A lot has changed about Occidental Petroleum (OXY 0.86%) since around 2020. Some of the changes were good and some weren't, though how you view the company may depend a little bit on your approach to investing.

Occidental Petroleum has some very well-known supporters, but does that make it a buy while the shares trade below $45?

What does Occidental Petroleum do?

Occidental Petroleum, which is usually just shortened to Oxy, is a large business, with a market cap of around $40 billion. However, large is a relative term, as that valuation is relatively small compared to the largest players in the energy sector. For instance, industry giant ExxonMobil (XOM +1.38%) has a market cap of around $440 billion.

Image source: Getty Images.

This difference actually plays an important role in whether or not you might want to buy Oxy stock today. That's because ExxonMobil is one of the largest integrated energy companies on the planet. And Oxy is basically trying to grow to a point where it can compete with companies like ExxonMobil. The primary route that Oxy has used to grow its business of late has been acquisitions.

The process started to ramp up in 2019 when Oxy bought Anadarko Petroleum. With the financial support of Warren Buffett and Berkshire Hathaway (BRK.A 0.30%)(BRK.B +0.00%) it managed to steal Anadarko away from Chevron (CVX +1.80%). But the deal led to a sea change for Oxy because it leaned heavily on debt to get the Anadarko deal done. When oil prices plunged during the coronavirus pandemic, it was forced to cut its dividend and refocus its financials around debt reduction.

NYSE: OXY

Key Data Points

Occidental Petroleum is a growth play in a volatile industry

To Oxy's credit, it has dramatically improved its financial situation concerning its balance sheet. Its debt-to-equity ratio rose to nearly 2x following the Anadarko deal but is now down to around 0.7x. And it has inked two more acquisitions since it completed the Anadarko acquisition, so it has been much more prudent about its purchases. That's a good thing.

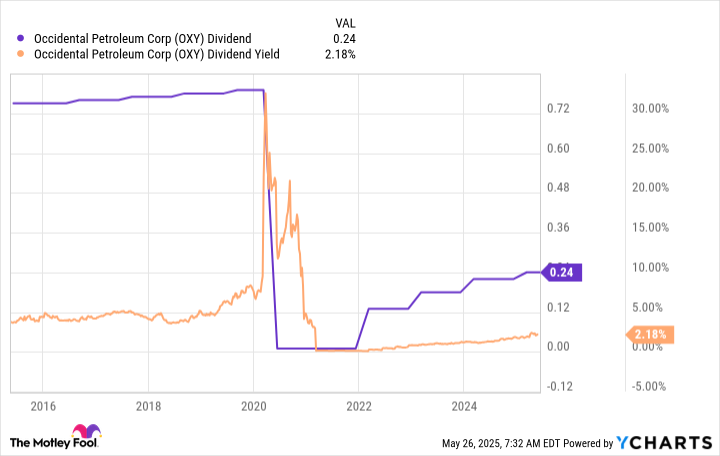

But the dividend remains well below where it was prior to the dividend cut. What's interesting is that the dividend yield remains notably lower, as well. This is basically a function of the market recognizing that Oxy is taking a different approach with its business. It is now more focused on growth. That's not a bad thing, but it is very different from what you will get from industry giants like ExxonMobil and Chevron. These two integrated energy companies lean more toward reliable dividends despite operating in a volatile industry.

Data by YCharts.

From a top-level perspective, Oxy's financial performance and stock price will always be impacted heavily by the often volatile prices of oil and natural gas. That's no different than what you'd end up facing with ExxonMobil or Chevron. However, when you dig a little bit deeper, Oxy is more growth-oriented than ExxonMobil or Chevron, and that creates both opportunity and risk.

Even with the financial support of Berkshire, Oxy got out over its skis with the Anadarko transaction. Although it has been more prudent since that point, the misstep shows that execution is vital to Oxy's growth approach and, importantly, that it hasn't always executed at a high level. Investors took the brunt of the hit, noting the steep stock price decline and dividend cut that were the fallout. An investment in ExxonMobil or Chevron probably won't expose you to the same kind of risk, or at least not at the same level, given their larger scales.

Should you buy Oxy or a larger oil company?

It is interesting to note that Buffett (through Berkshire) owns both Oxy and Chevron stock. That basically means he is invested in an industry giant that produces reliable dividends and a smaller peer that is focused on growth. That could be the best option for long-term investors looking at the energy sector more broadly. But if you have to choose just one investment, Oxy is the riskier choice and the one that likely has more long-term upside.

If you choose to buy Oxy, however, go in knowing two important facts. First, no energy producer can fully avoid the impact that commodity prices will have on its business, which is why Oxy's price is below $45 today. And, second, Oxy's focus on growth increases risk in a sector that is already on the risky side. The second factor here should be the one you pay the most attention to if you plan to own whatever energy stock you buy for the long term.