Recursion Pharmaceuticals (RXRX 2.17%), a biotech company focused on artificial intelligence (AI), went public in April 2021. This was before ChatGPT, before AI became the hottest topic on Wall Street, and before the technology caused some companies' profits to soar. One might think that Recursion would have benefited from the rapid expansion and adoption of AI technology, but that hasn't exactly been the case, to say the least.

Let's discuss Recursion Pharmaceuticals' performance over the past four years and whether the company can deliver solid returns in the future.

NASDAQ: RXRX

Key Data Points

It's been a southbound ride

It can take about 10 years (plus or minus a few) for a brand-new clinical compound to go from the early stages of discovery to the market, and those are just the ones that make it that far. Many are abandoned at some point after they fail to prove safe or effective in clinical studies.

The entire process requires hundreds of millions of dollars -- sometimes more -- which is invested in running clinical trials (and associated costs), as well as complying with legal requirements and submitting regulatory applications. Furthermore, the costs of developing drugs have increased over the past few decades, despite substantial technological advances.

Image source: Getty Images.

Recursion Pharmaceuticals wants to change that approach, and the company is betting that AI can be a significant help. Recursion's AI-powered operating system is constantly testing compounds against a library of human genes to predict which is most likely to perform well in clinical trials and, eventually, earn approval.

This strategy could help reduce costs and expedite the development time of medicines. Everyone would benefit from it: Patients would receive potentially life-saving drugs faster and at lower prices, while biotech companies would be able to decrease expenses and costs, thereby boosting their profits and margins.

That said, Recursion doesn't have a single therapy on the market yet. Over the past four years, the company has made little notable clinical progress. Like most clinical-stage biotechs, Recursion Pharmaceuticals generates little revenue (it does receive some from collaboration agreements) and consistently reports losses.

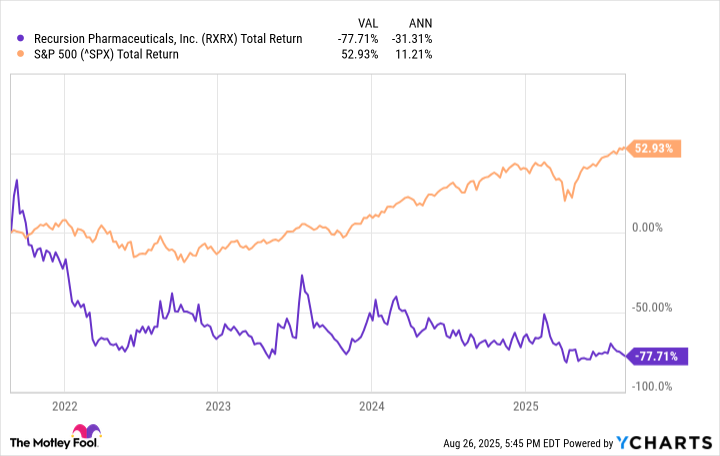

Add that to broader market issues, such as various economic troubles that have impacted equities over the past few years, and the result is that Recursion Pharmaceuticals has significantly lagged the market since 2021. Given the company's annual return of negative 31.3%, $1,000 invested in Recursion Pharmaceuticals four years ago would be worth $222.63 today. By investing the same amount in an ETF that tracks the S&P 500 index's performance, an investor would have approximately $1,529.59 today.

RXRX Total Return Level data by YCharts

Is there a rebound in the cards?

Recursion Pharmaceuticals partnered with Nvidia to build the largest supercomputer in the pharmaceutical industry to support its ambitions. The company's research agreements with several giants of the sector, including Roche and Bayer, prove that these well-established drugmakers see some promise in its approach. These partnerships will also help the company with funding, which can be a significant problem for smaller biotechs.

Further, the U.S. Food and Drug Administration announced earlier this year that it would gradually phase out animal testing in favor of other methods, including AI-powered approaches, which is precisely what Recursion Pharmaceuticals already does. One of the goals that regulators cited for the change was an effort to reduce R&D expenses for drugmakers, which they could eventually pass on to consumers in the form of lower drug prices.

All that is to say that Recursion may very well be onto something. Even so, until the biotech actually earns approval for a medicine -- or at least gets a product or two to late-stage studies -- the market will remain highly skeptical. The stock could soar if it proves that its approach is successful by launching medicines at a fraction of the cost of its competitors.

However, Recursion Pharmaceuticals is a risky play, and failure to make clinical and regulatory progress could further sink the stock price. Only investors with a large tolerance for volatility should consider initiating a position in the company. Others should steer clear.