last year, at $210 million and $101 million, respectively. Investors may be surprised -- and encouraged -- by how that's generated.

In a move to prepare for the upcoming spinoff, this year FMC Corp. began breaking down its lithium segment performance by product. Here's the revenue distribution for the first half of 2018:

|

Product |

First-Half 2018 Revenue |

Application |

|---|---|---|

|

Lithium hydroxide |

$102.7 million |

Premium-grade metal for battery manufacturing |

|

Butyllithium and specialty compounds |

$82.5 million |

Industrial chemical synthesis, ceramics |

|

Lithium carbonate |

$25.5 million |

Metal for battery manufacturing and production of lithium hydroxide |

|

Total |

$210.7 million |

According to the U.S. Geological Survey, total lithium market breakdown in 2017 was 46% batteries, 27% ceramics & glass, 5% polymer production, and 22% other |

Data source: SEC filing.

That battery manufacturing materials comprise the majority of total segment revenue isn't surprising, but investors may be surprised to learn that it's just 61%. However, the other 39% is derived from a valuable niche application in industrial polymer synthesis and a handful of other specialty applications, showing the business is relatively diversified.

Of course, battery manufacturing applications will come to dominate the business in short order, but FMC Corp. is well prepared by focusing on the premium end of the spectrum.

While battery manufacturers can use both major commodities -- lithium hydroxide and lithium carbonate -- lithium hydroxide is easier to process and formulate into specific battery chemistries. That, and the fact that it's made from lithium carbonate, adding a process step and therefore a cost, allows it to trade at a premium price for saving battery manufacturers the trouble.

That's why, in 2016, FMC Corp. announced it would triple annual production of the premium material to 30,000 metric tons by 2019. Not only does the expansion remain on track, but the company also expects to have 80% of that capacity entered into long-term contracts by the end of this year. Meanwhile, the company is also on track to double annual production of lithium carbonate in Argentina to 40,000 metric tons by 2022.

In other words, so long as prices remain healthy, there could be years of double-digit growth in store.

Image source: Getty Images.

What about that spinoff?

Aside from knowing that the separation of the agtech and lithium businesses is on track to occur in October, investors don't have many details just yet.

However, based on the typical procedure for spinoffs, investors will receive a fraction of a share of the spinoff company (Livent Corporation) for each share of the parent company (FMC Corp.) they own. The market valuation, and therefore share price, of the parent company will be adjusted lower to make up for the "loss" of the assets included in the spinoff. Of course, it will all wash out for shareholders, as they'll still own the same total valuation, just split between stock in two companies.

Given that Livent Corporation will immediately become one of the largest pure-play lithium stocks, it may very well earn a higher value over time -- that's the "to better create shareholder value" argument for the spinoff -- than it could possibly contribute to a company as large as FMC Corp. That's especially likely if it continues on its torrid pace of growth and executes its expansion plans.

When investors combine the solid performance of the agricultural solutions segment, the double-digit growth of and long-term plans for the lithium segment, the 10% year-to-date drop in share price, and management's willingness to unlock value by allowing a strategically important business to run wild, there's a strong argument for buying shares of FMC Corp. in September. That's why it's my top stock to buy this month.