The story of the stock market these days is arguably Palantir Technologies, which was the best-performing stock in the S&P 500 in 2024 and is looking to repeat that success this year. Palantir is capitalizing on the rise of artificial intelligence (AI) to bring AI-powered solutions to its government contracts, and is rapidly expanding in the commercial space as well.

While Palantir is a massive success story, it's not the only AI company working in the government space. BigBear.ai (BBAI 8.70%) is much smaller than Palantir and its stock is up 20% so far this year. However, BigBear.ai stock took a beating after the company's second-quarter earnings report and is down 28% in the last month.

Is BigBear.ai worth buying on the dip? Let's take a look.

Image source: Getty Images.

About BigBear.ai

Based in a Virginia suburb of Washington, D.C., BigBear.ai is geared heavily toward its federal government work. The company provides mission-ready AI solutions and services for defense and intelligence agencies.

The company has a $165 million contract with the U.S. Army to modernize and incorporate AI into its platforms, allowing commanders to make data-driven decisions for the training and mobilization of soldiers.

It is also involved in a number of smaller efforts, including a collaboration with Hardy Dynamics to help integrate machine learning and AI into military operations, and an enhanced passenger processing program using biometric software at international airports in Chicago, Los Angeles, New York, Denver, Dallas, and Charlotte, North Carolina.

NYSE: BBAI

Key Data Points

The company is looking to capitalize on the Trump administration's focus on using biometrics to support border control and an increased emphasis on using AI to guide military decision-making. Management sees a $70 billion opportunity from increased funding for U.S. Customs and Border Protection, and a $673 million opportunity from funding approved for biometric border controls.

And it's growing its international efforts, including new work with the United Arab Emirates for AI work across several sectors. The work is being done in conjunction with Easy Lease PJSC and Vigilix Technology Investment.

While these are all logical headwinds that support BigBear.ai's growth story, the company's recent earnings report raised some issues.

A disappointing report

While Palantir wowed the market by reporting quarterly revenue that topped $1 billion for the first time, BigBear.ai actually saw a revenue decrease in the second quarter. The company had sales of $32.5 million, down 18% on a year-over-year basis. It cited lower volume on some Army programs for the drop.

The company also posted a net loss of $228.6 million, a massive increase from its loss of $14.4 million in Q2 2024. BigBear.ai said the increase was due to non-cash changes in derivative liabilities of $135.8 million regarding 2029 warrants, and a non-cash goodwill impairment of $70.6 million.

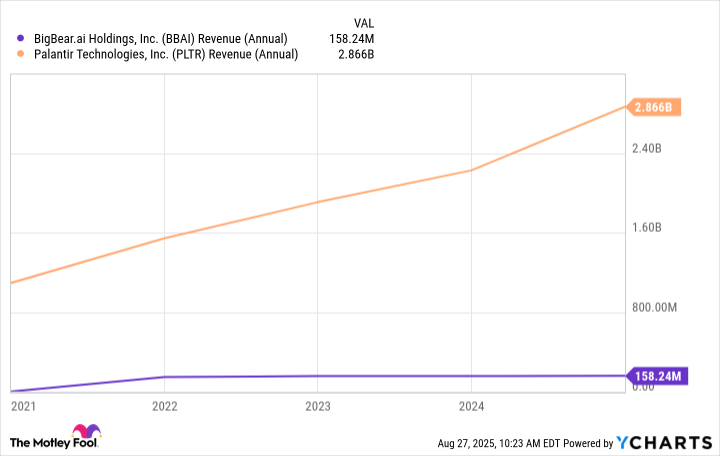

In addition, BigBear.ai withdrew its adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) guidance, citing uncertainty about Army programs and anticipated growth investment spending in the second half of the year. That's a huge red flag for investors, particularly when you consider that Palantir saw 48% revenue growth in the second quarter. While Palantir's revenue is taking off like a rocket, BigBear.ai is staying relatively flat.

BBAI Revenue (Annual) data by YCharts

The bottom line

If you're comparing Palantir and BigBear.ai, the one place where BigBear comes out ahead is the valuation. Palantir's price-to-sales ratio is an astounding 117, while BigBear.ai comes in at just over 9. The biggest argument against Palantir has been its valuation -- but it's also hard to overlook Palantir's massive growth.

That's why it makes sense for investors to hedge their bets against Palantir by looking at other AI companies that have government contracts. But I am deeply skeptical of BigBear.ai at this point because it's not showing that it has enough contracts to be viable. While Palantir closed 157 deals valued at more than $1 million in the second quarter alone, BigBear.ai is overly dependent on its large Army contract -- and doesn't have the ability to adjust should the dollars from that one deal stop flowing.

That's why I'm not buying BigBear.ai stock on this dip.