After a sleepy 2024, industrial stocks have been on a tear this year. The Industrial Select Sector SPDR exchange-traded fund (ETF) is up over 15%. At that rate, it's outpacing the S&P 500's gain of about 10%, making it one of highest sector performers in 2025.

Why are industrials performing so well? Couple of reasons. First, artificial intelligence (AI) infrastructure spending is booming. Data centers need industrial products, like turbines, HVAC systems, and transformers, that only industrial companies can make at scale.

Second, aerospace and defense stocks are having one of their best years. Global defense budgets have been surging, with demand for civil and defense aviation outpacing supply. Throw in major infrastructure investments on the federal level -- like the Infrastructure Investment and Jobs Act (IIJA) -- and industrials are clearly propped up by all sorts of tailwinds.

That doesn't mean every industrial stock is a win. Industrials tend to be cyclical, and one must be careful not to buy when a company's earnings are about to peak. As I scan the landscape of industrial companies, these two stick out as opportunities now.

Joby Aviation

Joby Aviation (JOBY 4.20%) has been one of the top-performing industrial stocks in 2025. Indeed, as of this writing (Sept. 1), share prices have climbed almost 75% year to date, which tops the S&P 500 by a long shot, as well as the -6.5% year-to-date loss of its rival Archer Aviation.

Image source: Joby Aviation.

Joby is a pioneer in the electric vertical take-off and landing (eVTOL) industry. Its production prototype is the S4, an all-electric aircraft that can hold four passengers and fly up to about 150 miles before it needs a new charge. The S4 is quieter than a helicopter, produces no emissions, and could help alleviate one of the peskiest problems in urban transportation: gridlocked traffic along congested roads.

The total addressable market (TAM) for urban air mobility is expected to be about $9 trillion in 2050, according to analysts at Morgan Stanley. Joby is currently worth about $12 billion. If it can capture a portion of that market, the growth opportunity could be staggering.

NYSE: JOBY

Key Data Points

But let's not get too enthusiastic here. The reality is that Joby isn't making meaningful revenue -- yet. Last quarter, it brought in about $15,000, essentially none, and incurred a net loss of $325 million. It still hasn't passed the regulatory hurdles imposed by the Federal Aviation Administration (FAA), which means its cash position -- about $991 million at the end of the second quarter -- is something investors should watch closely.

At the same time, Joby is making progress. In mid-August 2025, Joby flew an eVTOL craft successfully between two U.S. public airports in Marina and Monterey, California. It's also about 70% finished on its side of stage four FAA-type certification. And finally it completed its acquisition of Blade Air Mobility, which offers it a network of terminals in key markets like New York.

Again, nothing is fixed, and Joby still has a long way to go before it's taxiing customers between vertiports. But for growth stock investors who can stomach volatility, a $100 investment in this eVTOL stock could go a long way down the road.

Caterpillar

You've probably seen a Caterpillar (CAT 3.36%) machine at some point in your life. Big yellow claw digging holes or flattening dirt for roads. It's a household name -- a brand on T-shirts and kids' toys -- yet that's not the reason why it's worth a $100 investment today.

That reason has to do with artificial intelligence (AI). Although Caterpillar is best known for its industrial and mining equipment, it also makes equipment for power generation and backup power generators, both of which are critical for data centers to run 24/7. As the AI revolution makes data centers indispensable, demand for reliable power systems is expected to escalate, which could whip up a multi-year tailwind for Caterpillar to ride.

NYSE: CAT

Key Data Points

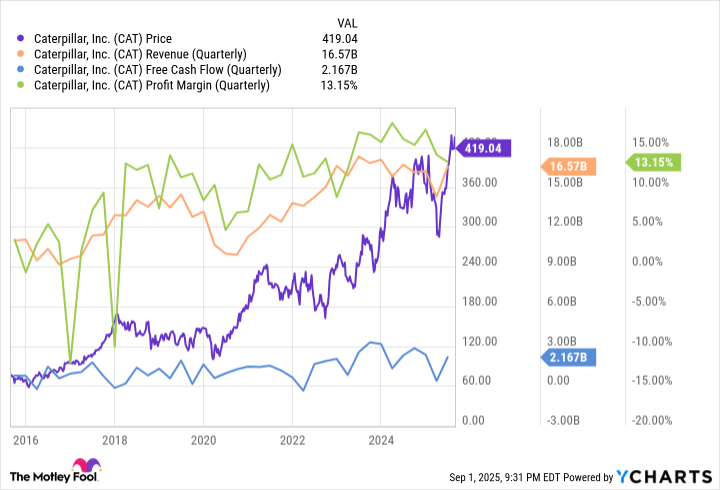

The company has already seen growth from this trend. Its Q2 earnings report showed sales from its Energy & Transportation segment up 7% year over year, the only segment to post higher sales. Those sales netted about $7.8 billion, outpacing Construction ($6.2 billion) and Resource Industries ($3.1 billion).

Headwinds for Caterpillar, however, are strong. The company now expects to lose between $1.5 to $1.8 billion this year to tariff-related expenses, while stiff competition with other heavy industrial makers, like Komatsu and Deere & Co, has added pressure to its margins. Both of these headwinds are in addition to the company's normal cyclicality, which means its revenue and cash flow can swing wildly with economic cycles, as the chart below illustrates.

Still, this 100-year-old company has weathered its fair share of catastrophic events, from the Great Depression to the Great Recession. With its industrial leadership and new growth from AI spending, Caterpillar offers a rare blend of stability and upside right now.