Is it time to reset or reallocate your portfolio? Maybe you just need some new places for idle cash that's been slowly building up.

Don't sweat it. I think I can help. Here's a closer look at five stocks I've had an eye on for a while, all of which have become some of my top prospects. I think they'll work for plenty of other investors, too.

Image source: Getty Images.

1. PepsiCo

PepsiCo (PEP +0.87%) stock has dramatically underperformed shares of its rival Coca-Cola since late 2023, when lingering inflation turned downright painful.

Whereas Coca-Cola's business model largely punts expensive bottling operations to its third-party bottling partners, PepsiCo owns most of its manufacturing facilities, which were suddenly more expensive to operate.

It would also be naïve to pretend Coca-Cola doesn't have at least a little more pricing power than PepsiCo does, particularly in comparison to PepsiCo's Frito-Lay snack chip business.

NASDAQ: PEP

Key Data Points

However, while the backdrop put pressure on PepsiCo's profit margins, it was never the existential threat that the stock's 30% pullback from its 2023 peak suggests. The sell-off has done investors a huge favor, though. It's pumped this stock's forward-looking dividend yield up to 4.2%.That yield is also based on a dividend that has now been raised for 53 consecutive years.

2. AppLovin

Ever heard of AppLovin (APP 0.57%)? It would be a bit surprising if you had. It's anything but a household name. There's a good chance you or someone in your household has been exposed to its service, however.

AppLovin helps app developers advertise their apps. This description still understates what the company brings to the table, though. The company's turned digital marketing into an art and a science. From streaming TV to mobile apps and more, AppLovin helps marketers create, manage, and measure advertising campaigns.

Its target market clearly loves what it offers, if this year's projected top-line growth of more than 21% is any indication. This pace of revenue growth is also expected to last at least through 2027. This technology company is also profitable, and increasingly so. In fact, its per-share profits are expected to triple from last year's $4.53 to more than $14.00 per share by 2027.

There's been some drama, for the record. In March, short-selling specialist outfit Muddy Waters argued that AppLovin's advertising tech didn't actually work as effectively as it was said to. Shares tumbled on the news.

It's quite telling, however, that the stock has since more than reclaimed that lost ground.

3. Snap

When Snapchat parent Snap (SNAP 2.39%) went public in 2017, investors were understandably hesitant. Twitter (now X) and Meta Platforms' Facebook were well-entrenched by then, and still growing. The last thing the world seemed to need at the time was yet another social media platform. Investors needed an unprofitable one even less.

NYSE: SNAP

Key Data Points

A funny thing's happened in the meantime. Snapchat's continued to make forward progress in terms of revenue, profitability, and user headcount. Its first-quarter daily user tally of 460 million extends a slow and steady growth streak to another new record. Sales growth and progress toward consistent profitability remain equally impressive, firmed up by the company's willingness to consistently try new things, and learn from its failures as well as its successes.

What gives? It's arguably an underappreciated theory, but it's possible that more and more people are finding Facebook and X to be a bit too toxic, and increasingly so. It's easier for users to shield themselves from this noise with the Snapchat app.

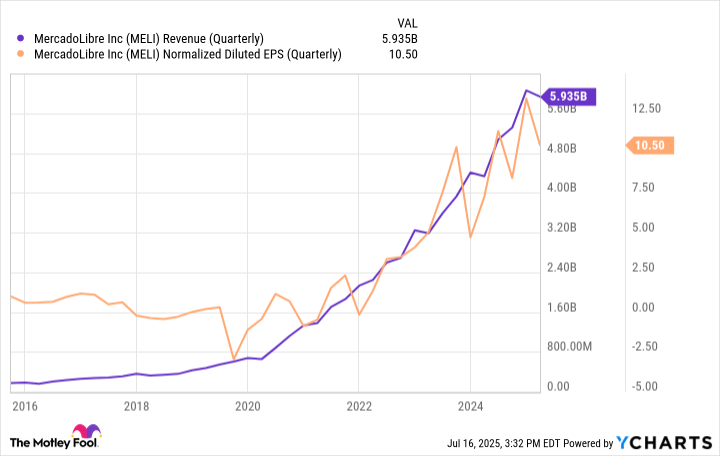

4. MercadoLibre

There's a good chance you've never heard of MercadoLibre (MELI 1.94%). Don't let that deter you. It's a fantastic growth opportunity.

MercadoLibre is often referred to as the Amazon of Latin America, by virtue of its e-commerce platform that serves the entire region. From payment processing to delivery logistics to technological tools for brick-and-mortar retailers, MercadoLibre is a turnkey solution for a bunch of South American consumer-facing businesses. Last year, its tech facilitated the sale of $51.5 billion worth of goods and services, and it also served as the intermediary for nearly $200 billion in digital payments. Both were well up from year-earlier comparisons.

MELI Revenue (Quarterly) data by YCharts.

This still only scratches the surface of its opportunity.

In many ways, Latin America's telecom landscape is where North America's was 25 years ago, when Amazon first began growing into a powerhouse. Research outfit Canalys reports that smartphone shipments to Latin America reached a record-breaking 137 million units just last year, in step with the region's now-rapid growth of wired and wireless broadband.

NASDAQ: MELI

Key Data Points

As was the case in North America, this access is driving strong interest in online shopping. A forecast from Payments and Commerce Market Intelligence predicts that the Latin American e-commerce market is set to double in size between 2023 and 2027.MercadoLibre is perfectly positioned to capture more than its fair share of this growth.

5. Alibaba

Last but not least, I'm adding Alibaba (BABA 1.82%) to my list of favorite stocks to buy right now.

Alibaba is parent to China's powerhouse e-commerce platforms Taobao and Tmall, which collectively control about half of China's online shopping market. Its e-commerce sites AliExpress and Alibaba.com -- largely aimed at customers outside of China -- don't boast the same sort of reach, but they're still respectable presences in their own right.

The company is much more than e-commerce. It operates a digital entertainment arm, a logistics service, and a cloud computing business that's developed a powerful AI-powered chat tool called Qwen that can be used -- and monetized -- in several different ways.

What about the tariff standoff that's part of a much bigger trade war being fought between the world's two economic superpowers? It may not matter nearly as much as you might think it should.

China (in general) and Alibaba (in particular) largely operate within silos that don't outright require superstrong relations with top trade partners. As evidence of this argument, after Alibaba's first-quarter top-line growth of 6%, China reported that its retail spending improved 4.8% in June, following May's 6.4% increase. Industrial output remained firm as well.

This isn't to suggest that China wouldn't love to have better trade relations with the U.S. It's simply to point out that the country -- and this company -- can still thrive despite the trade impasses.