Shares of retailer Target (TGT -1.39%) have tanked over the past year, falling nearly 42% in just 12 months. At the same time, the company's primary rival, Walmart (WMT -1.15%), has seen its shares steadily rise.

This might actually be an opportunity for contrarian investors to add Target to their portfolios while Wall Street is hyperfocused on consumers trading down to lower-priced retailers. The next big move could, ironically, be an upturn for Target's more "premium" approach.

Here are three reasons to consider buying Target like there's no tomorrow.

1. Target is out of step, but taking action

There's no question that Target is underperforming Walmart right now. All you need to do is look at each company's income statement to see that. For example, Target's sales fell 0.9% in the second quarter of 2025 while Walmart's U.S. business saw a sales gain of 4.8% in the comparable period. Same-store sales at Target declined 1.9% while Walmart's same-store sales in the U.S. rose 4.6%.

Image source: Getty Images.

But Target isn't sitting around and hoping for the best. The board of directors has switched in a new CEO, and a team has been installed to revamp the company's operating approach. There are some early signs that performance is improving, too. Sales fell an even worse 3.8% in the first quarter, with a 5.7% drop in same-store sales. One quarter of improvement doesn't make a trend, but it hints that all is not lost, even though Wall Street's negativity is extreme, given Target's huge stock price decline.

2. Target has lived through tough times before

The fact that Target's business performance is, perhaps, turning higher again is important. But the really notable thing is that the retailer has increased its dividend annually for more than five decades, making it a Dividend King, just like Walmart. A company can't build a streak like that without going through some rough patches, which is doubly true given the fickle nature of consumers in the retail sector.

But the divergent performances of Target and Walmart highlight an important difference between the two retailers. Walmart is keyed in on offering "everyday low prices" while Target attempts to provide a more upscale feel with its stores and the products it offers. Right now, consumers appear to be trading down to lower-price options, which happens from time to time. But when consumer sentiment improves, it is likely that they will trade back up again, likely returning to Target.

In the meantime, Target's new management approach is likely to work on highlighting the value proposition it offers to lure customers back sooner rather than later. There's really nothing new about any of this; Target has successfully navigated such customer mood swings before. Long-term investors should probably give the company the benefit of the doubt here.

3. Target looks rather cheap right now

Target is out of step with consumers right now, but it sees the problem and is addressing it. And it has a long history of successfully dealing with swings like this one. Those are both great reasons to buy the stock, but the linchpin is that Target's share price decline has the stock's valuation looking attractively cheap.

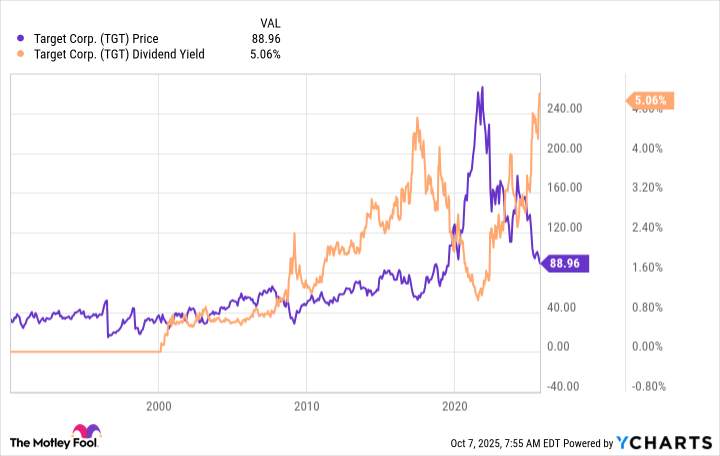

Using a non-traditional valuation metric, Target's dividend yield is near the highest levels in the company's history. That not only means that buying the stock will leave you collecting a huge 5.1% yield, but it also hints that the stock has been placed on the deep discount rack. Buying Dividend Kings while they have historically high yields involves some risk, but it can help you build yourself a reliable long-term income portfolio on the cheap.

The value opportunity here is backed up by more traditional valuation metrics like the price-to-sales and price-to-earnings ratios. Both are below their five-year averages today. And the difference between the average and the current ratio isn't small, either. For example, Target's P/S ratio is currently around 0.4 times versus a five-year average of nearly 0.7, which is a discount from the average of around 40%.

Target is probably worth the risk for long-term dividend investors

There's no question that Target's business isn't resonating with consumers today. But that's just kind of how the retail sector works. This Dividend King has survived periods in which it was out of favor before, while continuing to reward investors with a reliable and growing income stream. And given the lofty yield and low valuation, if you think in decades and not days, today could be a good time to think about adding this iconic retailer to your dividend portfolio.