PepsiCo (PEP +1.16%) reported earnings for its fiscal 2024's second-quarter last Thursday morning. While the stock initially sold off, it recovered as the day progressed and was up 1.5% on Friday.

Still, Pepsi remains down year to date despite significant gains in the major indexes. Read on to learn about some of the challenges impacting the business and why the dividend stock is worth buying anyway.

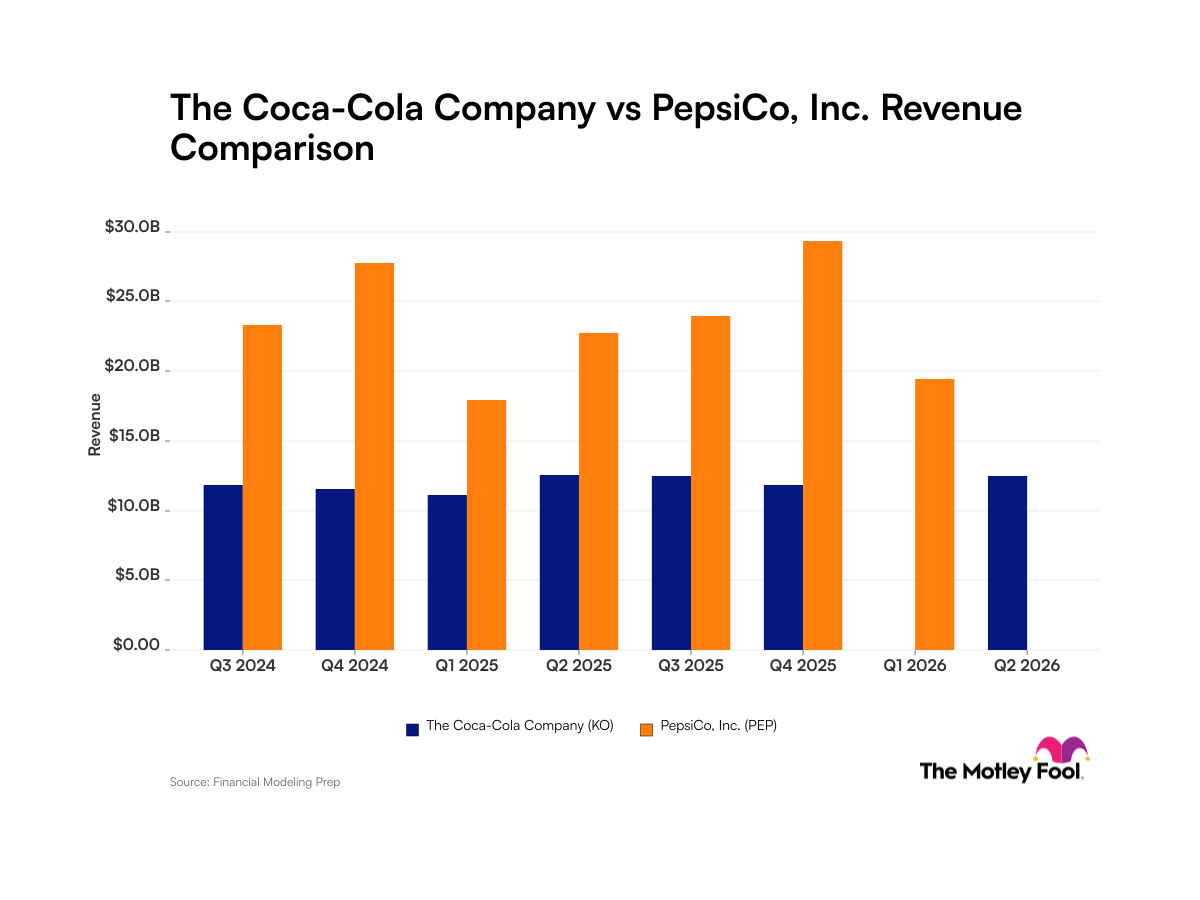

Image source: Getty Images.

Pepsi's in a pickle

Pepsi has done a masterful job managing costs and exhibiting pricing power throughout the last few years of supply-chain headaches and inflation-induced headwinds. But there's no sugarcoating the fact that Pepsi is now seeing volume declines across its key segments. Retailers can grow earnings in three major ways:

- Increasing the number of products they sell

- Changing the price it sells them for

- Reducing costs associated with selling the products

Pepsi is missing the first part of this equation, and that's arguably the single biggest factor holding back the stock price over the last three years. The company's price hikes worked -- at least, for a while. But we're starting to see some major consumer pushback, as exhibited by recent sales-volume data.

