For the first time in a while, the autonomous driving discussion isn't revolving around Tesla or Waymo. On July 17, news broke that ridehailing platform Uber Technologies (UBER 3.60%) is partnering with electric vehicle (EV) manufacturer Lucid Group (LCID +2.04%) to help bring Uber's own robotaxi ambitions to life.

Following news of the deal, Lucid shares rose nearly 40%. Let's explore the mechanics of the deal with Uber and assess whether now is a good time for investors to get in on the action around Lucid.

NASDAQ: LCID

Key Data Points

How are Uber and Lucid working together?

Before diving into the mechanics of Uber's deal with Lucid, investors should first understand the company's business model. Similar to how Airbnb does not own or build the properties on its platform, Uber is not a traditional automobile business in that it does not manufacture or sell cars. Instead, Uber employs drivers who own (or lease) their cars and provide ridehailing and delivery services directly through an app.

While companies such as Waymo and Tesla continue to invest billions of dollars in developing self-driving car technology, Uber is getting involved in the robotaxi market through a series of strategic partnerships with car manufacturers and robotics specialists.

Now, Lucid will be joining the likes of Waymo, WeRide, Avride (owned by Nebius Group), and Serve Robotics in Uber's autonomous vehicle ecosystem.

Image source: Getty Images.

Per the terms of the deal, Uber will invest $300 million into Lucid to help the company build a reported 20,000 (or more) vehicles over the next six years. These vehicles will come equipped with autonomous driving software developed by Nuro, another Uber partner.

Is Lucid stock a buy now?

The table below breaks down production and delivery figures as well as gross profit trends for Lucid over the last year.

| Category | Q1 2024 | Q2 2024 | Q3 2024 | Q4 2024 | Q1 2025 |

|---|---|---|---|---|---|

| Production | 1,728 | 2,110 | 1,805 | 3,386 | 2,212 |

| Deliveries | 1,967 | 2,394 | 2,781 | 3,099 | 3,109 |

| Gross Margin | (134%) | (134%) | (106%) | (89%) | (97%) |

Data source: Investor Relations.

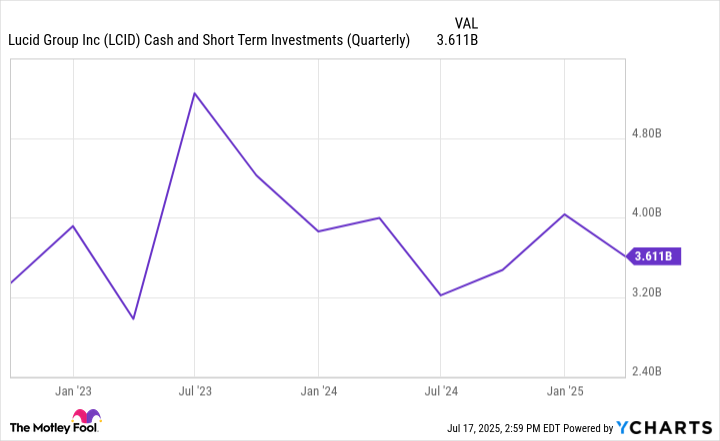

In the figures above, there are a few themes that are difficult to look past. First, Lucid's production and delivery figures have been inconsistent over the last several quarters. Moreover, like other budding EV manufacturers such as Rivian, Lucid is burning through heaps of cash.

LCID Cash and Short-Term Investments (Quarterly) data by YCharts.

In a way, I'm not sure I necessarily see Uber's $300 million infusion into Lucid as something to cheer about. Given the dynamics in the graph above, Lucid likely needs these additional financial resources in order to fulfill Uber's order backlog.

These poor unit economics are going to make it hard for Lucid to truly compete with more mature, technologically sophisticated businesses such as Waymo or Tesla in the long run. Moreover, building a fleet of 20,000 cars over six years doesn't exactly scream a sense of urgency -- especially when competition from platforms like Waymo and Tesla is heating up.

To me, this deal contains quite a bit of execution risk on Lucid's end. Additionally, it feels more like a pressure campaign by Uber, which seems steadfast in its approach to forge a number of partnerships in the autonomous vehicle market in an effort to compete more directly with Tesla -- which so far has shown little interest in collaborations.

While the prospects of becoming part of Uber's ecosystem are intriguing, the deal looks more like an exciting piece of PR for Lucid at the moment. Even though the upside of this deal could be transformative for Lucid in the long run, the company's roadmap still looks uncertain and speculative for the time being. For these reasons, I do not see the Uber partnership alone as a reason to buy Lucid stock right now.