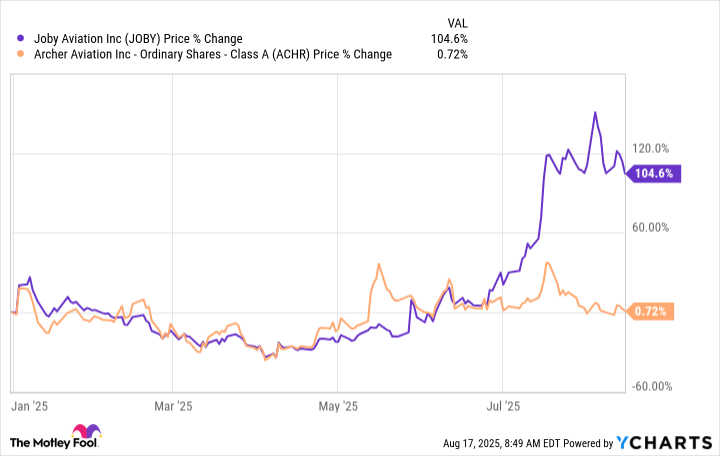

Archer Aviation (ACHR +8.11%) shareholders are experiencing turbulence while watching rival Joby Aviation (JOBY +9.05%) fly high. Archer's stock has dropped 13% over the past 30 days, while Joby's shares have climbed by nearly 2% in the same period. More telling, Joby's shares have more than doubled this year while Archer's stock has essentially traded sideways in 2025:

But here's what the market might be missing: Archer just reported a fortress balance sheet with $1.72 billion in cash, significantly more than Joby's $991 million -- or $1.24 billion including Toyota's pending $250 million investment -- and the company is targeting its first commercial revenue in late 2025. For contrarian investors, this divergence could spell opportunity.

Image source: Getty Images.

The cash burn reality check

Archer's Q2 numbers weren't pretty on the surface. The net loss ballooned to $206 million from $107 million a year ago, while the adjusted loss on earnings before interest, taxes, depreciation, and amortization (EBITDA) hit $119 million. The company missed earnings expectations badly, posting a loss of $0.36 per share versus the Street's forecast of $0.25, a 44% miss that initially sent shares tumbling.

But dig deeper, and the picture improves. Archer's typical burn rate of between $95 million and $110 million per quarter gives it roughly 15 quarters of runway at current spending levels. Even if it continues to burn cash at an elevated rate, the air-taxi pioneer ought to have at least two years of solid runway before needing another major capital injection.

Why the market is wrong about Archer

Wall Street currently crowns Joby as the leading bet in the electric vertical takeoff and landing (eVTOL) space, assigning it a market cap north of $14 billion. Archer, by comparison, trades at roughly $6.3 billion despite holding more cash on its balance sheet.

NYSE: ACHR

Key Data Points

What the market is overlooking is Archer's potential military windfall. Unlike with passenger operations, defense contracts don't hinge on certification from the Federal Aviation Administration (FAA). Thanks to recent acquisitions aimed at accelerating military aircraft development, Archer could start generating revenue years before commercial air-taxi services ever take flight.

The Pentagon is actively seeking next-generation vertical lift solutions, and allied nations are following suit. Archer is positioning itself as a direct answer, while Joby's fortunes remain tethered to regulatory timelines.

CEO Adam Goldstein has been clear: Defense is the company's largest near-term opportunity. With defense buyers known to pay premium prices for cutting-edge tech, Archer's path to profitability could be far shorter than Wall Street assumes.

The path-to-profitability problem

Both companies face a punishing road ahead. Wall Street doesn't expect Archer to generate positive cash flow until at least 2028. FAA certification could slip to 2027, which puts added weight on the company's defense contracts to deliver recurring revenue sooner rather than later.

Consumer adoption is another headwind. Early uptake of air-taxi services is expected to be sluggish, and persuading people to step into an entirely new mode of transportation may prove harder than building the aircraft itself.

Competition also looms large. Beyond Joby, rivals including Vertical Aerospace, Beta Technologies, and China's EHang are sprinting toward the same target. The reality is that the eVTOL market won't sustain a dozen winners in its formative years. Infrastructure, regulatory, and demand constraints mean only a select few will survive.

Time to take flight?

At current levels, Archer looks like the better risk-reward play than its closest peer, Joby Aviation, in the eVTOL space. The stock trades at a 42% discount to its 52-week high despite operational progress and a strong balance sheet. While Joby captures most of the market's attention, Archer has the balance sheet to weather delays -- plus potential defense and international opportunities for near-term revenue.

For risk-tolerant investors who believe urban air mobility represents the future of transportation, Archer offers a compelling entry point. The company has sufficient cash to reach commercialization and multiple potential revenue streams, and it trades at a discount to its closest peer. Just remember: This is still a pre-revenue company burning $100 million-plus quarterly in an unproven market. Size positions accordingly.