Oracle (ORCL 3.70%) stock delivered solid returns over the past year thanks to the healthy growth that enjoys on account of the fast-growing demand for its cloud artificial intelligence (AI) infrastructure. However, the past month has difficult for shareholders.

Shares of the cloud infrastructure provider dropped by nearly 10% in the last month. However, Oracle could put the market's negativity to rest on September 9 when it releases its fiscal 2026 first-quarter earnings report. There is a solid chance that Oracle could cruise past Wall Street's expectations and deliver better-than-expected guidance.

Image source: Getty Images

A massive revenue pipeline that's growing at an incredible pace

AI has turned out to be a game-changer for Oracle of late. Traditionally known for providing database management systems for enterprises, Oracle now benefits from the booming demand for new cloud infrastructure that can be used to train and deploy AI models and applications.

NYSE: ORCL

Key Data Points

The company's growth is expected to accelerate in the current fiscal year, and customers have been queuing up to use Oracle's infrastructure-as-a-service (IaaS) at a remarkable rate. Oracle is expecting its total cloud revenue growth rate to increase by 16 percentage points in fiscal 2026 to 40%.

More importantly, management forecasts that its remaining performance obligations (RPO) will jump by more than 100%. That's a big deal considering that in fiscal 2025 Q4, its RPO rose by 41% to $138 billion. RPO is the total value of the contracts that a company signed but has yet to fulfill at the end of a period.

Considering that Oracle expects its revenue to jump by at least 17% in fiscal 2026 to $67 billion, the projected growth in the company's RPO means that it is on track to land more contracts that it can immediately fulfill. Importantly, Oracle is ensuring that it can quickly bring on more data center capacity to meet the incredible demand that it is witnessing.

Its capital expenditures tripled in fiscal 2025 to just over $21.2 billion. Oracle is expecting its capital expenditures to hit at least $25 billion in the current fiscal year, but don't be surprised to see it spend even more, considering its recent contract wins. For instance, OpenAI recently signed a deal with Oracle to build more data center capacity, and this partnership is expected to generate $30 billion in annual revenue for the latter company.

As a result, there is a good chance that Oracle's cloud infrastructure revenue growth could exceed the 70% jump that management has forecast for fiscal 2026, which would already be a nice improvement over the 51% growth it recorded last year. Also, higher capacity will allow Oracle to book more business, as the company is either having to say no to some new customer demand or else defer that demand until the point that it has enough capacity.

So, if Oracle indeed decides to expand its data center capacity at a more aggressive pace, it could meet more client demand and deliver stronger-than-expected results in September. Also, don't be surprised if Oracle raises its guidance based on its swelling order book and capacity investments. These developments can help lift the cloud computing giant's stock out of its recent rut.

The recent dip opened a solid long-term opportunity for investors

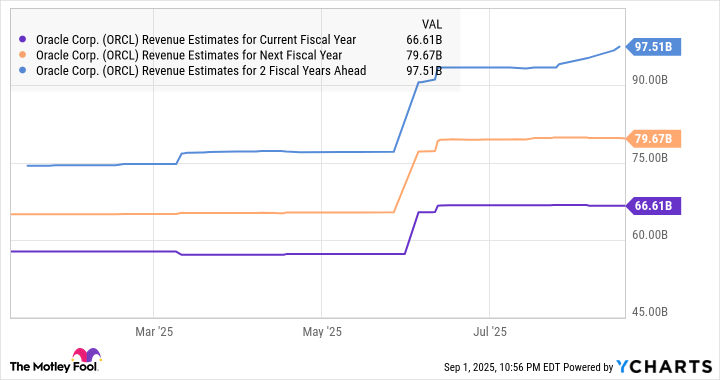

The phenomenal growth that's expected in Oracle's revenue pipeline this year explains why its top-line growth is projected to accelerate.

ORCL Revenue Estimates for Current Fiscal Year data by YCharts.

It won't be surprising to see Oracle maintaining its terrific growth beyond the next three years. A study by the analysts at Research and Markets forecasts that the global cloud computing market will grow by more than 350% over the next decade thanks to the proliferation of AI, generating a whopping $3.5 trillion in revenue in 2035. Oracle's fast-growing global data center network and its multicloud partnerships with the likes of Amazon, Google, and Microsoft put it in a terrific position to benefit from this tremendous opportunity.

As such, investors looking for a long-term winner should consider buying Oracle following its recent slide. A solid set of quarterly results this month could supercharge the stock once again, and we have already seen that the company is capable of sustaining its momentum in the coming years, thanks to the lucrative AI opportunity that it can benefit from.