Lululemon (LULU 4.21%) was once a market darling. It is now one of the worst-performing stocks of 2025. Shares are off close to 50% so far in 2025 on rising fears of competition and macroeconomic headwinds in its athleisure category, with shares down over 60% from all-time highs. After a bustling few years with casual athletic clothing on the rise during the early days of the pandemic, consumers are now flipping to new categories.

And yet, there are still a lot of things to like about Lululemon's business. With the stock trading at one of its cheapest levels ever, is Lululemon stock about to go parabolic for investors who buy today?

NASDAQ: LULU

Key Data Points

Slow North America growth

From the third quarter of 2020 to the fourth quarter of 2023, Lululemon's trailing-12-month revenue in North America more than doubled from $3.5 billion to $7.6 billion. Since then, its trailing-12-month revenue has barely budged, hitting $8 billion over the last 12 months. Investors are not liking this revenue growth slowdown in the core North American market. Last quarter, Americas revenue increased just 4% year-over-year in constant currency.

While a slowdown should never be celebrated, it is important to take everything within a proper context. The entire athleisure category that Lululemon serves has struggled in recent years, especially in the Americas. Competitor Nike saw revenue drop 11% year over year last quarter, while Athleta slipped 6% (geographical revenue was not disclosed, but the brand is mainly centered in North America). This puts Lululemon's slow 4% revenue growth in a better light.

Despite macroeconomic headwinds for the athleisure category, Lululemon has been able to grow market share and still expand in North America.

Image source: Getty Images.

Room for international expansion

North America is the ugliest part of Lululemon's business, but international is firing on all cylinders. Total international revenue grew 20% year-over-year in constant currency terms last quarter, with China mainland revenue up 22% even with Chinese consumers facing a spending recession for the last few years after the country's housing bubble burst.

Lululemon is just beginning to tap the East Asian market, which is the largest spending region in the world on luxury and premium apparel. Now, it is beginning to expand in Europe. For example, it just opened a flagship 5,700-square-foot store in Milan's shopping district to showcase its products to European shoppers. Other regions outside of China and North America make up just a sliver of Lululemon's revenue, giving it a huge runway to expand in Europe.

Even if growth in North America is sluggish for a few years, other geographies can help Lululemon keep chugging along for investors.

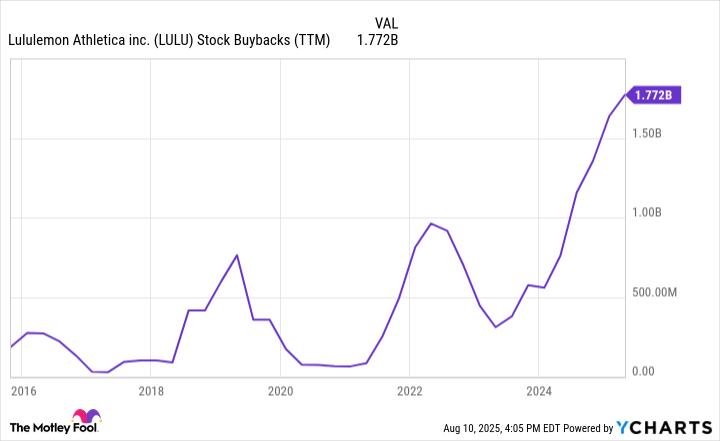

LULU Stock Buybacks (TTM) data by YCharts

Is Lululemon stock about to go parabolic?

After this recent drawdown, Lululemon has a market cap of $22.7 billion. This gives the stock a trailing price-to-earnings ratio (P/E) of under 13, its lowest level in 10 years. If revenue can keep growing and profit margins remain strong (the metric has steadily expanded in the last 10 years), then Lululemon stock looks exceedingly cheap at these levels.

The cherry on top is management's increased spending on stock buybacks, which hit $1.77 billion over the last 12 months. At this rate, Lululemon is close to repurchasing 10% of its outstanding stock per year, which would be a huge boost to earnings per share (EPS) growth.

Apparel is a fickle industry, but Lululemon has shown resilience through thick and thin and now trades at a relatively cheap earnings ratio. Combined with its aggressive buyback program, I think the stock has a chance to zoom parabolic for investors.