Bill Holdings (BILL 1.86%) offers an expanding portfolio of software products designed to help small businesses streamline their bookkeeping and accounting processes. The company went public in 2019 at $22 per share, and by mid-2021, it had soared by an eye-popping 1,400% to a peak of $335.

Investors rewarded Bill's stratospheric revenue growth back then, even though the company was losing truckloads of money. But the economic environment shifted in 2022 when the global economy slowed due to soaring inflation and rising interest rates, so Bill decided to build a more sustainable business by sacrificing some of its hypergrowth in favor of improving its bottom line.

Investors weren't so keen on the idea, and Bill stock is now trading 85% below its 2021 record high. However, could the sharp drop be the ultimate long-term buying opportunity? Here's what Wall Street thinks.

Image source: Getty Images.

Helping small businesses save time and money

Small business owners are time poor because they wear so many hats. They have to be product experts, sales people, marketers, and bookkeepers, among many other roles. Legacy accounts receivable, accounts payable, and budgeting processes that require paper invoices and clunky payment systems are inconvenient, and often result in lost time and money. Bill is solving that problem.

The company developed a cloud-based digital inbox where businesses can receive invoices directly, and also upload paper-based invoices. From there, the platform automatically forwards them to the right person for approval, who can pay them with a single click. Bill also makes the accounts receivable process a breeze by enabling businesses to rapidly generate invoices, send them to customers, and track incoming payments.

Around 493,000 businesses were using Bill's various software solutions at the end of fiscal 2025 (which concluded on June 30). The company acquires customers both directly and also through a network of more than 9,000 accounting firms that recommend its software to their clients. Since Bill's products make the accounting process much easier, it's a win for all parties.

Bill just delivered its first profitable year since going public

Bill generated a record $1.46 billion in total revenue during fiscal 2025, which was a 13% increase from the previous year. That growth rate has trended lower over the last few years, as the company shifts its priority toward improving its bottom line, which involves carefully managing costs.

Spending less aggressively on things like marketing can slow the pace of customer acquisition, and in turn reduce the number of opportunities to capture more revenue.

On that note, Bill increased its operating expenses by just 3% during fiscal 2025, to $1.27 billion. But since the company's increase in revenue outweighed its increase in costs, it managed to deliver a net income of $23.8 million on a generally accepted accounting principles (GAAP) basis. It was Bill's first annual GAAP profit since it went public in 2019.

If Bill starts to deliver consistent annual profits, it will give management the flexibility to redirect more resources back into growth initiatives like marketing and research and development. Therefore, while it's possible the company's revenue growth continues to decelerate for the next year or so, there is definitely potential for a reacceleration in the future.

Wall Street is bullish on Bill stock

The Wall Street Journal tracks 27 analysts who cover Bill stock, and 14 have given it a buy rating. One other analyst is in the overweight (bullish) camp, while the remaining 12 recommend holding. None of the analysts recommend selling.

Their average price target for the stock is $58.39, which implies a relatively modest potential upside of 13% over the next 12 to 18 months. However, the Street-high target of $89 suggests the stock could soar by 72% instead.

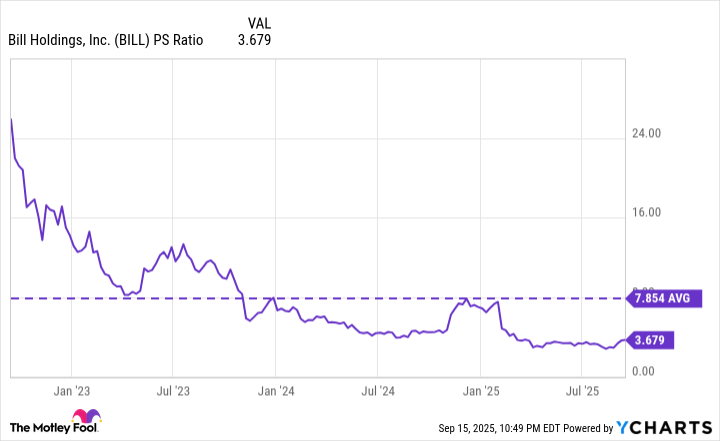

Bill stock looks cheap right now, so the Street-high target might be realistic. It's trading at a price-to-sales (P/S) ratio of just 3.7, which is a 52% discount to its three-year average of 7.8 (this excludes data from the exuberant 2021 period):

BILL PS Ratio data by YCharts

Bill generates most of its revenue by taking fees when businesses process payments through its platform. The company processed $345 billion in payment volume during fiscal 2025, but that's a drop in the bucket considering a whopping $135 trillion flows between businesses worldwide every year. That means there is still a very long runway for growth, so investors might do well to follow Wall Street's lead and add Bill stock to their portfolio for the long term.