Some discount retailers are seeing improving traffic and sales this year, as consumers are on the hunt for better value. Not all discount stores are experiencing this, but if this is the beginning of a broader shift in consumer behavior, it could be a great buying opportunity for investors looking for potentially undervalued stocks in the retail sector.

Here are two stocks that could be timely buys right now.

Image source: Getty Images.

1. Target

Shares of Target (TGT +1.50%) have fallen about 61% from the previous peak in 2021. Several issues have contributed to the decline, including inventory loss from theft and weak same-store sales (comps).

However, this is still one of the largest and most profitable discount retailers. Despite these problems, Target still generated more than $4 billion in net profit on $105 billion of revenue over the last year.

The company just raised its quarterly dividend by 1.8%, marking 54 consecutive years of dividend increases. It also has plenty of headroom to maintain dividend increases, paying out less than half its trailing-12-month earnings.

NYSE: TGT

Key Data Points

There are signs that Target's business will improve. It recently announced leadership changes to accelerate its growth strategy. The company's digital business is performing well, with consumers engaging more with same-day delivery services, which grew 35% last quarter.

Total net sales were still down in the first quarter, but digital comps were up 4.7%, which should encourage the company to continue investing in this sales channel to drive more growth.

Management also noted progress in mitigating the inventory problems that weighed on its profitability the past few years. Including the expected impact from tariffs, it expects full-year adjusted earnings per share (EPS) to be between $7 to $9 -- more than enough to cover the dividend.

Target stock may remain volatile in the near term, but with the forward dividend yield sitting at 4.38%, and the forward price-to-earnings ratio down to 14 (toward the lower end of its three-year range), it could be close to bottoming out.

2. TJX Companies

When consumers start looking for value, TJX Companies' (TJX 0.18%) off-price merchandise strategy is usually there to benefit. TJX has some of the top-performing discount apparel stores like T.J. Maxx, Marshalls, and outdoor clothing specialist Sierra (along with HomeGoods and other brands). A $10,000 investment in the stock in 2005 would be worth $279,000 today, including dividends, and there are several reasons to expect the stock to keep growing in value.

NYSE: TJX

Key Data Points

The company is in business to find deals on quality merchandise and to stock its stores with these gems at big discounts. It excels at this business model, with a global sourcing channel and sophisticated supply systems. With consumer confidence shaken in the first half of 2025 over uncertainty about the economy, every one of its segments -- including TJX Canada and TJX International -- posted a sales increase.

TJX has successfully navigated several challenging economic environments over the last few decades. The best thing about this business is that it is positioned to grow sales whether the economy is booming or in a recession, thanks to its global buying infrastructure and the attractive deals it can offer.

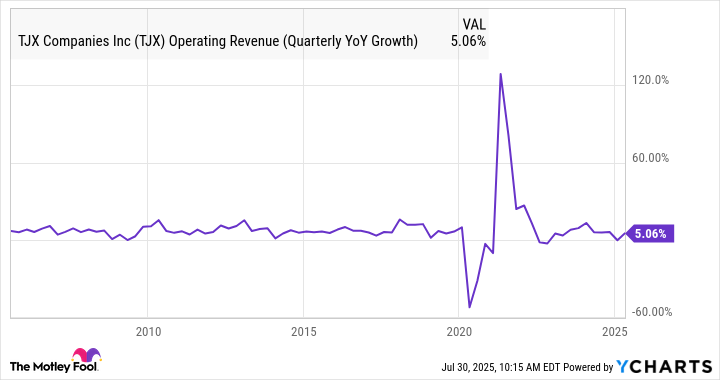

Management has maintained quarterly sales growth consistently over the last 25 years, with the only significant decline experienced during the pandemic in 2020.

TJX Operating Revenue (Quarterly YoY Growth) data by YCharts; YoY = year over year.

Another business practice that supports the retailer's growth prospects is its talent development program. TJX is known to promote managers from within its own ranks, which helps build a deep bench of talent that lends itself to consistent performance over the long term.

The stock is not cheap, but it should deliver great returns. Management is seeing strong merchandise acquisition opportunities, as well as opportunities for market share growth worldwide in the off-price market.