Centrus Energy (LEU +8.74%) offers investors something rare: A pure play on the supply side of U.S. nuclear power.

As one of two U.S. suppliers licensed to produce low-enriched uranium (LEU), and one of one to produce high-assay low-enriched uranium (HALEU), the nuclear energy stock appears ideally positioned to profit from Washington's push to obtain nuclear independence.

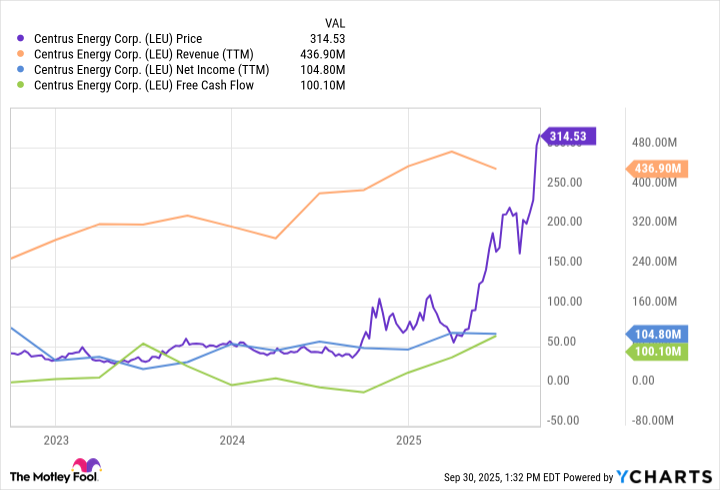

At the time of writing, Centrus stock is up an eye-watering 323% on the year and over 470% year over year. But whether this is a no-brainer growth stock depends on how well this company executes on its promises and how long favorable policy winds continue in its sails.

Image source: Getty Images.

What exactly does Centrus do?

Centrus, at its core, is a nuclear fuel supplier. Simply put, it provides LEU -- the standard fuel used in today's nuclear reactors -- through long-term purchase agreements.

Centrus' enrichment capacity is small but growing. In late 2023, it fired up operations at the American Centrifuge Plant in Piketon, Ohio, the first U.S.-owned enrichment plant to start production since 1954.

That same plant is currently the only U.S. facility licensed to produce HALEU, a special kind of nuclear fuel that's needed for next-generation reactors.

Until recently, production of HALEU on a commercial scale was done outside the U.S. (think: Russia). But with the Biden administration's former push for emission-free power, and the Trump administration's push for national security, production of HALEU on U.S. soil has become an urgent matter.

NYSE: LEU

Key Data Points

On that note, Centrus has a contract with the U.S. Department of Energy (DOE) to produce high-assay low-enriched uranium (HALEU). In mid-June, it delivered 900 kilograms of HALEU to the DOE, the second delivery of that fuel in two years. It's now entered phase III, which calls for another 900 kilograms of HALEU through June 30, 2026.

A growth story that may have already hit its climax

Like other nuclear energy stocks, Centrus comes with an asterisk. And that asterisk is its valuation.

Between mid-2024 and mid-2025, Centrus' market cap ballooned from about $684 million to more than $5.5 billion, an eightfold increase driven mostly by policy tailwinds and its delivery of HALEU to the DOE. In the same period, Centrus' net income decreased slightly from $30.6 million to $28.9 million even as gross profit increased to $53.9 million from $36.5 million.

I'm OK with Centrus' financial situation, as it has a solid balance sheet and positive cash flow. The kicker, however, is how other valuation metrics have exploded with today's $5.5 billion market cap.

At today's price, the stock trades almost 50 times trailing earnings and 77 times forward earnings. This points to an expectation of explosive near-term growth. With Centrus operating only one enrichment facility right now -- and at a limited production capacity at that -- it could take a half decade before revenue growth catches up to these numbers.

Centrus' growth also depends in part on the rollout of next-generation nuclear reactors, several of which are designed to run on HALEU. Many of these designs are still in development -- many don't even have regulatory approval yet -- and could take a few years before they move from blueprint to commercial plant.

That's not to suggest that Centrus isn't going to be a key player in a future market of HALEU fuel. But this market is still very much more future than present. A lot can happen between now and then, like a new administration, for instance, with a different energy agenda.

Because of that, Centrus is not a no-brainer for growth. It's a speculative play that requires thought and planning. For growth investors who can stomach the risk, the long-term payoff could be worth the volatility. Otherwise, a nuclear energy exchange-traded fund (ETF) could be a less risky venture.