PepsiCo (PEP 0.17%) has been stuck for a while. Its overall sales have been pretty lackluster, with soda volumes slipping and its snacks losing share in its key North American market. Meanwhile, its push into healthier offerings has not yet been able to offset weakness in its core brands.

However, the company could have a nice opportunity ahead with one of the newest trends in soft drinks: "dirty soda."

NASDAQ: PEP

Key Data Points

Dirty soda on the rise

Dirty soda is a pretty simple concept that hearkens back to the days of soda fountains and malt shops. You start with a regular soda, like Pepsi or Mountain Dew, then add cream or flavored syrup or sometimes both. A Utah chain called Swig introduced the term back in 2010 and built a strong following.

The concept went viral through TikTok videos, helping expand the trend way beyond Utah. Swig now has more than 140 shops and its same-store sales have been climbing. Meanwhile, big players like McDonald's and Taco Bell, owned by Yum! Brands, are starting to test their own versions, which shows this is no longer just a regional fad but something that can scale across the country.

Meanwhile, PepsiCo has started to lean into the idea because it already owns some of the soda brands that make the whole thing work. At a convenience-store trade show in Chicago later this month, PepsiCo will debut two new dirty-soda-inspired drinks, Dirty Dew and Mug Floats Vanilla Howler, which follow the Pepsi Wild Cherry & Cream flavor that's already been one of the fastest-growing in its portfolio.

Soda volumes in the U.S. peaked roughly 20 years ago and have been on the decline for much of the last decade, as younger consumers have turned more to energy drinks, coffee, and flavored water. However, soda sales have started to tick higher in the past two years, partly because of dirty soda and prebiotic sodas. Pepsi acquired prebiotic soda brand Poppi in May, and then introduced a prebiotic version of its namesake cola a few months later to try to capitalize on that trend.

CEO Ramon Laguarta has said that innovation in beverages is a key part of PepsiCo's turnaround plan, and the company expects sales growth to improve over the next few quarters as these new products hit shelves while broader cost-cutting efforts gain traction.

PepsiCo has been shutting down underused plants, investing in its enterprise resource planning (ERP) system and artificial intelligence (AI) to improve productivity, and looking for savings in procurement so it can free up cash to put back into product innovation. That's the kind of discipline it needs to get operating margins up and still have room to grow.

The snack business still needs attention as well. Lay's and Tostitos are being relaunched with a focus on real ingredients and cleaner labels. The "permissible snack" portfolio, built around PopCorners and SunChips, has already grown past $2 billion and gives PepsiCo a platform to win back share. If snacks stabilize and beverages get a lift from momentum in dirty soda, that could help drive more meaningful growth.

The away-from-home channel is another piece that management keeps highlighting because it's accretive to gross margin and gives PepsiCo more room to innovate. Dirty soda works perfectly in this setting, since restaurants can easily make it with what they already have on hand. Dirty soda is a cheap but fun treat for customers who don't mind paying a little more for something different, but aren't looking to pay coffeehouse prices.

Image source: Getty Images.

Time to buy PepsiCo stock?

Pepsi hasn't been an exciting stock for a while because growth slowed and costs crept up, but along with prebiotic sodas and healthier snacks, dirty soda could be a catalyst that gets the company growing again. The stock also currently offers an attractive 4% dividend yield, which is just about covered by its free cash flow.

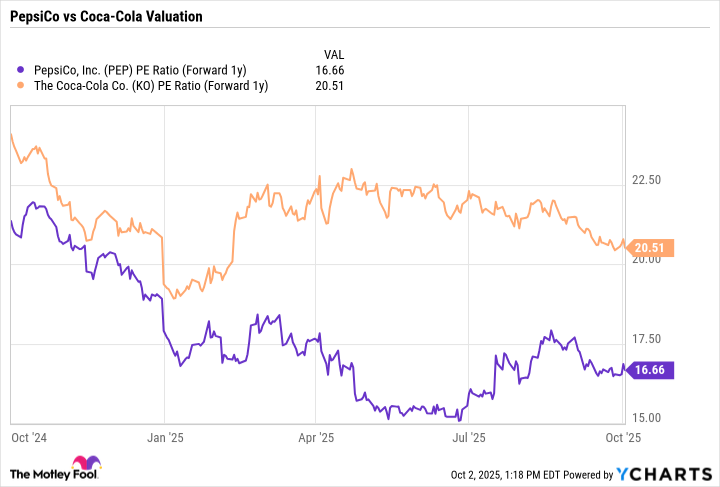

However, now that the heavy spending on its new ERP system is complete, its elevated capital expenditures (capex) will come down, and its coverage ratio will improve. That's a nice setup for a stock that trades at a considerable discount to rival Coca-Cola based on their forward price-to-earnings (P/E) ratios:

PEP PE Ratio (Forward 1y) data by YCharts.

PepsiCo's turnaround still hinges on execution in snacks and on getting costs down, but the trends in dirty soda and new innovations around it should start to help drive growth. With investors getting paid a 4% yield waiting for a turnaround, I think the stock is a buy.