Many businesses have come a long way in terms of practicing conscious capitalism, but the truth is, a primary goal of publicly traded companies is to create value for their shareholders. And quarterly dividends are one of the most transparent ways that a company can return some of that value to them.

If dividend yield were the only metric that investors used to judge them by, Ford Motor Company (F 0.83%) would easily best its crosstown rival General Motors (GM 1.09%), as the former boasts a lucrative 5%-plus yield while GM's sits at a much more modest 1%.

However, that's really only half of the equation, and by the time you finish reading this, you'll understand that General Motors actually returns far more value to shareholders.

Image source: Ford Motor Company.

Give Ford its due

Let's start off on the right foot. Ford deserves a lot of credit for its dividend. The company has stood firm on its commitment to return 40% to 50% of its adjusted free cash flow to shareholders, and paid out roughly $3 billion in total dividends last year -- not too shabby.

It gets even better because Ford also often returns extra value to shareholders via supplemental dividends. For example, in 2025, the company will return $0.60 per share for the year in regular dividends, split into $0.15 quarterly payments, but it also dished out a supplemental $0.15 per share dividend in the first quarter.

NYSE: F

Key Data Points

Taking it one step further, Ford's dividend is a bit more secure for shareholders because the Ford family still owns a large portion of a special class of shares that come with special voting rights, but that also receive the standard dividend. The Ford family received roughly $55 million in dividends last year by controlling roughly 2% of shares that come with 40% of the company's voting rights.

This level of control on their part means that when it comes to dividend policy, leadership's interests will be aligned with shareholders' interests for the most part, and that's a good thing.

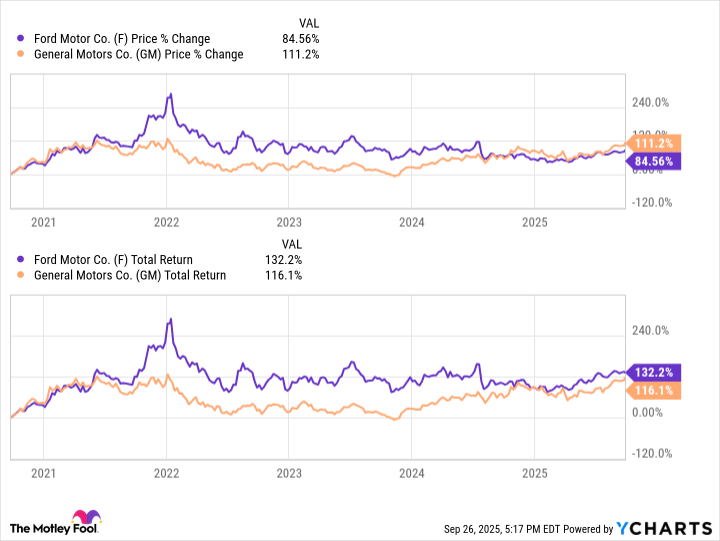

Now, let's consider two other points: the share price performance of Ford and GM, and then their total returns.

The difference is simple. General Motors' share price did increase more than Ford's; yet, on a total return basis -- including the value of their respective dividends -- the folks at the Blue Oval in fact returned more value to shareholders.

But if we're only judging these two heavyweight automakers by the value returned via dividends and share price gains, we're still doing General Motors a major disservice. This is where total yield comes into play.

What's total yield?

While dividend yield is a term thrown around constantly, total yield is often less heard of, but it's a useful metric, and investors would do well to become familiar with it. Total yield takes into account the impact of share buybacks, also known as share repurchases. To calculate the buyback yield, simply take the dollar amount spent on repurchasing shares and divide it by the existing market capitalization of a company.

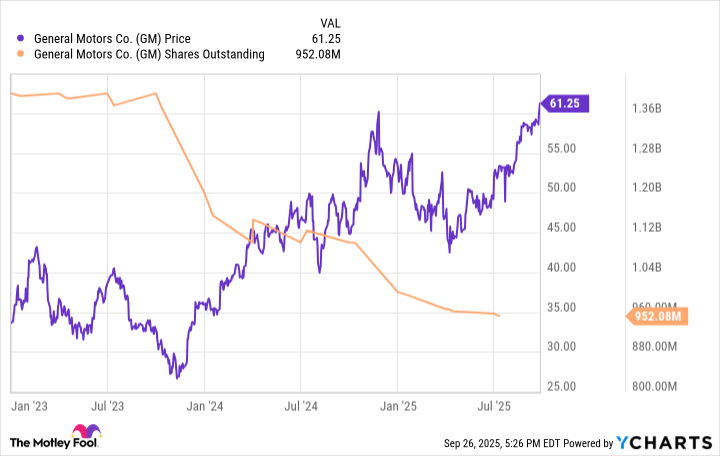

In the simplest of examples, if a company purchased $50 million worth of its stock, and its market cap was $500 million, its buyback yield would be 10%. This is big news for GM investors because the company has spent more than $16 billion buying back shares in recent years, and you can see the dramatic reduction that made in the number of outstanding shares, which in turn helped drive the share price higher.

When you take GM's share buybacks into account using total yield, which again combines the impact of both dividends and share buybacks, the picture looks entirely different. Ford boasts a 5.1% dividend yield, but only buys back small quantities of its shares annually, making its total yield a still respectable 6.85%. GM, on the other hand, distributes a dividend that yields a more modest 1%, but factor in its massive share buybacks and the automaker's total yield skyrockets to 14.29%.

What it all means

Investors arguing over the preference between dividends and share buybacks is a rivalry as old as time, and as fierce as any sports, or other, rivalry you can dream up. Both methods have their pros and cons, and both are intended to return value to shareholders.

All too often, when investors think about Ford and General Motors returning value to shareholders, they limit themselves to thinking about Ford's lucrative dividend -- but now you know the other half of the equation.

Remember to use total yield as an investment metric when applicable, tell your friends about it, and make the world smarter, happier, and richer -- and stay Foolish.