Volume declined across Pepsi's North American business segments, including a whopping 17% decline in Quaker Foods, a 4% drop in Frito-Lay, and a 3% decline in PepsiCo Beverages.

The company is guiding for 4% organic revenue growth for full-year fiscal 2024. And with the first half of Pepsi's fiscal-year's results in the books, analysts are rightfully skeptical of the company's ability to get there, given the volume declines.

On the earnings call, Morgan Stanley analyst Dara Mohsenian pointed out that second-half revenue would have to show mid-single-digit growth to reach the 4% goal. He asked how Pepsi planned to achieve accelerated growth amid a challenging operating environment.

Pepsi CEO Ramon Laguarta pointed out that Pepsi initially hoped to get 5% organic revenue growth on the year but has since tempered expectations. He also said that Quaker is recovering from supply-chain disruptions that would be resolved by the fourth quarter and help the segment return to growth. Plus, Pepsi's international business has been doing fairly well and is seeing higher volumes, which Pepsi expects will continue.

Laguarta also discussed Pepsi's targeted sales and marketing efforts, which it's using to cater to cost-conscious consumers. He highlighted Pepsi's strong July 4th promotions and some encouraging data points that investors would hear about when Pepsi reports its third-quarter results. The key takeaway was that Pepsi recognizes that the consumer is stretched thin and needs to stall or even lower prices in categories where there's room to do so to get volumes back up.

Pepsi is far from the only consumer goods company that's shifting its focus toward higher sales volume. McDonald's stock is also near a 52-week low and has seen pushback to further price increases. To restore value to its brand, McDonald's has introduced a $5 meal deal to boost traffic.

Margins may take a hit in the short term. Overall, however, the goal of companies like Pepsi and McDonald's is to change consumer perception from viewing their products as overpriced to viewing them (or at least certain items) as a good deal in a higher-price environment.

Pepsi investors should watch the relationship between sales and margins in the second half of this fiscal year. If North American volumes improve as Pepsi expects, but margins take a hit, that could be a net negative. In other words, what will be the cost of Pepsi achieving its 4% organic growth goal -- if it achieves it at all?

An attractive dividend and valuation

Pepsi could turn things around fairly quickly, especially if consumer spending picks up. Still, given the uncertainty, investors will want to ensure they get a good value for the stock.

PEP PE Ratio data by YCharts.

As you can see in the chart, Pepsi tends to be a premium-priced stock with its medium-term and long-term median price-to-earnings (P/E) ratios all over 26. However, its current P/E ratio is just 25 and its forward P/E is 20.4 -- suggesting Pepsi is a good value right now. This makes sense because the stock price has languished.

You may be wondering why a low- to moderate-growth business like Pepsi deserves a valuation this high. Pepsi has a diversified and global food and beverage business that's resistant to recessions. Management and analyst commentary tend to revolve around a percentage point or two change in performance, not drastic ebbs and flows in business. It's this consistency, paired with the strength of Pepsi's dividend, that makes it such a safe stalwart.

Pepsi is a Dividend King -- an elite category of companies that have paid and raised their dividends for at least 50 consecutive years. On top of that track record, Pepsi sports a yield of 3.3% -- which is significantly higher than the S&P 500 average yield of 1.3%.

It's rare to find a company with a history of dividend raises and a high yield. For example, fellow consumer staples Dividend King Procter & Gamble has a yield of 2.4%, and Walmart, another super-safe stock, has a yield of just 1.2%.

Buy Pepsi stock for a lifetime of passive income

Pepsi has its challenges, but they're understandable, given what other consumer goods companies are dealing with now. Pepsi's inexpensive valuation and dividend, which blends quantity and quality, make it a particularly compelling income stock to consider today.

Still, some investors may want to take a wait-and-see approach to the stock and monitor how Pepsi's margins will react to more promotions and marketing. There's little Pepsi can do if the consumer remains pressured for a prolonged period, which could eventually weigh on volumes and profitability.

Investors with a long-term time horizon should focus more on where Pepsi will be three to five years from now, rather than get too caught up in its near-term results. With that in mind, Pepsi stands out as an excellent dividend stock that can fuel your portfolio with passive income for years, if not decades, to come.