Online ad-technology company The Trade Desk (TTD +4.22%) used to be a market darling. The company thrived in the coronavirus lockdown era, continued to win in the inflation panic of 2022, and soared in the relative normalcy of 2023 and 2024. The digital advertising market saw several upswings and downturns in this span, but The Trade Desk just kept growing its business.

As a result, the stock soared from $27 at the start of 2020 to $142 in December 2024. At the peak, it traded at lofty valuations such as 134 times free cash flow and 227 times earnings.

NASDAQ: TTD

Key Data Points

But the market turned against The Trade Desk in a heartbeat. One mildly disappointing revenue report later, the stock dipped 34% in a single week and then kept sliding. Today, The Trade Desk's stock stands 65% below the bittersweet ceiling it reached in December.

And I think it's an excellent stock to buy after that sudden price correction. Here's why I'm tempted to double down on my existing position.

Let's talk about what went wrong

First, I'll admit that The Trade Desk's challenges are real. Sales growth has slowed down in recent quarters (and should continue to decline in the next report) for two key reasons.

First, political marketing gave the ad industry a temporary boost in 2024 that isn't there this year. Comparing these distinctly different periods is like swimming with a weighted vest and heavy boots -- last year's full-year sales growth of 26% will retreat below 20% in 2025.

Second, a significant portion of The Trade Desk's sales come from a small group of very large customers. Recent case studies include household names like McDonald's, Pepsi, IKEA, and Disney. It's cool to have a strong stable of repeat customers, but there's a downside, too. These big names are also more vulnerable to the ongoing tariff uproar than smaller, more local companies. So, the tariff tension weighs very directly on large ad campaign budgets going through The Trade Desk's ad placement tools.

How The Trade Desk is fighting back

The company is taking resolute action to address the tariff-based challenges. If a robust competitor like The Trade Desk is struggling under these conditions, rival solutions are probably suffering even more. Hyper-targeted ad programs can still be effective in a difficult economy. Here's what CEO Jeff Green said in August's Q2 earnings call:

In volatile environments, these things have historically accelerated the move to programmatic precisely because it comes with control, agility, and performance. And when advertisers become more deliberate and performance-driven, programmatic is at its very best. That's the very best that we can offer to them, and that's when we're doing our best work for them. So because programmatic (which really is just a fancy word for fast-paced and data-driven) is measurable, it allows us to win share.

Image source: Getty Images.

Short-term flex meets long-term love

On top of this valuable programmatic ad placement focus, The Trade Desk is working out flexible short-term deals instead of multiyear contracts right now. It is also setting up joint business plans (JBPs) with clients willing to make long-term commitments. JBPs involve working closely with an important customer to define multiyear goals and strategies -- for a premium price. And the process of setting up a partnership like this usually results in a tighter commitment for the long haul.

I love this combo of flexible short-term pricing and more long-term relationships. It should support sales to price-sensitive customers while boosting the long-term value of deeper commitments.

"The number of live JBPs is at an all-time high, and we continue to see spend under JBPs significantly outpace the rest of our business," Green said.

Why I'm seeing dollar signs

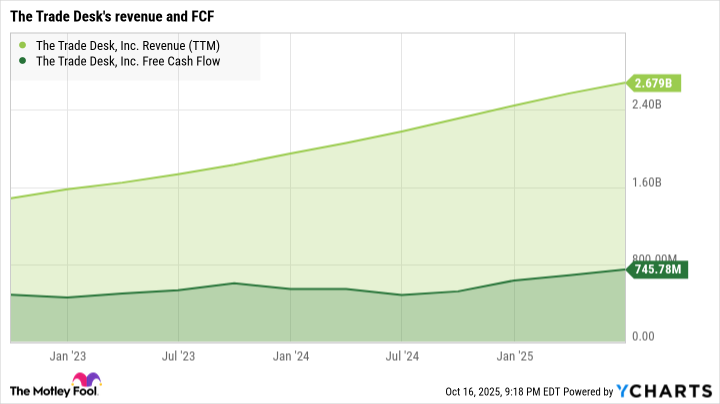

So, The Trade Desk's shares are changing hands near all-time-low valuation ratios. The company is generating massive cash profits, with $746 million of free cash flow over the last four quarters, based on $2.68 billion in top-line revenues.

And I really don't mind The Trade Desk's roughly 20% growth targets for 2025. Sure, it's a slowdown -- but from incredibly high levels, and the resulting pace is still impressive. Even in a weak market, The Trade Desk knows how to draw beautiful financial charts:

TTD Revenue (TTM) data by YCharts. TTM = trailing 12 months.

In my eyes, The Trade Desk remains a thrilling growth stock, and the stock is selling at a deep discount nowadays.