Huntington Ingalls Industries (HII +2.22%) has emerged as a stock market outperformer in 2025, rewarding shareholders with a solid 21% return year to date as of this writing.

The defense contractor, recognized as the largest military shipbuilder in the United States, is set to capitalize on several growth tailwinds. The new Trump administration has proposed increased funding for domestic shipbuilding programs, which directly benefits the company's unique market positioning. The company's outlook is further bolstered by an extensive order backlog set to drive increasing earnings.

Here are four reasons I believe shares of Huntington Ingalls are a great buy for your portfolio now.

Image source: Getty Images.

1. A critical leader in national security

U.S. Navy aircraft carriers and nuclear-powered submarines are modern engineering marvels of unparalleled complexity, with Huntington Ingalls Industries leading innovation in the field. The company's Newport News Shipyard is the only U.S. facility capable of constructing Gerald R. Ford-class aircraft carriers, among the most technologically advanced warships globally.

Huntington Ingalls' shipbuilding division also constructs Arleigh Burke-class destroyers and San Antonio-class amphibious ships, essential for surface combat and troop deployment. Additionally, the company's Mission Technologies division develops uncrewed undersea vehicles (SUUV) like the Lionfish, alongside cybersecurity solutions and AI-driven autonomous systems, highlighting its diverse defense offerings.

This critical role in producing key defense assets positions Huntington Ingalls as an indispensable partner to the U.S. Department of Defense, enhancing its appeal as a potential investment.

2. Trump's defense agenda is powering the outlook

A major theme in the new Trump administration has been revitalizing U.S. military strength to counter China's advancements in high-tech systems like hypersonic missiles and AI-enhanced naval technologies.

President Trump outlined plans to boost shipbuilding for national security and economic growth during a joint address to Congress in February. This was followed by an Executive Order in April titled "Restoring America's Maritime Dominance" aimed at strengthening domestic shipbuilding capabilities, enhancing maritime workforce training, and ensuring adequate commercial vessel capacity for national security. Huntington Ingalls Industries should benefit from these policy directives.

With a current $48 billion order backlog, Huntington Ingalls Industries now expects more than $50 billion in additional awards in the next 20 months, adding to its growth runway and earnings potential.

NYSE: HII

Key Data Points

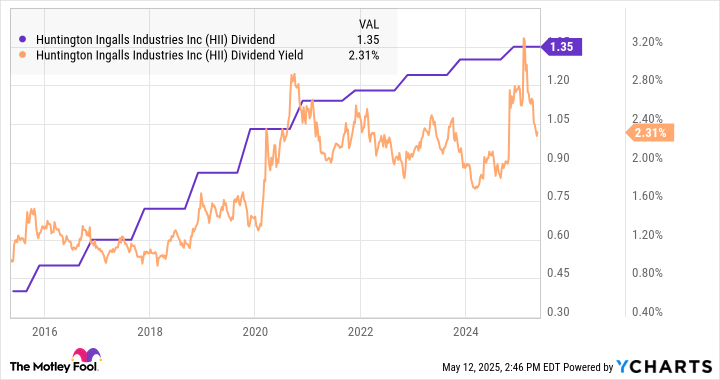

3. Dividend growth outlook

In the first quarter (for the period ended March 31), Huntington Ingalls reported revenue of $2.7 billion, representing a decline of 2.5% year over year, reflecting the uneven timing of large orders. Nevertheless, earnings per share (EPS) of $3.97 surpassed Wall Street estimates, driven by higher margins. Looking ahead, the company is guiding for full-year shipbuilding revenue between $8.9 billion and $9.1 billion, at the midpoint, implying an increase of 3% from 2024, with several milestone ship deliveries planned through 2026.

Perhaps the biggest development for Huntington Ingalls is its recent acquisition of a new production site near Charleston, South Carolina. The facility is expected to enhance overall capacity by 20% from 2024 company levels, setting the stage for stronger top-line growth into the next decade. According to Wall Street analysts, from the current 2025 EPS estimate of $13.92, roughly flat from last year, the 2026 forecast of $16.21 points to a 16.5% increase next year. That's great news for investors eyeing the sustainability of the company's $1.35 per share quarterly dividend, yielding 2.31%. Huntington Ingalls has increased its annual dividend payment for the past 13 years, with room for more growth going forward.

HII Dividend data by YCharts

4. A compelling valuation

Where Huntington Ingalls Industries stands out is through its attractive valuation, trading at 16 times its consensus 2025 EPS as a forward price-to-earnings (P/E) ratio. This level represents a discount to defense sector peers, including companies like RTX, Lockheed Martin, General Dynamics, and Northrop Grumman, which, as a group, trade at an average forward P/E closer to 19. With a renewed strategic focus on military seapower and naval technologies, Huntington Ingalls' stock may be undervalued.

HII PE Ratio (Forward) data by YCharts

The big picture for investors

I'm bullish on Huntington Ingalls Industries and believe all the pieces are in place for its share price rally to keep going. The stock is a great option for investors to add to diversified portfolios and gain exposure to high-level themes in domestic manufacturing and the defense sector.