Buying and holding companies for the long term is a mindset that every investor should adopt. The goal of long-term investing is to identify the best companies and hold them until they're no longer exceptional, thereby generating a substantial profit along the way. Some stocks have more robust investment cases than others, but one that I particularly like is Taiwan Semiconductor Manufacturing (TSM 0.27%).

I've got 10 reasons why it's an excellent stock to buy now and hold forever, as it looks like a stellar deal.

Image source: Getty Images.

1. Strong client base

Taiwan Semiconductor is the world's leading contract chip manufacturer, with clients such as Nvidia (NVDA +0.47%) and Apple (AAPL +0.26%) at the top of its customer list. You'd be hard pressed to find a high-end device without chips from TSMC.

Furthermore, TSMC is the sole supplier for many of these chips, which solidifies its position and makes it difficult to replace.

2. Continuous innovation

One of the reasons big names in the tech space have chosen Taiwan Semiconductor as a partner is its culture of constant innovation. Taiwan Semiconductor has consistently launched cutting-edge products year after year, and is slated to do so again.

Later this year, Taiwan Semiconductor will launch its 2 nanometer chips, and in 2026, it will launch its 1.6nm chips. Nobody in the world has these chips available yet, and TSMC will likely be the first to offer them to clients.

NYSE: TSM

Key Data Points

3. Excellent yields

Part of TSMC's dominance stems from its high chip yields. While there isn't concrete information available on this topic, it's widely known that many chip foundries have struggled to produce leading 3nm chips (with yields often cited in the 50% range). TSMC has delivered yields of 90% or greater, resulting in lower scrap costs and a more favorable price for the client.

As long as TSMC can maintain its excellent yields, it will continue to differentiate itself from the competition.

4. Expanding footprint

One concern about Taiwan Semiconductor is its proximity to mainland China. Taiwan's politics are incredibly complex, and there is a persistent fear of China's potential takeover.

However, TSMC is working to mitigate this threat by establishing new production facilities worldwide. It is spending $165 billion in the U.S., as well as building facilities in Japan and Germany. By diversifying away from the island of Taiwan, the risk of a single point of failure is reduced.

5. China isn't as much of a risk as you may believe

Although the China threat is real, because of TSMC's global customer base, it's hard to envision a scenario where the entire market doesn't crash if Taiwan is attacked. This action could potentially plunge the world's superpowers into a war, in which case almost no stock would be safe.

This makes me fear military action against Taiwan less. The domino effect of an attack would be catastrophic, and that should deter China from taking such aggressive action.

6. Massive five-year growth projections

Barring any world-changing events, TSMC's management is excited about its growth prospects. For the next five years, it expects AI-related revenue to grow at 45% compound annual growth rate (CAGR). As for total revenue, it expects revenue to increase at nearly a 20% CAGR.

That's huge growth, and showcases how strong of an investment Taiwan Semi can be over the next few years.

7. Fantastic long-term outlook beyond

While management isn't offering guidance beyond the five-year time frame, it's hard to imagine a world where we're using less technology. As a result, TSMC's chips will always be in high demand due to its leadership position, giving it a rosy long-term outlook.

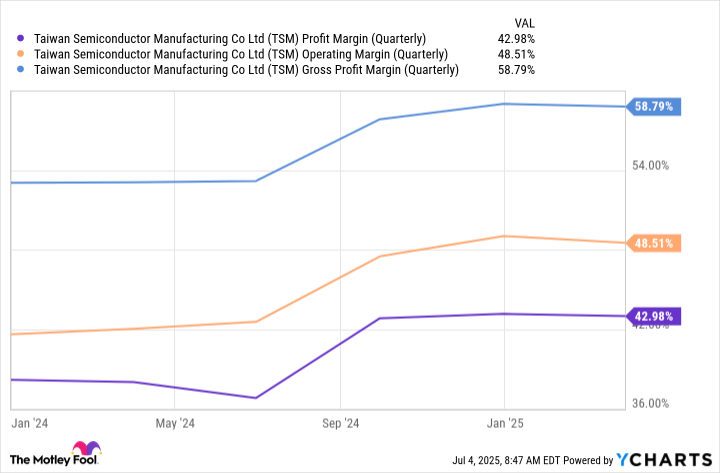

8. Excellent margins

Taiwan Semiconductor also delivers incredible profit margins.

TSM Profit Margin (Quarterly) data by YCharts

Most companies dream of having a profit margin greater than 40%, yet Taiwan Semiconductor consistently achieves that. This results in substantial cash flows, enabling it to reinvest in the business, repurchase stock, or distribute dividends.

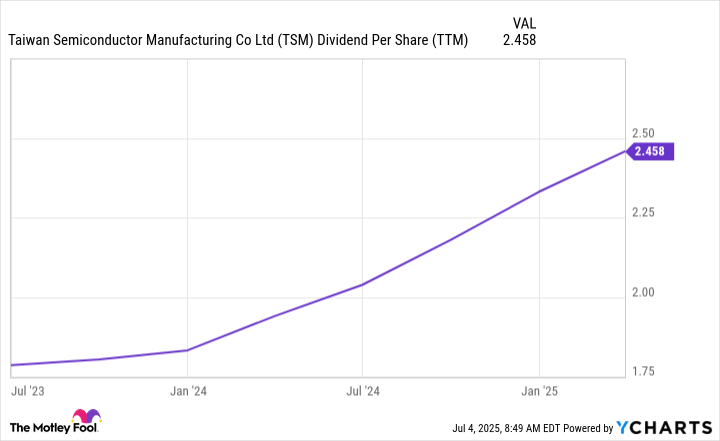

9. Growing dividend

While Taiwan Semiconductor may not be the world's best dividend company, it offers a solid 1.2% yield and has consistently increased its payout over the past few years.

TSM Dividend Per Share (TTM) data by YCharts

Over time, this dividend payout could become a substantial part of the TSMC investment thesis, further supplementing the company's massive chip growth.

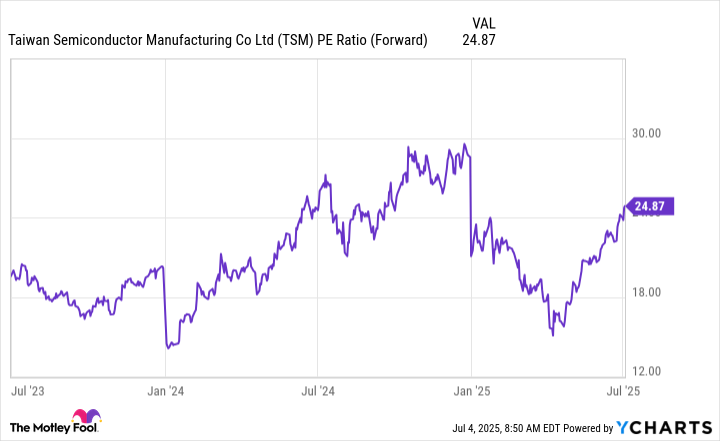

10. The stock isn't overvalued

TSMC is an excellent buy today. The stock trades at 24.9 times forward earnings, which isn't significantly more expensive than the broader market, as measured by the S&P 500 (^GSPC 0.19%), which trades at 23.2 times forward earnings.

TSM PE Ratio (Forward) data by YCharts

Considering that Taiwan Semiconductor is projected to significantly outgrow the market over the next few years, this seems like a fair price to pay for a company with fantastic long-term potential.