2025 is more than halfway over, but numerous stocks remain poised for strong growth to close out the year. These are the companies I believe investors should focus on buying, and I predict they will close out the year on a strong note.

Two stocks that I think will have a solid end to the year are Nvidia (NVDA +2.03%) and Alphabet (GOOG +0.04%) (GOOGL +0.21%). Each stock has a different reason why the end of 2025 could be a boost for it, but it all circles back to one thing: artificial intelligence (AI).

Image source: Getty Images.

1. Nvidia

Nvidia has been the top stock to invest in during the AI arms race, as it has essentially acted as the weapons dealer in this arms race. Nvidia makes graphics processing units (GPUs), which are the most powerful general-purpose computing devices available on the market. Nvidia has sold millions of GPUs bound for use in AI-focused data centers, and that doesn't appear to be slowing down anytime soon.

NASDAQ: NVDA

Key Data Points

In Q2 FY 2026 (ending July 27), it grew revenue at a 56% pace despite being unable to sell its products in China. As the final details of this arrangement between the U.S. government and Nvidia are finalized, it could provide a growth catalyst that emerges at the end of the year and into 2026. This could provide a huge boost for the stock, as Nvidia projected about $8 billion in H20 sales for Q2 if it was allowed to sell to that market.

Regardless, domestic AI demand remains robust. As we approach 2026, we can expect to hear more from AI hyperscalers about their infrastructure buildout plans, which are likely to increase from the levels seen in 2025. This bodes well for Nvidia, and I think it could cause the stock to rise as we near 2026.

2. Alphabet

Alphabet is one of these AI hype-scalers that's spending a boatload of money on AI capacity. It has multiple reasons for doing so, and all make sense. First, it's a cloud computing provider, which allows clients to rent computing power from Google Cloud. As demand for AI processing power continues to grow, it is necessary to continue purchasing Nvidia GPUs and other computing devices to meet the increasing demand.

NASDAQ: GOOGL

Key Data Points

Google Cloud is only a small part of Alphabet's business; the much larger segment is Google Search, which accounts for over half of Alphabet's revenue. Some investors fear that Google Search will lose market share to generative AI, and there is some anecdotal evidence that this is already occurring. However, a large portion of the global population hasn't made this switch, and with Google integrating AI search overviews, it's bridging the gap between traditional search and a generative AI experience. This requires a ton of computing power, which further bodes well for a company like Nvidia.

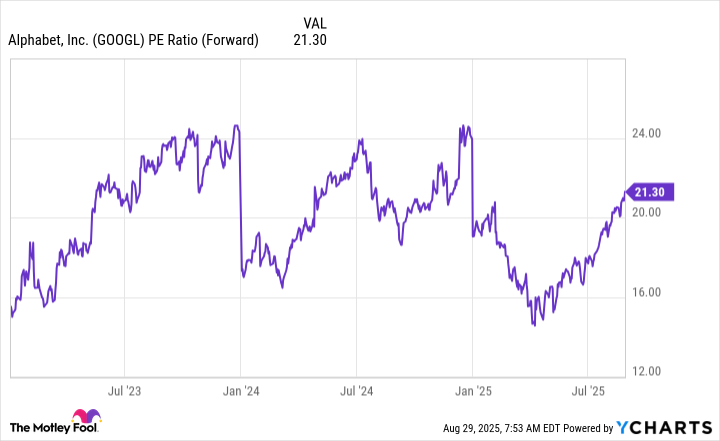

Regardless, Alphabet is still growing at a rapid pace, with revenue rising 14% in Q2 and diluted earnings per share increasing at a 22% pace. Despite those strong growth figures, Alphabet's stock trades at a relatively low price-to-earnings ratio of 21.3 times forward earnings.

GOOGL PE Ratio (Forward) data by YCharts

Compared to the S&P 500 (^GSPC +0.64%), which trades for 23.7 times forward earnings, Alphabet's stock appears fairly cheap. Furthermore, compared to its big-tech peers that trade with a forward P/E multiple between the high 20s and the low 30s, Alphabet is quite undervalued.

Alphabet has had a strong few months, but this strength could continue throughout the rest of 2025 as it plays catch-up to achieve a premium valuation that it deserves for its strong execution. This could lead to strong performance to close out 2026, making it a smart buy now.