Shares of financial technology (fintech) company PayPal (PYPL 1.68%) dropped 9% on July 29 after it reported second-quarter financial results. I believe it was a clear overreaction.

Investors seemed to head for the exits after looking at PayPal's second-quarter free cash flow. In Q2, the company generated free cash flow of $692 million, which was down a whopping 49% year over year. That certainly looks troubling.

Image source: PayPal.

In reality, PayPal had been expecting $6 billion to $7 billion in free cash flow in 2025. After reporting Q2 results, its expectations are unchanged. The 49% Q2 drop is simply a cash-flow timing issue, not a sign of something problematic. Consequently, I believe the 9% drop for PayPal stock was overdone.

But is the drop in PayPal stock's price a buying opportunity? That's a question worth exploring.

What's going right for PayPal

PayPal is a low-growth business at this point with just 5% Q2 revenue growth. Active accounts were only up by 2%. But the company is turning some heads when it comes to profitability.

NASDAQ: PYPL

Key Data Points

When PayPal hired Chief Executive Officer Alex Chriss in 2023, he immediately took notice of the company's transaction margin. To win large accounts, the company had lowered its prices, particularly when it was working behind the scenes with unbranded checkouts.

PayPal has renegotiated some of its top contracts since Chriss' arrival, and it's lifted how much profit it makes per transaction. In Q2, the company's transaction margin dollars increased by 7%, which was notably ahead of its 5% revenue growth.

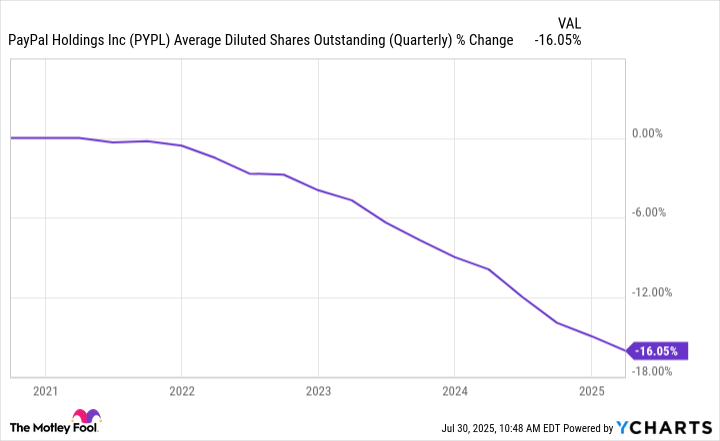

When it comes to the bottom line, it gets even better for PayPal. Management has aggressively bought back stock with its profits, lowering the share count and consequently boosting its earnings per share (EPS). Q2 EPS was up 20% year over year, which is something that shareholders love to see.

Since early 2022, the share count for PayPal has steadily dropped, as the chart below shows.

PYPL Average Diluted Shares Outstanding (Quarterly) data by YCharts

There are some caution flags out

PayPal stock dropped 9% after earnings, as mentioned. It's also down 23% from 52-week highs, as of this writing. So, investors want to know if this pullback is a buying opportunity. After considering what's going right, some may be inclined to believe that it is indeed an opportunity.

There is more to consider, however. First and foremost, PayPal's user growth has stalled. Active accounts were only up 2% in Q2. But more troubling was the 4% drop in transactions per active account on a trailing-12-month basis. The downward trend started in the first quarter, when transactions per account had dropped by 1% (after years of increases), but it looks like it's picking up steam now.

With account growth stalling and transactions dropping, PayPal doesn't offer much to investors when it comes to revenue growth. That's why these are caution flags -- stocks that outperform the S&P 500 usually have above-average top-line growth.

What's the verdict?

While PayPal's recent growth leaves a lot to be desired, better growth could be around the corner.

For starters, PayPal owns Venmo, and it accounts for 18% of the company's total payment volume -- a meaningful amount. Venmo's growth has accelerated in recent quarters. In the second quarter of 2024, Venmo's volume was only up 8% but it was up by 12% in Q2. This acceleration is promising.

Moreover, PayPal just announced PayPal World, a partnership that will allow for interoperability with major digital wallets worldwide. Early joiners include Latin America's MercadoLibre and China's Tencent. This partnership could boost PayPal's adoption, but investors won't know for sure until after it officially launches this fall.

For me, the verdict is that PayPal stock is a buy, with a caveat. The caveat is that I don't believe the company's current growth can lift the stock above the S&P 500 over the next five years. Shareholders need some of its growth initiatives to pay off.

However, PayPal stock is low-risk. Its scale is vast, it's generating substantial free cash flow, and it's boosting shareholder value with stock buybacks. Even if growth continues to sputter, the company's EPS should increase modestly, lifting the shares.

Because PayPal stock is down significantly from its 52-week high, there's a margin of safety with this investment. In conclusion, if things go as they are now, there may be little downside for investors. And if things get better due to things such as Venmo's growth, then it could be a market-beating investment.