At one point in time, Lululemon (LULU 1.35%) was a darling of the stock market, loved by investors, with shares trading up over 3,000% from its initial public offering (IPO) around 20 years ago. No longer. The stock has collapsed and it now trades at one of its lowest valuations ever, driven by a narrative around increased competition in athleisure apparel and declining category sales in North America. Lululemon stock now trades down 64% from all-time highs, its worst drawdown since the Great Recession in 2008-09.

Let's dissect the problems with Lululemon's business today and see if this discounted price makes the stock a buy.

Image source: Getty Images.

A slowing athleisure category

The core reason for Lululemon's stock drop is slowing overall revenue growth. Since the pandemic boom for athleisure and casual clothing, Lululemon's revenue growth has steadily declined and hit a level of 7.32% last quarter, which is a five-year low.

Slowing revenue growth is never good in a vacuum. However, with Lululemon, investors may be overreacting by sending the stock down over 60% just because revenue growth slowed to 7%. Athleisure spending as a whole has gone through a cycle in North America, booming during the pandemic and now coming back down to earth. Many Lululemon competitors such as Nike are seeing declining sales in North America, while Lululemon is still growing 4% year over year in constant currency in North America.

What's more, Lululemon has been able to retain its high profit margins even with a revenue growth slowdown. Operating margin was above 23% over the last 12 months, which is close to a five-year high. This shows that Lululemon has been able to retain its premium price point with consumers despite tons of knockoff competitors hitting the market. Faster growth than the competition and strong profit margins are two good signs for the health of Lululemon's business in North America.

NASDAQ: LULU

Key Data Points

Management's approach to capital allocation

With increasing scale and fat profit margins, Lululemon generates a ton of cash flow. The first thing management does with this cash flow is reinvest into international expansion, which is a huge growth market for Lululemon. China mainland revenue is growing at 22% year over year and can be a huge market for the brand. The company is beginning to make a major push into Europe, launching its first flagship store in Milan's famous shopping district. Athleisure growth has been slower in Europe compared to other regions but still has a ton of potential for the Lululemon brand.

After international expansion, Lululemon takes its cash flow and returns it to shareholders through share buybacks. Over the last 12 months, management has repurchased $1.77 billion in stock, which equates to 8% of the current $22 billion market cap repurchased on an annual basis. The company has accelerated stock buybacks in recent quarters with the stock falling, which is a good thing for investors. As shares outstanding come down, the company will grow its earnings per share (EPS) at an even faster pace.

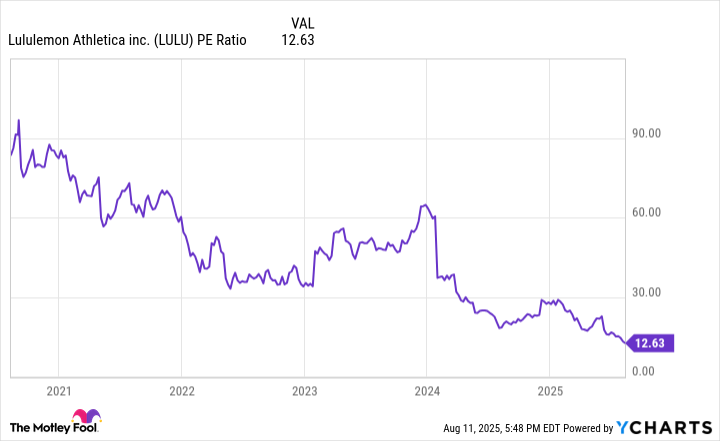

Data by YCharts.

Lululemon's valuation is appetizing

As of this writing on Aug. 11, 2025, Lululemon stock trades at a price-to-earnings ratio (P/E) ratio of just 12.6, a five-year low and well below its previous P/E ratio of 90 back in 2021. This discount means that the business doesn't have to perform extraordinarily in order for the stock to do well for investors.

Even if Lululemon's revenue only grows in the single digits going forward, the stock will likely go up. Stable margins and a heavy buyback program can help EPS grow at a double-digit rate over the long term, even if the stock price keeps falling in the interim. Stock prices follow growth in EPS on a long enough time horizon.

If you are confident that Lululemon can keep taking share in athleisure by growing steadily in North America and expanding internationally, then the stock's current valuation looks highly appealing. Consider buying shares of Lululemon and holding on tight for the long haul.