What happened

Elastic (ESTC +0.34%) stock benefited from market momentum in November and recovered from a sell-off that hit the cloud-software space in October. Shares gained 10.3% last month, according to data from S&P Global Market Intelligence.

Cautious outlooks from tech companies including Workday and Cisco and a slew of downgrades for major companies in the enterprise software space prompted the clipping of valuations for high-flying cloud services companies including Elastic in October. Momentum for the broader market helped the stock recover last month, and shares are now up roughly 6% on the year -- and roughly 111% from the company's market debut in October 2018.

Image source: Getty Images.

So what

There wasn't much in the way of business-specific news behind the software-as-a-service (SaaS) company's recovery last month. Elastic announced a new nominee for its board of directors and published a press release stating that it would have a presentation at the Barclays Global Technology, Media and Telecommunications Conference in San Francisco on Dec. 12, but the stock's November gains appear to have stemmed almost entirely from a broader rebound for cloud services companies.

Now what

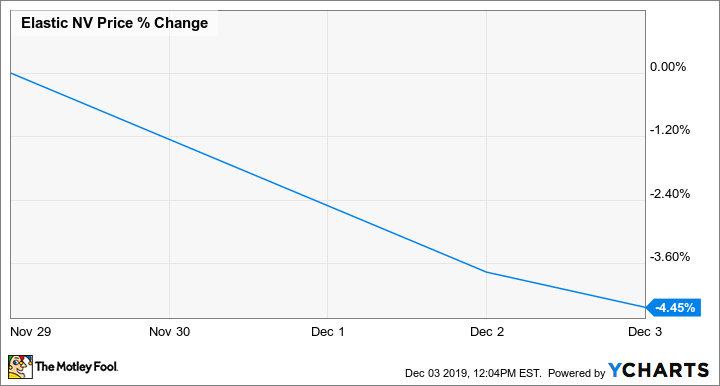

Elastic shares have given up some of their gains amid a sell-off for the broader market early in December. The open source enterprise software company's shares are down roughly 4.5% so far in this month's trading.

Elastic is set to report second-quarter earnings after the market closes on Dec. 4. The company is guiding for sales in the quarter to come in between $95 million and $97 million. Hitting the midpoint of that target would mean achieving sales growth of 51% year over year. The company's non-GAAP (adjusted) loss per share for the period is projected to come in between $0.30 and $0.32.

For the full-year period, Elastic is guiding for sales between $406 million and $412 million -- representing year-over-year growth of 51% at the midpoint of the target. Management expects adjusted losses per share for the year to be between $1.24 and $1.40.

The company is valued at roughly 14.7 times this year's expected sales.