Palantir Technologies (PLTR 1.66%) has an important event coming up on Aug. 4: its quarterly earnings. These updates are a huge deal, as they are one of four times a year when investors receive detailed updates directly from the company on its financial performance. It could be argued that this is the only information that should move stocks, besides a handful of other breaking news announcements surrounding a business.

Palantir has incredibly high expectations heading into the report. But will its results be enough to satisfy investors?

Image source: Getty Images.

Palantir is seeing strength in multiple areas

Palantir's software integrates data analytics with AI. This isn't a new concept; Palantir has been doing this for over two decades. Originally, its software was intended for government use and provided its users with actionable insights after processing all data inputs. It's widely reported that Palantir even helped track down the final hiding location of Osama bin Laden.

After developing significant relationships with various government clients, Palantir expanded to the commercial side, which has been a successful endeavor. Still, government revenue makes up the majority of Palantir's total, coming in at $487 million compared to $397 million in commercial revenue during Q1. However, don't assume that just because the government is a large part of Palantir's business its revenue is growing slower.

NASDAQ: PLTR

Key Data Points

In Q1, government revenue rose 45% while commercial revenue rose 33%. This mismatch has one primary factor: poor international AI adoption. Commercial AI adoption hasn't been as rapid in other areas (particularly Europe) as it has in the U.S. This is evidenced by U.S. commercial revenue increasing 71% to $255 million during Q1.

In Palantir's Q2 earnings report on Aug. 4, investors should watch this trend to see if commercial AI adoption is starting to take off in areas outside the U.S. If it does, it could cause Palantir's stock to react positively.

But there is one prohibiting factor that could dampen any effects of a strong quarter.

Palantir's valuation is hard to justify

Palantir's stock has risen dramatically over the past year and a half. The stock is up over 800% since the start of 2024; however, Q1's revenue growth was only 39%. This represents a serious mismatch between business and stock growth, so what's going on here?

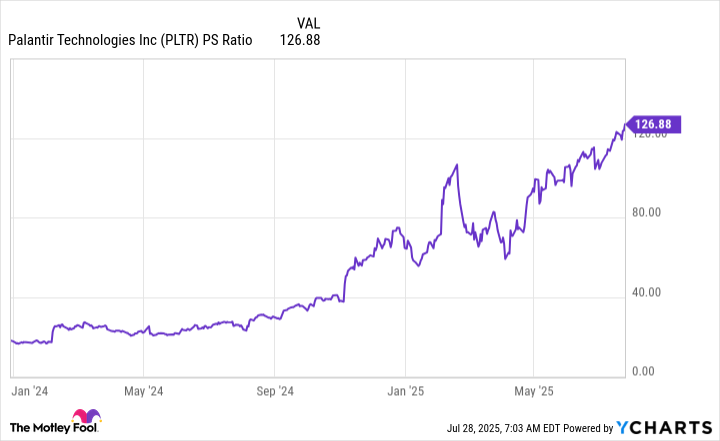

Palantir's stock and business have nearly uncoupled, as the stock valuation has risen to more than 125 times sales.

PLTR PS Ratio data by YCharts

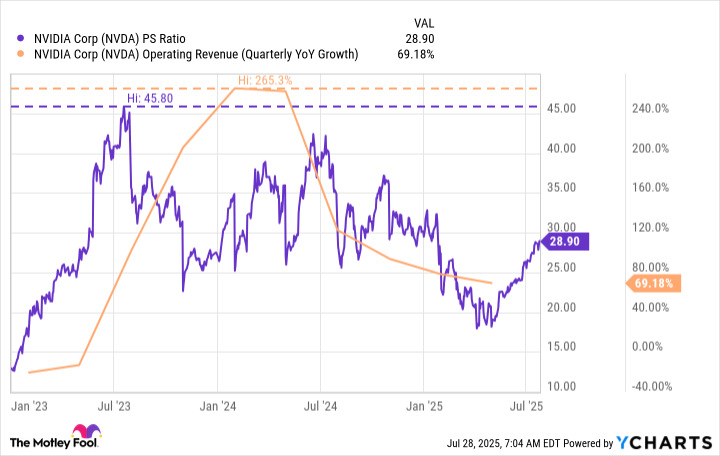

Most stocks that achieve this valuation are doubling or tripling their revenue year over year, but Palantir is nowhere close to that. If we compare it to one of the fastest-growing companies over the past few years, Nvidia, it's clear that Palantir is not only growing much slower but also at a much higher valuation than Nvidia ever achieved.

NVDA PS Ratio data by YCharts

Despite Nvidia's revenue growing at a jaw-dropping 265% pace, it never traded for more than 46 times sales.

Palantir expects a 38% revenue growth rate for Q2, and trades for more than 125 times sales. There's an obvious mismatch between what the business is doing and what the stock indicates that it could do.

This creates a precarious situation for Palantir's stock, and it could fall dramatically after earnings if the market doesn't get what it wants.

For Palantir to maintain its ultra-premium price tag, it will need to exceed internal growth expectations by several percentage points. If it doesn't, don't be surprised if the stock gets whacked. Even if it exceeds guidance, it could see a sell-off due to its premium valuation.

There is no compelling argument for why Palantir's stock should be valued this high, and it's in a precarious position. While the stock may continue to rise following earnings, it will likely be due to hype, as the current expectations baked into the stock price aren't even in the same ballpark as where Palantir is as a company.