One of the hardest but most valuable lessons to learn with investing is to add to your winners. As counterintuitive as it may feel, winning stocks tend to keep winning over the long term. A perfect opportunity to put this lesson to work is with Sprouts Farmers Market (SFM +1.05%), a better-for-you grocery store chain.

The company's share price has already quadrupled in two years, but the company remains reasonably valued and could see decades of success. Here's what sets the unique grocer apart and why a recent 20% dip makes now a good time to add to this winner.

NASDAQ: SFM

Key Data Points

Sprouts Farmers Market: Reimagining the grocery business

Sprouts Farmers Market is home to 455 specialty grocery stores across 24 states. It primarily focuses on groceries with specific attributes, such as being organic, gluten-free, keto, vegan, plant-based, high-protein, Kosher, paleo, or made with no seed oil.

Focusing on this specialty grocery niche -- an industry expected to grow between 5% and 6% through 2030 -- Sprouts offers investors numerous reasons to be optimistic about its outperformance potential.

A resilient customer base

Sprouts' customers tend to be health-oriented, focusing on lifestyle-friendly products that fit a particular diet. This notion makes the company's customers more resilient as they're not likely to stray from their diets, even if macroeconomic conditions worsen.

Further supporting its customers' resiliency is the fact that the average Sprouts customer has an above-average household income of $121,000, leaving the company less susceptible to fluctuations in the economy. Despite numerous challenges facing consumers over the last three years, Sprouts has grown sales and earnings per share (EPS) by 33% and 122%, respectively.

Image source: Getty Images.

Major store-count expansion plans

Sprouts plans to grow its store count from 455 today to 1,200-1,400 over the long haul. With 75% of its stores in just five states -- California, Arizona, Colorado, Texas, and Florida -- there is ample greenfield opportunity across the U.S. to do so. Sprouts plans to open roughly 50 stores in 2025 and has an additional 130 approved locations already in its pipeline after that.

The company recently expanded into the Northeast and now has 20 stores in the region. This area will be critical for investors to watch as it represents the company's first foray into colder climates, where it's more complicated to deliver fresh, local produce consistently.

If Sprouts can succeed in the Northeast and maintain their high quality and freshness, an expansion to the northern U.S. states could be viable.

E-commerce sales expand Sprouts' reach

E-commerce sales grew by 27% year over year in the last quarter (compared to 17% overall for Sprouts), and now equals 15% of total sales. These e-commerce sales are vital because they dramatically expand the company's service area.

Generally, its brick-and-mortar store customers live within about a 10-minute drive from the store. However, by partnering with all the major food and grocery delivery behemoths, Sprouts can boost this area to anyone within 30 minutes of a store.

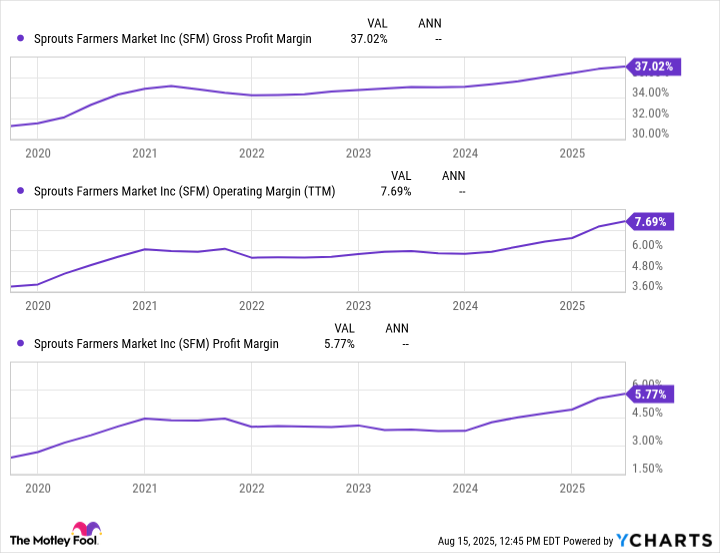

Sprouts' burgeoning profitability

Sprouts remains in expansion mode, but its profitability continues to shoot skyward. One reason for this robust profitability is that the company's new stores typically reach breakeven profitability within the first year.

Data by YCharts.

This quick turnaround means that even though Sprouts is accelerating its expansion plans, it doesn't have to sacrifice margins to grow.

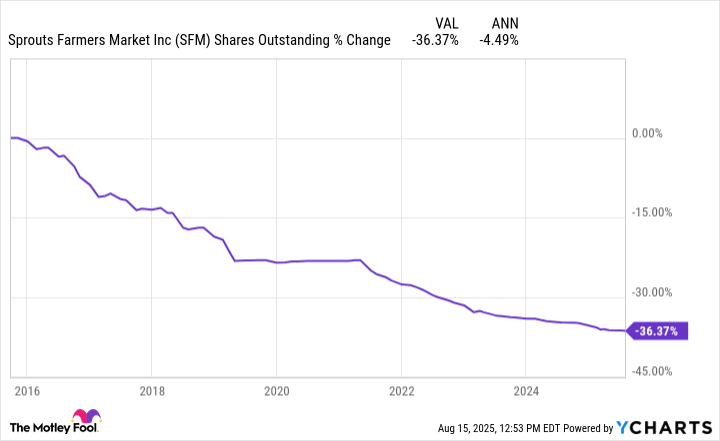

Powerful stock buybacks

Armed with this 6% net profit margin -- and a matching 6% free cash flow (FCF) margin (even though it spends heavily on new stores) -- Sprouts has ample cash to give back to shareholders. Using stock buybacks as a way to reward shareholders, Sprouts has lowered its shares outstanding by 4.5% annually over the last decade.

Data by YCharts.

With more than one-third of its shares now reabsorbed into the company, Sprouts essentially juiced its "per-share" figures, like EPS, by more than 50% from these buybacks alone.

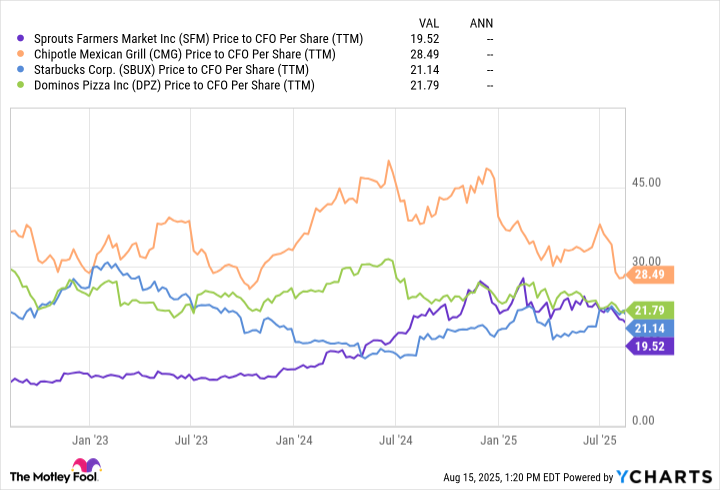

Is it too late to buy Sprouts Farmers Market?

There's no denying that Sprouts Farmers Market is more richly valued than it used to be. From 2020 to 2024, the stock averaged a price-to-cash from operations (P/CFO) ratio below 8. Today, this ratio sits at 19.

Yet if we compare it to some of the most popular stocks in the food industry, Sprouts still looks relatively cheap.

Data by YCharts.

Despite growing sales at a similar rate over the last decade -- and with Sprouts offering by far the most store-count expansion potential of the group -- it remains the cheapest option. Simply put, Sprouts Farmers Market looks like an outstanding winner to add to at a fair price following its recent dip.