Warren Buffett has a lot of money burning a hole in his pocket. Technically, it's Berkshire Hathaway's (BRK.A +0.07%) (BRK.B +0.11%) pocket, but Buffett gets to decide how to use the cash. And when I say a lot of money, I mean a lot of money: Berkshire's cash position totaled nearly $348 billion at the end of the first quarter.

The problem is that Buffett can't find many stocks to buy that meet his stringent investment criteria. However, I think there's one beaten-down blue chip stock that fits his playbook perfectly.

Image source: The Motley Fool.

A business Buffett understands

Buffett has stated on multiple occasions, in various ways, that he will only invest in a business that he thoroughly understands. In his 1996 letter to Berkshire Hathaway shareholders, he wrote: "You don't have to be an expert on every company, or even many. You only have to be able to evaluate companies

within your circle of competence."

Probably no business is within Buffett's circle of competence more than insurance. Berkshire generates a significant portion of its revenue from its property and casualty business. But the core principles of running an insurance business are the same regardless of what type of insurance it is. The key to success is to effectively evaluate risk and charge premiums that cover that risk while making a profit.

UnitedHealth Group (UNH 0.11%) is the largest health insurer in the United States. I don't doubt that Buffett knows its business quite well. After all, he bought a stake in UnitedHealth for Berkshire's portfolio in 2006 and owned the stock for three years.

Financials Buffett would find appealing

UnitedHealth Group's share price has plunged more than 50% this year. The company delivered lower-than-expected results in the first quarter. It initially cut full-year guidance and then withdrew the guidance altogether. However, I suspect that Buffett would still find UnitedHealth's financials appealing.

NYSE: UNH

Key Data Points

Buffett has talked about the importance of return on equity (ROE) in the past. He has hinted that 20% is his preferred ROE threshold. UnitedHealth Group's ROE over the past 12 months was 22.7%.

Despite its disappointing Q1 results, UnitedHealth Group's revenue still grew $9.8 billion year over year to $109.6 billion. The company also generated a profit of nearly $6.3 billion. It had nearly $34.3 billion in cash and cash equivalents with a manageable debt load. I think Buffett would focus on UnitedHealth's hard numbers more than he would Wall Street's expectations.

A price Buffett almost certainly likes

Why hasn't Buffett put more of Berkshire's massive cash stockpile to work? He can't find many stocks with attractive valuations. But UnitedHealth Group has a price Buffett almost certainly likes.

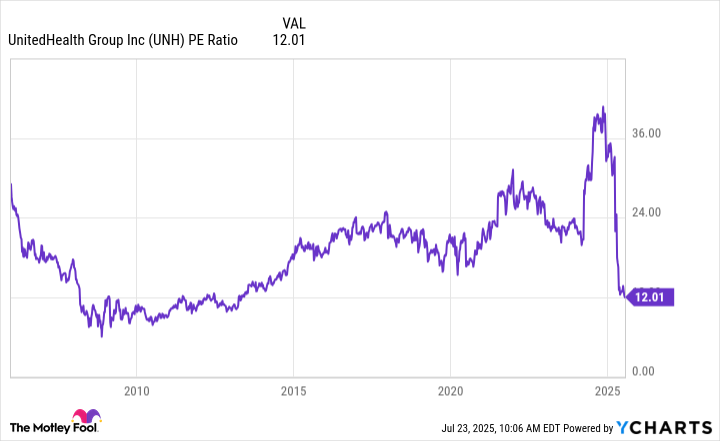

The healthcare stock trades at roughly 12 times trailing 12-month earnings. UnitedHealth Group's earnings multiple was significantly higher when Buffett first initiated a position in early 2006.

UNH PE Ratio data by YCharts

Of course, Buffett focuses on future earnings potential. Could he be worried that UnitedHealth Group's profits will continue to all? I don't think so.

The company's primary issue is that costs for some of its Medicare Advantage plans were higher than expected. Buffett knows that insurers can easily address these kinds of problems in the next year by increasing premiums. He would likely believe UnitedHealth Group's prediction that the company will return to growth in 2026.

Is Buffett buying UnitedHealth Group stock?

I also don't know if Buffett is buying UnitedHealth Group stock. He could be content to sit on Berkshire's cash and leave it to Greg Abel to make any big moves after Buffett steps down as CEO at the beginning of next year.

What I do know, though, is that UnitedHealth Group fits Buffett's playbook. And that playbook has been enormously successful through the years. Investors wanting to emulate Buffett might want to consider buying shares of the beaten-down blue chip stock while it's a bargain -- whether or not the "Oracle of Omaha" buys it himself.