Few companies have affected the consumer's daily life more than Amazon (AMZN +0.67%) has over the past two decades. The business has grown from an online book store to a one-stop-shop for almost every item. Prior to Amazon Prime, two-day shipping was a luxury no one knew they needed. Now it's difficult to live without.

Amazon has expanded to grow much beyond its original e-commerce business. It has a cloud infrastructure business in Amazon Web Services (AWS), an entertainment wing, as well as multiple hardware brands. With all this expansion, investors may be wondering if Amazon has any room left to grow at a pace that can keep producing outsized stock returns. While I don't have a crystal ball, I think Amazon's recent financial results give investors a good idea of whether now is the right time to buy.

Image source: Getty Images.

Slowing retail sales growth

It doesn't require much critical thinking to understand how Amazon's e-commerce business benefited from the pandemic. Now it is coming against tough comparisons. For 2021's fourth quarter, North American sales only grew 9%, and international sales actually fell 1% year over year. While these two segments were profitable from an operating income standpoint during last year's quarter, each lost money in 2021's Q4.

NASDAQ: AMZN

Key Data Points

During its Q4 earnings call, CFO Brian Olsavasky said the company experienced $4 billion in costs due to inflationary pressures. He cited wage increases, higher pricing for third-party delivery, and labor constraints as reasons for the loss. However, Amazon also announced a $20 price hike to its Amazon Prime subscription service. With more than 200 million Prime members worldwide, that would equate to a $4 billion rise in pure income for Amazon.

This is the first time since 2018 that Amazon raised its Prime prices, so consumers shouldn't be too concerned, especially with added services like Amazon Pharmacy or Prime Gaming. The price hike should also conveniently offset the costs due to inflation.

Slowing sales growth and loss of profitability are two things investors never want to see when evaluating a business. However, Amazon is taking an active approach to ensure these losses don't become permanent.

The best division within Amazon

The segment that is thriving within Amazon is AWS. And AWS's performance is the best reason to purchase shares of Amazon. According to Statista, AWS commands a massive 33% share of global cloud infrastructure spending, leading second-place Microsoft Azure which has a 22% share. Purchasing the market share leader has been a historically successful investment philosophy, especially when the business continues to innovate and grow.

For the full year, Amazon's AWS sales grew 37% to $62.2 billion (about 13% of Amazon's total revenue). The real kicker with AWS is its extreme profitability when assessed from an operating margin standpoint.

| Segment | Full-year Operating Margin |

|---|---|

| North America e-commerce | 2.6% |

| International e-commerce | (0.7%) |

| AWS | 29.8% |

Source: Amazon

AWS is the primary driver of both profits and revenue growth for Amazon. If this business continues to grow and succeed, then the stock will follow suit. However, if AWS loses market share, then Amazon investors might reconsider owning shares.

Image source: Getty Images.

The odds of this happening are low. AWS is the most in-demand cloud infrastructure provider, and management will ensure it maintains its leadership through incentives and innovation. Over 26,000 people attended AWS's re:Invent conference in person where more than 115 new services and features were announced, showing how important AWS is in cloud infrastructure.

The impending stock split

On March 9, Amazon's management announced the company would be splitting its stock 20-for-1 effective on June 3. While a stock split is mostly cosmetic, it does provide some short-term boosts. First, investors without access to fractional shares can purchase the stock without overweighting their portfolios. Second, Amazon may become a candidate to enter the Dow Jones Industrial Average as the index is price-weighted and a nearly $3,000 stock would throw the index out of balance.

The stock split is far from a reason to buy -- unless the stock has been out of reach because of its high price and you have a brokerage that doesn't offer fractional shares -- but it isn't a reason to sell either.

An attractive valuation

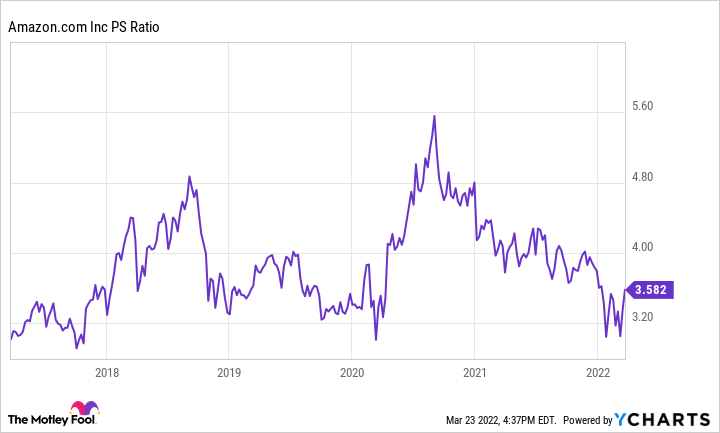

Amazon should be assessed from a price-to-sales standpoint as its profitability has gone up and down.

AMZN PS Ratio data by YCharts.

While off its recent low, 3.5 times sales is fairly standard for Amazon's stock over the past five years. Because of this, investors can feel confident they aren't buying Amazon at nosebleed valuations.

While the trend in the e-commerce business is a little concerning, it's likely more a reflection of some lingering effects of the ongoing pandemic and Amazon's response to it. Countering it is the fact that AWS shows no signs of slowing down. Amazon's management won't let its e-commerce dominance and profitability slip away, so within a few years profits should return to normal levels. At a decent valuation, I think Amazon stock is a buy now -- as long as it's purchased with the idea of holding the stock for at least three to five years to give it time to succeed.