Krispy Kreme (DNUT +0.23%) hasn't been a great stock to own this year. It's down more than 70% from its 52-week high of $12.68, which it reached last November. Since then, it's been in a persistent downward spiral as its lackluster results haven't given investors much of a reason to invest in the business.

The company, however, still has a well-recognized brand, and it's a popular option for consumers who are buying doughnuts or coffee. Could the rapid decline in its share price make for a great buying opportunity for long-term investors, or is Krispy Kreme's stock likely heading lower?

Image source: Getty Images.

What's wrong with Krispy Kreme stock?

Krispy Kreme's business centers around its famous doughnuts, and, while they are iconic, they also don't make for healthy eating options. And whether it's due to weight loss drugs rising in popularity (which can curb appetites) or simply part of longer-term trends focusing on healthier eating, demand hasn't been terribly strong for Krispy Kreme of late.

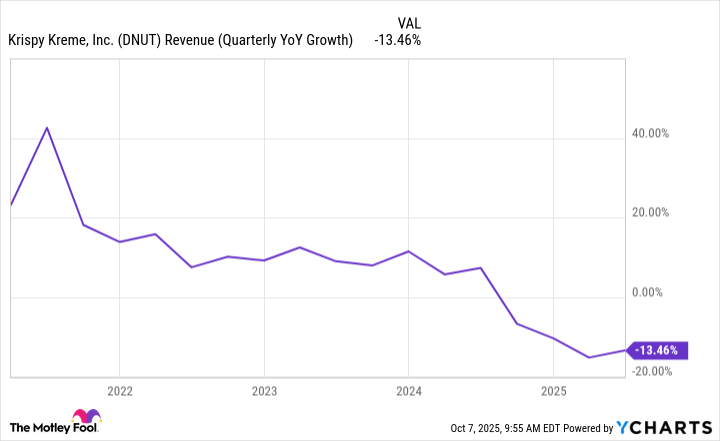

DNUT Revenue (Quarterly YoY Growth) data by YCharts

The company's growth took off after the pandemic, but it has been declining in recent years. And last quarter (which ended on June 29), its sales were down a staggering 13%. However, management said the large double-digit decline was largely a result of selling its stake in Insomnia Cookies. But even with that excluded, the company's organic revenue declined by 0.8%, indicating that there are still some growth-related concerns around the business moving forward.

Is the stock as risky as its discounted multiples suggest?

When investors are concerned about a company's future, they may not be willing to buy its stock unless it's trading at a discount. Krispy Kreme falls into that category as it currently trades at just 0.4 times its trailing revenue, and at around 0.9 times book value.

Since the company frequently incurs losses, there's no price-to-earnings multiple to base its valuation on, which is a red flag for investors, because if the business is struggling with profitability, then Krispy Kreme may not be much of a company worth investing in today. Not only are sales down, but it's not even able to turn a profit. In each of the past four quarters, Krispy Kreme has incurred an operating loss. Plus, over the past four quarters, it has burned through over $23 million in cash from its day-to-day operating activities.

Krispy Kreme's management knows the current situation needs improvement, and it's focused on a turnaround plan that aims to strengthen its margins and to get the business back to generating profitable growth. It is also looking to "reduce capital intensity" as it plans to have a leaner business model in the future.

NASDAQ: DNUT

Key Data Points

Krispy Kreme stock may be cheap, but it's not a bargain buy

Although Krispy Kreme stock has fallen significantly this year, its cheap price doesn't make for a compelling reason to invest in the business. It resembles more of a value trap at this stage than a solid investment option. A lot hinges on the success of its turnaround plan. It needs to be successful in showing that it can grow and do so profitably. It's not an easy task, which is why the food stock isn't taking off despite management's ambitious goals.

Krispy Kreme's stock could have the potential to soar if the turnaround produces improved financial results, but there's no way of knowing if that will indeed happen. The best option for investors may be to take a wait-and-see approach with the stock and to monitor what progress the business is making.

For now, however, there's not much of a reason to invest in the stock, and I wouldn't be surprised to see it go lower in the weeks and months ahead, as there's plenty of risk here.