The special purpose acquisition company (SPAC) era led to the hype and eventual fall of hundreds of different startups that entered the public markets through reverse mergers. From 2020 through the end of 2022, over 1,000 new stocks went public, with most severely underperforming the indices. In 2025, a few are starting to mount a comeback.

Enter Archer Aviation (ACHR +0.47%). An electric air taxi innovator that aims to alleviate traffic in major cities, its stock has gone from under $2 in 2023 to $9.15 today, but still trades below its $10 SPAC merger price. Does that mean you can buy shares of this disruptive company and make it rich? Let's look closer at the numbers and find out.

A person walks on the tarmac in front of an Archer Aviation Midnight model eVTOL aircraft. Image source: Archer Aviation.

Defeating traffic with flying taxis?

Automotive traffic is a major pain for everyday life in many cities around the world, and Archer Aviation aims to be the solution to this problem. How? Through its electric vertical takeoff and landing (eVTOL) product called the Midnight. It is a helicopter-like vehicle powered by electric batteries that can transport up to four passengers and their luggage through the air from point-to-point landing spots in cities. Unlike a helicopter, it is much quieter and can operate over residential neighborhoods with minimal disturbances, at least in theory.

Working with partners such as United Airlines and governments like the United Arab Emirates, Archer Aviation is planning to build point-to-point air taxi networks in cities like New York. Most routes will cut down an hour-long drive in traffic to a 10-15 minute journey in a flying vehicle. As more and more taxi routes are utilized, Archer Aviation believes it will unclog the traffic jams and bring about a huge benefit to society. From a business perspective, this hopefully means a large potential market of paying customers for these journeys.

NYSE: ACHR

Key Data Points

The problem remains in getting certification from the Federal Aviation Administration (FAA). Only partially approved as of today, Archer Aviation hopes that the Midnight will get final approval to deploy for flights sometime next year, although it is unclear how likely this scenario is.

Large upfront manufacturing spend

Since it cannot sell any aircraft to customers, Archer Aviation is currently generating zero dollars in revenue. It has many orders with aviation customers -- $6 billion as of last year -- but it cannot fill any of them until it gets the full approval from the FAA.

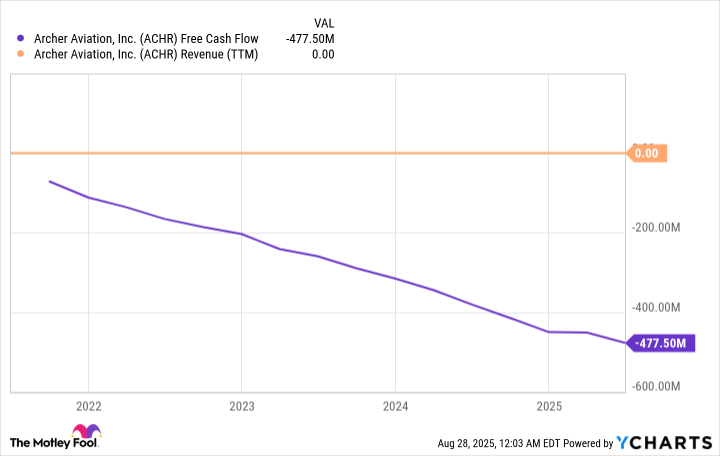

In the meantime, Archer Aviation is ramping up its manufacturing capabilities to start pumping out Midnight aircraft. The goal is to produce 50 vehicles a year in the near future. Building these vehicles has become a costly endeavor, especially when you consider the novelty of this type of aircraft. Over the last 12 months, Archer Aviation has burned $447.5 million in free cash flow, a figure that has only gotten worse the longer it has stayed public.

Management has raised a lot of money to give it a $1.7 billion liquidity position, but this is a company aggressively burning cash to scale up manufacturing. It may need to raise more funds during this decade if this burn rate gets worse.

Data by YCharts.

A perplexing stock to value

Investors have turned from bullish to bearish and now back to bullish on Archer Aviation stock. It currently trades at a market cap of $5.9 billion, which is a hefty valuation for a company that has never generated a lick of revenue.

A stock is worth what it will generate in future earnings. When looking at Archer Aviation, there is a lot of potential to grow the number of Midnight aircraft sold around the world every year if the electric air taxi technology can take off. At an estimated cost of $5 million per vehicle, 50 vehicles sold a year will get the company to $250 million in revenue. And 200 sold will get it to $1 billion, which is not an unreasonable scenario within a decade.

The problem comes with the low profitability of aircraft manufacturing. It is unlikely that Archer Aviation will generate a net income margin much greater than 10%, given how costly it is to maintain manufacturing, certifications, and quality control. A 10% margin on $1 billion in revenue is $100 million in future net earnings that may materialize sometime within the next 10 years.

Compared to a market cap of $5.9 billion, $100 million in earnings is a price-to-earnings ratio (P/E) of 59. What this means is that even in the most optimistic growth and profitability scenario, Archer Aviation will still be trading at a premium P/E ratio. That should make the stock one for investors to avoid, even if it is getting a lot of hype today.