For a few years now, the artificial intelligence (AI) movement has largely hinged on the performance of a single company: Nvidia (NVDA 1.06%).

Sure, if Microsoft or Amazon posted strong results from their respective cloud computing platforms or if Tesla managed to hype investors up over the prospects of self-driving robotaxis or humanoid robots, the technology sector might see a fleeting upward movement. At the end of the day, however, the focus seemed to eventually return to Nvidia -- with analysts obsessing over how demand for the company's chips and data center services were trending.

During the first half of the year, Nvidia's ship was caught in an epic storm. Investors started to question the company's long-growth prospects -- inspiring prolonged periods of panic-selling in the process. All told, Nvidia's market cap dropped by more than $1 trillion.

But now, with a market value north of $4 trillion, Nvidia has reclaimed its position as the most valuable company on the planet. Even better? Some on Wall Street are calling for further gains of up to 400%.

Let's explore the tailwinds supporting Nvidia's long-term growth narrative and detail why Wall Street sees such massive upside for the king of the chip realm.

NASDAQ: NVDA

Key Data Points

One Wall Street analyst is calling for a $10 trillion valuation for Nvidia

One of the most bullish Nvidia analysts on Wall Street is the I/O Fund's Beth Kindig. Kindig suggested that Nvidia could reach a $10 trillion market cap by 2030 -- implying 140% upside from current levels. Let's explore the main catalysts supporting Kindig's forecast.

According to management from Microsoft, Amazon, and Alphabet, roughly $260 billion will be spent in 2025 alone on AI infrastructure. On top of that, Meta Platforms is expected to spend roughly $70 billion on capital expenditures this year -- nearly double what it spent in 2024. Lastly, Oracle is beginning to make significant headway in infrastructure services -- allowing companies to rent Nvidia GPUs from their cloud-based data center platform. From a macro perspective, rising capex from the cloud hyperscalers bodes well for chip demand.

Kindig takes these secular tailwinds one step further, suggesting that competition from Intel and Advanced Micro Devices does not pose much of a threat to Nvidia's dominance. While it's hard to know how vendor preferences could change over the next several years, current industry research trends suggest that Kindig might be right -- underscored by Nvidia's rising market share in the AI accelerator industry.

The area of Kindig's analysis that I think is currently overlooked the most revolves around Nvidia's software architecture, called CUDA. Since CUDA is integrated tightly with Nvidia's hardware, developers essentially become locked into the company's ecosystem.

Not only does this lead to customer stickiness, but it opens the door for Nvidia to be at the forefront of more sophisticated, evolving AI applications in areas such as robotics and autonomous driving.

Image source: Getty Images.

What about $20 trillion?

Former management consulting executive Phil Panaro is even more bullish than Kindig. By 2030, Panaro thinks Nvidia's share price could reach $800 -- implying roughly a $20 trillion market cap.

Panaro cites opportunities across Web3 development and evolving use cases around how enterprises and governments leverage AI to generate more efficiency and cost savings as the main pillars supporting Nvidia's upside.

While these trends could eventually drive significant demand for Nvidia's data center services, tech adoption within the government tends to move slowly. Meanwhile, Web3 remains an emerging concept that could take far longer to mature than Panaro is assuming.

Is Nvidia stock a buy right now?

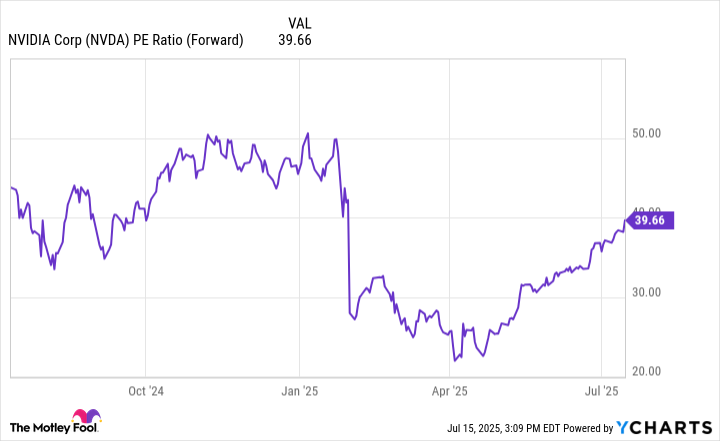

Nvidia stock has been mounting an epic comeback over the last couple of months. This valuation expansion can be easily seen through the dynamics of the company's rising forward price-to-earnings (P/E) multiple. Nevertheless, Nvidia's forward P/E of 40 is still well below levels seen earlier this year.

NVDA PE Ratio (Forward) data by YCharts

Trying to model Nvidia's peak valuation is an exercise in false precision. The bigger takeaway is that analysts on Wall Street are not only calling for significant upside in the stock, but they have outlined the foundation for Nvidia's long-term growth. The important theme here is that Nvidia has opportunities well beyond selling chips -- many of which have yet to make meaningful contributions to the business.

I see Nvidia stock as a no-brainer. Investors with a long-run time horizon might consider scooping shares up at current prices and plan to hold on for years to come.