Taiwan Semiconductor (TSM +0.38%) has had an excellent 2025 so far, up nearly 50% this year. However, I still think the stock has more room to run through the end of this year and into 2026.

I've got three reasons why Taiwan Semiconductor's stock is an excellent buy, and investors would be wise to take action now and scoop up shares before the rest of the market does.

Image source: Getty Images.

1. Increasing chip demand

One of Taiwan Semiconductor's largest clients is Nvidia. Taiwan Semiconductor manufactures chips for its clients because they don't have the ability to do it themselves. So, when a client like Nvidia talks about massive growth, it will benefit TSMC.

During Nvidia's Q2 conference call, Nvidia's management noted that they expect global data center capital expenditures to rise from $600 billion in 2025 to $3 trillion to $4 trillion by 2030. That's monster growth, and if it pans out, it translates into massive growth for Taiwan Semiconductor.

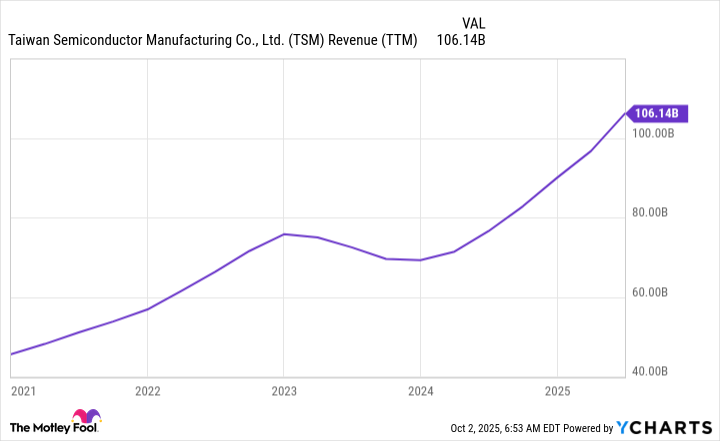

TSM Revenue (TTM) data by YCharts

That's not the only trend that's benefiting Taiwan Semiconductor.

If you look at other promising technologies, like autonomous driving, quantum computing, and humanoid robots, all of those technologies require advanced chips, which are likely sourced from Taiwan Semiconductor.

An investment in Taiwan Semiconductor is a bet that we're going to use more advanced chips in greater quantities, which seems like a no-brainer prediction to me. As a result, Taiwan Semiconductor appears to be a genius buy based on demand alone.

2. Taiwan Semiconductor is investing a ton of money in its U.S. facilities

Taiwan Semiconductor is also expanding outside of its base island to stand up facilities in multiple other countries, including the U.S. While some may point to U.S. tariff policies as the reason, investors should be cheering on this expansion. One of the biggest risks in investing in Taiwan Semiconductor is the fear of a mainland China takeover. This would sink the stock price, but if Taiwan Semiconductor had facilities in other parts of the world, it would soften the blow.

Taiwan Semiconductor has invested $165 billion in new chip facilities in the U.S., and that could be just the beginning if the company finds out that it hasn't built out enough capacity to satisfy U.S. demand. At its existing U.S. facility, Taiwan Semiconductor had reportedly sold out chip capacity through 2027, so there's clear demand for U.S.-produced chips.

Increased U.S. production is a good thing for U.S. companies and Taiwan Semiconductor alike, and I think it makes it a compelling stock to invest in.

3. Taiwan Semiconductor is always innovating

One of the reasons why Taiwan Semiconductor has become the top chip foundry is its culture of continuous improvement and innovation. Although TSMC has leading 3nm (nanometer) chip nodes, it's developing more advanced ones with impressive feature sets. This year, Taiwan Semiconductor is slated to launch its 2nm chip.

NYSE: TSM

Key Data Points

This chip node has an impressive improvement: When configured to run at the same speed as a 3nm chip, it will consume 25% to 30% less power. With how big of a deal data center energy consumption is becoming, this innovation will drive clients to upgrade their chip technology to realize energy savings. Taiwan Semiconductor isn't stopping there, either. Next year, it plans to release its A16 chip node, which will provide a 15% to 20% power consumption improvement over the new 2nm node.

Taiwan Semiconductor's commitment to always developing the most advanced technology possible and not resting on its laurels is one of the reasons it has become the most popular semiconductor foundry to partner with. I think this also makes it a strong buy, as advanced chips will cost more than their predecessors, boosting Taiwan Semi's revenue and profits along the way.