In January, I highlighted Robinhood Markets (HOOD 7.79%) as a stock to buy for long-term investors, despite doubts about whether the company could do more than disrupt the brokerage industry. Back then, it was trading around $40 per share, and many still questioned its staying power.

Fast-forward six months -- not yet the long term -- and the stock has surged past $100, lifting its market capitalization to nearly $90 billion, resulting in a remarkable 173% increase year to date. With shares now near all-time highs, let's dive into what's driving this momentum, what lies ahead, what could go wrong, and whether the stock still makes sense for investors.

Here's how Robinhood is growing so quickly

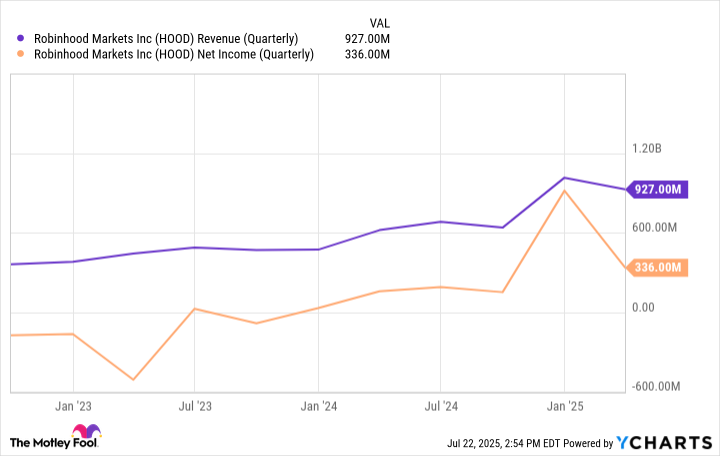

Robinhood delivered standout Q1 2025 results, with revenue soaring 50% year over year to $927 million. The biggest driver was a 77% surge in transaction-based revenue, which climbed to $583 million.

Robinhood's second-largest revenue stream, net interest income, rose 14% to $290 million, fueled by a larger base of interest-earning assets and a continued ramp-up in securities lending.

Moreover, the brokerage gained $2 billion in net deposits in the quarter to a record $18 billion, and Robinhood Gold, the company's subscription offering that costs $5 per month or $50 annually, saw subscribers nearly double year over year from 1.7 million to 3.2 million.

Robinhood CEO Vlad Tenev summed up the growth on the Q1 earnings call: "Customers are not only trading more with us, but they're entrusting us with more of their assets."

As for how its growth is translating to the bottom line, Robinhood produced $336 million in net income, an impressive increase of 114% year over year.

HOOD Revenue (Quarterly) data by YCharts

Can Robinhood continue to grow?

As for where Robinhood goes from here, the company acquired TradePMR, a trading platform designed for independent registered investment advisors, for $300 million in cash and stock. The deal, which allows Robinhood entry into the wealth management sector, is another step in diversifying its business.

Additionally, Robinhood recently closed on its $200 million acquisition of Bitstamp, the world's longest-running cryptocurrency exchange, to broaden its addressable market outside of the U.S.

"Our 10-year arc, our long-term arc, is to build the No. 1 global financial ecosystem," Tenev added on Robinhood's most recent earnings call. "That means expanding our business from retail only, which it pretty much is now, to also serving businesses and institutions, and also expanding from primarily U.S. to being a full global platform serving customers everywhere."

Notably, Robinhood has nine different businesses that each generate at least $100 million in annualized revenue, nearly twice as many as a couple of years ago. Tenev also mentioned other opportunities for growth, including building out 24-hour trading, 401(k) administration for businesses, and employee stock plan administration for public companies.

Image source: Getty Images.

Here's what could go wrong for Robinhood

As of now, considering Robinhood's high growth, profitability, and clean balance sheet with $2.2 billion in net cash, you'd be hard pressed to find any problems with its business. However, the stock can be a different story.

For high-growth companies like Robinhood, their stocks typically have two issues: share dilution and valuation.

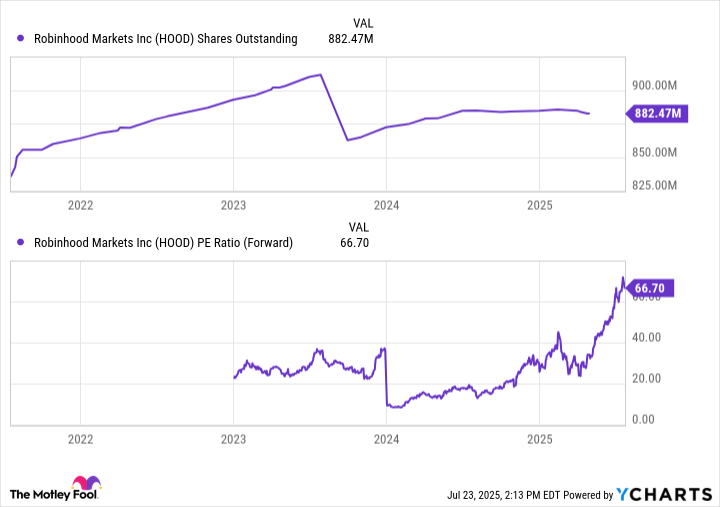

Since its IPO, Robinhood's share count has risen by 5.6%, which dilutes investors' ownership stake. The good news is that management is addressing the concern, lowering share-based compensation from $871 million in 2023 to $304 million in 2024. Additionally, management recently increased its share repurchase authorization from $1 billion to $1.5 billion, or nearly all of its $1.6 billion in trailing 12 months of net income. According to management, the buybacks will decrease its share count by approximately 1% in 2025.

As for the stock's valuation, Robinhood now trades at roughly 67 times forward earnings estimates, near an all-time high.

That's a steep price tag for a company still pouring resources into growth and customer acquisition. While Robinhood's roadmap includes promising new products that could eventually justify the valuation, many remain early stage ideas with no guarantee they will turn into meaningful profits.

HOOD Shares Outstanding data by YCharts

Is Robinhood stock a buy?

Robinhood continues to prove its doubters wrong. With 75% of its 25 million funded accounts coming from members of the millennial and Gen Z generations, the platform is well-positioned for long-term growth as those users get older and build wealth.

Still, with shares near all-time highs and valuation stretched, now may not be the best entry point. Long-term investors who believe in the vision might consider holding or dollar-cost averaging, i.e., investing a set amount at predetermined times. But chasing the stock after its massive run comes with real risk for future returns.