On the surface, it might seem like an easy choice for high-yield and dividend growth investors comparing Emera Inc. (EMRAF -0.08%) and Brookfield Infrastructure Partners LP (BIP -2.28%).

Emera's dividend yield of 5.6% is substantially higher than Brookfield Infrastructure's 4.7% at recent prices, and it has grown the dividend by an average of nearly 10% per year for a decade. Furthermore, Emera's heavy exposure to Florida, where its biggest subsidiaries are based, gives it solid upside to keep growing the payout for years to come.

Income investors might prefer Emera, but this Fool says Brookfield Infrastructure should deliver better total returns. Image source: Getty Images.

Lead-pipe cinch, right? Emera it is!

Not so fast, my investing friend. Brookfield Infrastructure shouldn't be ignored. Its global scale and participation in water, transportation, and telecommunications could make it the far better growth investment.

Let's take a deeper dive into both and see what we can learn.

Emera's Florida-focus is a strength and a weakness

In the first half of 2018, Emera saw its Florida and New Mexico segment generate 59.7% of adjusted net income, resulting from its acquisition of TECO Energy (Tampa Electric) in 2016. This acquisition was quite important to the company, giving it access to one of the best growth markets for any utility in North America: Florida.

In a recent investor presentation, Emera pointed out that Florida is a top-five growth state, with an average of 1,100 people moving there every day. Emera operates the third-largest public electric utility, Tampa Electric; a large solar operation in Florida Solar; and Peoples Gas, the state's largest natural gas utility.

The company is investing heavily in this market, too, balancing between expanding to meet the state's growing population and modernizing its infrastructure and power generation to improve efficiency and profitability. Emera plans to spend $6.7 billion on capital expenditures from 2018 to 2020, with most of that dedicated to Florida. That's a giant increase from its pre-acquisition spending:

EMRAF Capital Expenditures (TTM) data by YCharts.

At the same time, management has prioritized improving the balance sheet. Through the end of June, Emera's capital structure was comprised of 60% debt and only 29.2% equity. This is an improvement from 62.3% and 27.8% year over year, but still below the company's target of 55% debt and 35% equity by the end of 2020:

Image source: Emera presentation.

To reach this target, Emera will utilize more of its cash-flow growth for capital improvements and expansion.

The result? Over the next three years, the company says its dividend will grow 4% to 5% per year, potentially less than half the 9.9% compounded annualized growth rate it has delivered over the past decade.

Brookfield Infrastructure's diversity is its strength

While Emera has focused intently on Florida, Brookfield Infrastructure operates in 17 countries, owning electric utility and distribution assets; transportation infrastructure including railroads, highways, and ports; energy assets including natural gas gathering and distribution; telecommunications infrastructure including fiber, cell towers, and data centers; and water distribution, desalination, and irrigation assets.

In other words, it's a far more diverse business than Emera. On the one hand, this diversification could be problematic. Each sector adds more complexity -- both regulatory and technical aspects -- that calls for more resources to support. And this could cause a drag on the results.

On the other hand, these five sectors offer massive long-term growth potential, both from the need to modernize existing assets in developed economies and the need for more to support a burgeoning global middle class. Over the next decade, the global urban population will add about 1 billion new members, and Brookfield Infrastructure is positioned to be a big winner from that growth.

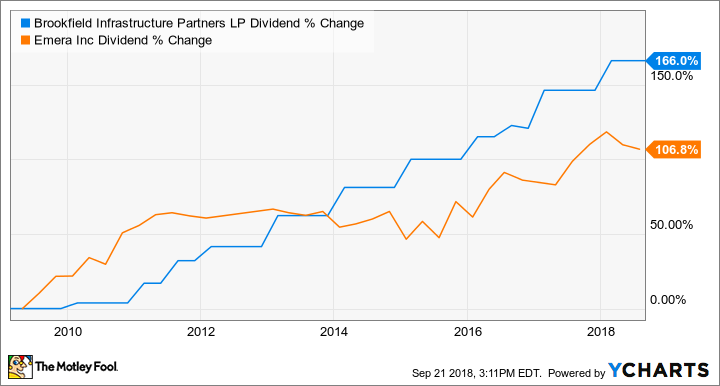

Furthermore, its management has proven incredibly capable of generating shareholder returns. Since instituting a quarterly payout shortly after going public in 2009, Brookfield Infrastructure has delivered far-superior dividend growth:

BIP Dividend data by YCharts.

Furthermore, its long-term goal of growing the payout 5% to 9% per year remains unchanged (and higher than Emera's).

Despite Emera's higher yield, Brookfield Infrastructure is the better buy

If you're an income investor simply shopping for the biggest paycheck you can get today, I wouldn't fault you for buying Emera. It's a solid utility that's smartly investing in a great growth market in Florida, and that should pay off over time, though its payout will likely grow at a slower rate going forward than it has in the past.

But if you're thinking more about the long-term prospects, and are more focused on your total returns, I think Brookfield Infrastructure should make for the superior investment. Not only does it participate in far more markets than Emera, but its recent moves into water and data/telecommunications should lead to substantially more growth opportunities.

And while that complexity can add more risk since there are more things that can go wrong, Brookfield Infrastructure's management has proven incredibly talented at both having the best operators and at allocating capital to deliver fantastic returns. And I expect that's going to remain the case going forward, and investors will continue to earn market-beating total returns.