After selling off this past summer, Dow Jones Industrial Average component Visa (V +3.73%) has rallied almost 10% during the past month. Here's why the financial stock just reached a new all-time high and has the potential to keep going.

A numbers game

Visa generates revenue every time one of its debit or credit cards is swiped, tapped, or processed on mobile, desktop, or in person. The company's fee structure allows it to benefit from both the frequency and volume of transactions. The company also has a growing international business, which has allowed travelers to process transactions securely and avoid manually converting currencies.

Image source: Getty Images.

Visa's price-to-earnings ratio (P/E) is almost 31, which is lower than its median P/E during the past three, five, seven, and 10 years.

V PE Ratio data by YCharts.

Add it all up, and Visa is a great value, even after its recent run-up.

Visa is a "safe" stock

Unlike other growth stocks that are priced for perfection, Visa's earning can continue growing at a high-single-digit to low-double-digit percentage pace, thanks to the benefits of network effects and its growing global reach. It doesn't depend heavily on economic cycles or strength in a particular end market or industry.

This is a particularly compelling advantage, compared to cyclical sectors. For example, if artificial intelligence (AI) spending slows, it could cause a major downturn across the semiconductor industry. If economic growth slows, cyclical industrial or consumer discretionary companies can get hit hard. If oil prices take a hit, oil and gas companies may see slowing or even negative profits.

Granted, some companies are much better positioned to handle cyclical slowdowns, even in vulnerable industries. But Visa is in a different category. It has proven that its earnings can steadily grow even amid inflation, higher interest rates, or recession fears.

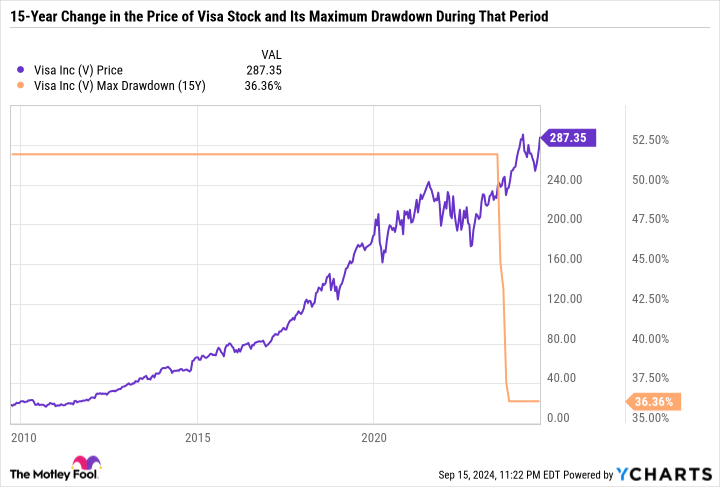

Perhaps most impressive is the stock's relative lack of volatility. During the past 15 years, Visa has gone from less than $20 a share to just over $287. And through it all, its biggest drawdown was just 36%.

A drawdown is a stock's decline from a high. This means that holding Visa during this period would have increased your money more than 15-fold, and the worst it sold off for was a little more than a third from the high.

That consistent track record stacks up against even the safest stocks on the market. For example, Coca-Cola, which is known for its recession-resistant business and growing dividend, had a maximum drawdown of 37% during the same 15 years -- nearly identical to Visa.

Visa blends growth and value

Stocks like Visa are often referred to as dividend growth stocks because they combine earnings growth with market-beating historical returns and regularly increase their dividends. Buying and holding a quality dividend growth stock can be a recipe for impressive long-term gains and steady passive income.

Companies can allocate capital in a variety of ways. For example, Amazon and Tesla don't pay dividends and prefer to reinvest money into their businesses. Some companies, like Adobe, don't pay dividends but repurchase their stock to offset dilution from stock-based compensation and return value to shareholders. Other companies distribute most of their earnings to investors through dividends, like many utilities or consumer staples companies.

Visa has a hybrid capital allocation model. It raises its dividend and buys back stock -- but not to the point where it can't invest in the core business. Not every company has the earnings and cash flow to support this capital allocation strategy. But some of the best companies, like Apple, Microsoft, and recently Alphabet and Meta Platforms, use a capital allocation model similar to Visa's.

NYSE: V

Key Data Points

A good way of making sure a company is truly a dividend growth stock and not just a dividend stock with a low yield is by looking at the payout ratio. Visa has a payout ratio of just 21.5% -- meaning it spends about $0.22 for every dollar in earnings on dividends.

Visa spends substantially more on buybacks than dividends. Even so, Visa has paid and raised its dividend every year since 2009.

Although Visa yields just 0.7%, it could afford a much higher dividend if it decided to reduce buybacks and reinvestments in the business. Again, Visa doesn't need to do that, but it's a good theoretical exercise that proves why an excellent stock can have a lower yield for a good reason.

Visa can be a lifelong holding

It's a common mistake to look at a stock's price and use it as a measuring stick to determine whether it's overvalued or a good buy. But companies aren't valued in the same way as goods and services.

Visa is a good example of why a quality company at an all-time high can still be worth buying. The stock is a great value, built to last, and can do well during an economic slowdown. Visa is one of those rare stocks that will appeal to a variety of investors -- regardless of their risk tolerance or investment time horizon.