CEO and chief investment officer of Ark Invest Cathie Wood earned a reputation for making high-conviction bets on disruptive, speculative opportunities aimed at toppling legacy incumbents in markets such as financial services, technology, and pharmaceuticals. When it comes to artificial intelligence (AI) stocks, it's no surprise that Wood has taken a liking to data analytics powerhouse Palantir Technologies, the third-largest holding across Ark's exchange-traded funds (ETFs).

Every now and then, however, Wood quietly complements Ark's high-growth positions with a select group of blue-chip counterparts. In Palantir's case, the company is often linked with an emerging corner of the AI realm, using its analytics platforms to bolster the capabilities of the U.S. Department of Defense (DOD).

While Palantir will likely remain a core Ark position, recent buying activity hints that Wood may be broadening her exposure within the national security arena, scouting for under-the-radar opportunities even as Palantir remains her flagship pick at the intersection of AI and military operations.

Throughout the summer, Wood has been accumulating shares of L3Harris Technologies (LHX +1.82%) in both the ARK Space Exploration & Innovation and ARK Autonomous Technology & Robotics funds.

Let's explore what may have prompted this move and assess if defense tech investors should consider looking beyond familiar names like Palantir.

NYSE: LHX

Key Data Points

Understanding how AI fits into the defense equation

While AI has become the dominant megatrend driving the technology sector, most conversations still center on chips, data centers, cloud infrastructure, or workplace productivity tools. Behind the scenes, however, AI is rapidly emerging as a transformative tailwind reshaping modern military strategy.

AI's applications in national security range from satellite imagery analysis and equipment maintenance to cybersecurity threat detection and autonomous navigation for unmanned systems like drones.

Among established defense contractors, the usual names include Northrop Grumman, General Dynamics, Lockheed Martin, Boeing, RTX, Kratos Defense & Security Solutions, and L3Harris.

Palantir stands apart from these incumbents thanks to its versatile AI platforms, including Foundry and Gotham. This integrated ecosystem has positioned Palantir as the operating system supporting a wide range of military operations, securing billion-dollar contracts with the Army and Navy, and extending its reach overseas through collaborations with U.S. allies in NATO.

Image source: Getty Images.

Why might Cathie Wood like L3Harris stock?

Like many of its peers mentioned above, L3Harris manufactures mission-critical systems poised to benefit from deeper integration of AI-enhanced capabilities. This makes it plausible that Wood is targeting stealth opportunities to complement Ark's more pure play AI holdings, such as Palantir.

That same logic helps explain why several defense-adjacent companies such as electric vertical take-off and landing aircraft (eVTOL) Archer Aviation and Joby Aviation, Kratos, AeroVironment, and Lockheed found a place in Ark's portfolio. When it comes to L3Harris however, I think there is a more specific catalyst behind Wood's recent buying.

While Palantir often commands the spotlight in the DOD's high-profile technology awards, many other contractors secure portions of these deals. L3Harris is one of them, partnering with Palantir to develop the Army's next-generation ground transportation systems under the Titan program.

During the company's second-quarter earnings call, L3Harris CEO Christopher Kubasik even highlighted the collaboration, noting, "our ongoing partnership with Palantir on the U.S. Army's Titan program continues to mature".

Is L3 Harris stock a buy?

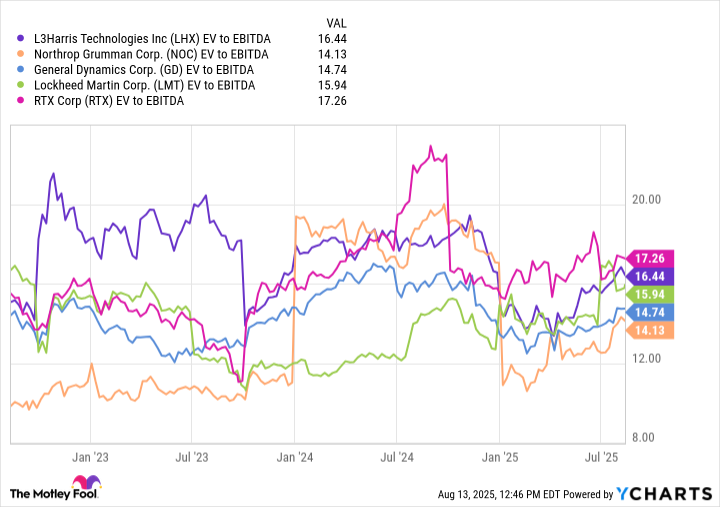

The comparable company analysis benchmarks L3Harris against a peer set of leading defense contractors on an enterprise value-to-EBITDA (EV/EBITDA) basis.

LHX EV to EBITDA data by YCharts.

From a valuation standpoint, L3Harris trades at an EV/EBITDA multiple of 16.4 -- a discount to historical peaks but still on the higher end of this cohort. Despite this relative premium, analysts largely view L3Harris through the lens of a conventional defense contractor, valuing the company based on its current contracts and pipeline.

I think that the upside from AI integration is not yet fully reflected in L3Harris's share price. As AI-enabled services become a greater priority at the Pentagon, the narrative around traditional contractors could shift especially as they form deeper ties with leading technology platforms like Palantir -- as L3Harris is already doing.

For this reason, I see L3Harris as well positioned for long-term valuation expansion and consider it a savvy buy at current levels.