Lucid Group (LCID +1.38%) stock saw a big pop last month after the company announced that it had entered into a robotaxi partnership with Uber Technologies. Uber will purchase 20,000 or more of the automaker's vehicles over the next six years and use them as key components of its robotaxi fleet. Lucid's share price has since had a substantial pullback.

There will soon be another big potential catalyst that could spur substantial moves for the stock. The electric-vehicle (EV) specialist is set to release its second-quarter report and host an earnings conference call after the market closes on Aug. 5, and investors will be taking a close look at its margins and bottom line.

NASDAQ: LCID

Key Data Points

If you're wondering what history says about your chances of success with buying Lucid's stock ahead of earnings, take a look at the chart below and read on for a deeper look at dynamics that could shape the company's valuation.

Image source: The Motley Fool

Lucid's stock has historically struggled after earnings

As the chart above shows, it's historically been a bad move to buy Lucid's shares ahead of the company's earnings reports. Most of its quarterly releases have corresponded with big sell-offs for the stock, and the EV specialist's share price is now down roughly 87% over the last three years. Sales and earnings performances have generally come in below the levels needed to spur gains for the stock:

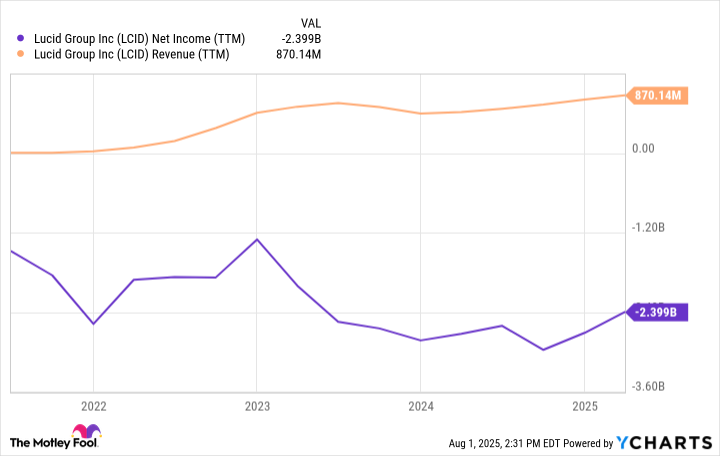

LCID Net Income (TTM) data by YCharts.

Lucid has posted large losses across its history as a publicly traded company. At the same time, the business's sales growth has been very uneven after an initial ramp-up period.

Heading into the upcoming earnings report, the business has recorded a net loss of roughly $2.4 billion on sales of roughly $870 million across the trailing-12-month (TTM) period. In other words, Lucid has lost roughly $2.76 for every $1 in revenue that it's generated over that stretch. There are good reasons to think that losses will continue to come in at high levels for the foreseeable future.

Will Lucid stock see another sell-off after the Q2 report?

Because Lucid announces its vehicle production and delivery numbers after each quarter, investors already have some key insights into what to expect with the second-quarter report. In the update it published at the beginning of July, the company announced that it had produced 3,863 vehicles and delivered 3,309 vehicles in Q2. For comparison, it produced 2,110 vehicles and delivered 2,394 vehicles in last year's second quarter.

The rollout of the Gravity SUV has helped spur a significant uptick in production and deliveries, but the stock could see a big pullback if the upcoming Q2 report arrives with a wider-than-expected loss. Lucid's path to profitability hinges on achieving economies of scale that allow it to shift into posting positive gross margins on each vehicle sold, and then continuing on that track until it can deliver positive operating income margins. As things stand, it currently costs the company far more to produce each one of its vehicles than is recouped through a sale.

Historically, Lucid Group's earnings reports have arrived with wide losses that have driven sell-offs for the stock. Given that shares already trade at a severely beaten-down price compared to where they were a few years ago, there's no guarantee that this dynamic will play out again after the next earnings report -- but investors will likely be looking to see that Lucid has a feasible path to eventually delivering big margin improvements.