Editor's Note: An edit was made to clarify that "Falcon Flex" allows customers a chance to reallocate between modules rather than scaling down their services.

CrowdStrike (CRWD 0.25%) experienced the worst of times just one year ago. A faulty software update by the cybersecurity giant led to the world's biggest-ever information technology outage, canceling everything from flights to surgeries. At the time, insurers estimated it would cost U.S. Fortune 500 companies more than $5 billion, and over the past year, it's weighed on CrowdStrike's earnings too. The company rolled out "customer commitment packages" as a way to compensate for the upset.

In spite of this challenge, though, CrowdStrike still has managed to grow -- with revenue climbing in the double digits -- and it's maintained strong relationships with customers. This has helped the stock advance more than 50% from the outage on July 19 of last year. Is CrowdStrike today, a year after the big IT outage, a buy? Let's find out.

Image source: Getty Images.

CrowdStrike's AI-driven platform

First, a few details about CrowdStrike's business. The company offers an artificial intelligence (AI)-driven cybersecurity system that's developed and optimized to run on the cloud. This platform is called Falcon, and it gathers data from across a particular business to train on, and then uses this to help prevent cyberattacks and other security problems for that customer. Falcon is made up of many "modules" -- from threat hunting and intelligence to automated malware analysis -- that customers can select, so they can use CrowdStrike to design a solution that truly meets their needs.

To add to the flexibility, CrowdStrike's "Falcon Flex" allows customers to pick and choose modules from its entire portfolio, and reallocate spending across modules as needed.

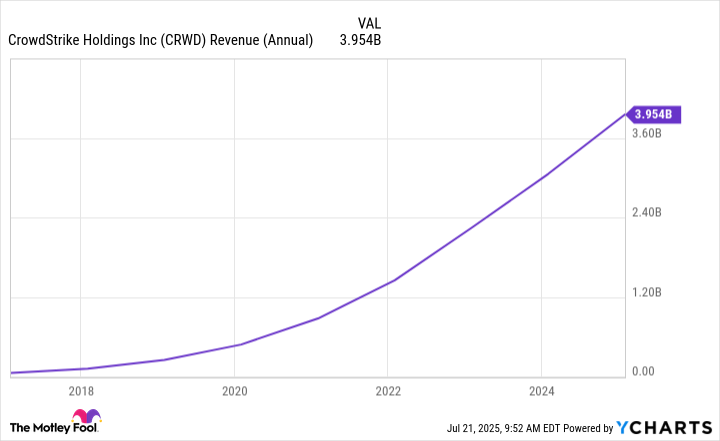

The extent of last year's outage -- halting business worldwide -- illustrates the popularity of CrowdStrike's services. And this also can be seen in the company's revenue growth over the past few years.

CRWD Revenue (Annual) data by YCharts.

Now, let's consider CrowdStrike's path since the outage. It's important to remember two things: First, this event was linked to a software update problem -- and not a cybersecurity issue -- so it doesn't call into question CrowdStrike's expertise in the area. And second, CrowdStrike acted quickly, issuing a fix for the situation within an hour. Of course, some systems took weeks to recover, but the company showed its ability to handle a crisis in an efficient manner -- a point that could encourage customers to stay on board.

In the first earnings report following the crisis, CrowdStrike said most customers stuck with the company, and CrowdStrike continued to sign new deals too. What has weighed on earnings in the quarters since is the customer commitment packages, offering benefits such as discounts, the addition of modules, and flexible payment terms. The company concluded this program as of the fourth quarter, ended Jan. 31, but expects it to impact revenue through the end of this fiscal year.

NASDAQ: CRWD

Key Data Points

Double-digit growth in recurring revenue

Meanwhile, CrowdStrike has continued to grow, with annual recurring revenue climbing 22% in the latest quarter to more than $4.4 billion. About $194 million of that was newly added in the quarter. And the company reached record cash flow from operations of $384 million. To round off that positive news, CrowdStrike announced a share-repurchase authorization allowing it to buy back $1 billion in shares; a company's interest in buying back its own shares illustrates confidence in its future.

Now, let's return to our question: Considering this whole picture, is CrowdStrike a buy a year after the big IT outage? It's true that CrowdStrike shares have climbed significantly in recent months, even reaching an all-time high. As mentioned, CrowdStrike expects the rest of this fiscal year to include some headwinds from the outage. But, in investing, it's important to look at a company's long-term prospects. From this angle, the situation looks bright. CrowdStrike has proven its strength through the worst of times and has continued to grow. The recurring revenue trends we're seeing now bode well for the future.

All of this makes the stock a buy today, a year after the crisis, and one to hold onto as a new phase of growth gets started.