If you're an income investor, or just a fan of highly valuable dividend-paying stocks, and are looking for a couple of companies with a 3%+ dividend yield, upside in their businesses, and brands you can trust, you're in the right place. Here are two excellent options that provide potential investors just that.

Image source: Getty Images.

Improving margins will fuel dividend

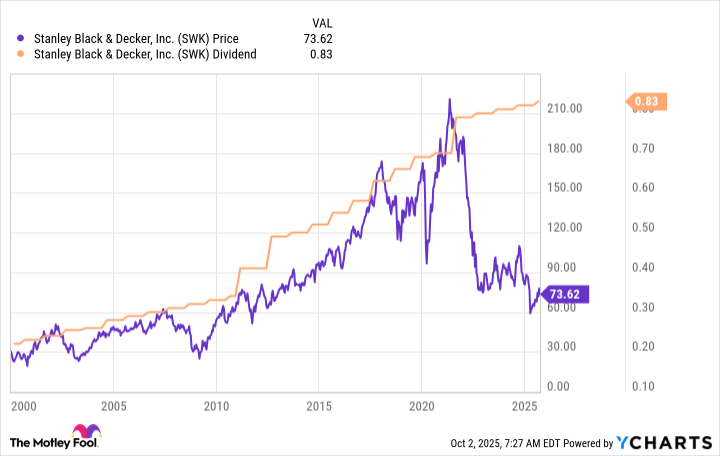

Stanley Black & Decker (SWK -1.42%) is a worldwide leader in Tools and Outdoor products that include power tools, hand tools, storage, digital jobsite solutions, and outdoor lifestyle products. The company operates manufacturing facilities across the globe and boasts impressive brands such as DEWALT, CRAFTSMAN, BLACK+DECKER, and STANLEY, among others.

One of the bright spots for owning shares of the power tools producer is its dividend. Over the summer, its Board of Directors approved a modest $0.01 increase of its quarterly cash dividend to $0.83 per common share, or a dividend-yield of 4.5%. It also extends the company's record for the longest consecutive annual and quarterly dividend payments among industrial companies listed on the New York Stock Exchange.

The good news is that for investors banking on not only its high-dividend yield, but its also potential, the company's current focus will improve margins. This should eventually trickle down into an increased dividend.

Stanley Black & Decker's former President and CEO, Donald Allan, Jr., said in a press release, "Supporting our long-standing cash dividend is a key element of our overall shareholder value proposition. This signals our confidence that we are building a Company and culture geared to deliver long-term organic growth and margin expansion as well as generate significant free cash flow to enhance shareholder return."

One way management is supporting dividends is through a series of initiatives expected to generate $2 billion of pre-tax run-rate cost savings by the end of 2025. The long-term adjusted gross margin target is an enticing 35%+. Since the beginning of the program in mid-2022, it's generated roughly $1.8 billion in pre-tax run-rate cost savings already.

Multiple routes to expansion

Bath & Body Works (BBWI 2.11%) is a specialty home fragrance and fragrant body care retailer operating with the brands Bath & Body Works, C.O. Bigelow, and White Barn. Not only does the specialty retailer offer a respectable dividend yield of 3.1%, there is immense growth potential for the company and its investors through store upgrades, digital opportunities, international expansion, as well as adjacent categories such as hair, lip, and laundry.

There is plenty of upside remaining in BBW's business that should power its top line well beyond its 2024 $7.3 billion level. The specialty retailer has a compelling product pipeline that should not only drive sales higher but reach new consumers. BBW could add low-hanging fruit business with expansion products that include shaving and facial care, but it could enter nascent categories such as haircare and men's care.

Beyond its potential production line expansion, the company has ample opportunity outside of its core U.S. market. In fact, for fiscal 2024, the company generated a vast majority of its sales from North America with only a paltry 5% of sales coming from international markets -- something the company plans to change.

The company already touches markets from Dubai, to Italy, all the way back to Mexico, and it just celebrated the opening of its 500th international store in London just last year, marking a stepping stone in the company's global growth strategy. In fact, Morningstar forecasts average sales growth of 3% from its North American stores, 3% from its digital e-commerce, and 5% from its international expansion.

Are they buys today?

Investors looking for rock-solid dividend stocks that also have upside potential in their business can certainly add Stanley Black & Decker and Bath & Body Works to their watchlists. Stanley Black & Decker has a lengthy history of delivering dividends and dividend increases, while it is also working to boost its bottom line through cost-cutting initiatives.

Meanwhile, Bath & Body Works may lack the dividend history of Black & Decker, it doesn't lack for opportunities. Not only does the company have nascent categories that make perfect sense under its umbrella of brands, it has immense untapped market potential globally -- both should power the company's business moving forward.