AGNC Investment (AGNC 0.71%) gets a lot of investor attention because of its shockingly high 14% dividend yield. To put that yield into perspective, the S&P 500 index (^GSPC 0.53%) is only yielding about 1.2%, and the average real estate investment trust (REIT) has a yield of 3.9%.

Yet the one group that probably shouldn't buy AGNC Investment is dividend investors. Here's what you need to know before you buy this ultra-high-yield mortgage REIT.

What does AGNC Investment do?

AGNC Investment buys mortgages that have been pooled together into bond-like securities. It generally attempts to enhance its returns by using leverage, which is usually backed by its portfolio of mortgage securities.

The value of the mortgage REIT is, basically, the value of its mortgage-security portfolio. The company provides that value every quarter via a metric called tangible net book value per share.

Image source: Getty Images.

This is an interesting fact because tangible net book value per share is similar to net asset value, which is what mutual funds report. In many ways, AGNC Investment is kind of like a mutual fund that invests in mortgage securities. That's vastly different from a traditional REIT, which owns and operates a portfolio of physical properties. This materially changes the story for investors.

AGNC Investment's goal, which it clearly states on its investor homepage, is "favorable long-term stockholder returns with a substantial yield component." Most REITs have the goal of providing reliable dividends, with REIT industry bellwether Realty Income stating its goal as being "committed to providing our shareholders with dependable monthly dividends." In other words, Realty Income is focused on generating income for investors, but AGNC Investment is focused on total return.

Total return versus dividends

Dividends are a piece of total return, but the total return calculation requires that dividends be reinvested. There's nothing wrong with reinvesting dividends, but many dividend investors are looking to live off of the dividends their portfolios generate.

If you do that, the dividends can't be reinvested and compound over time. This is the problem with AGNC Investment.

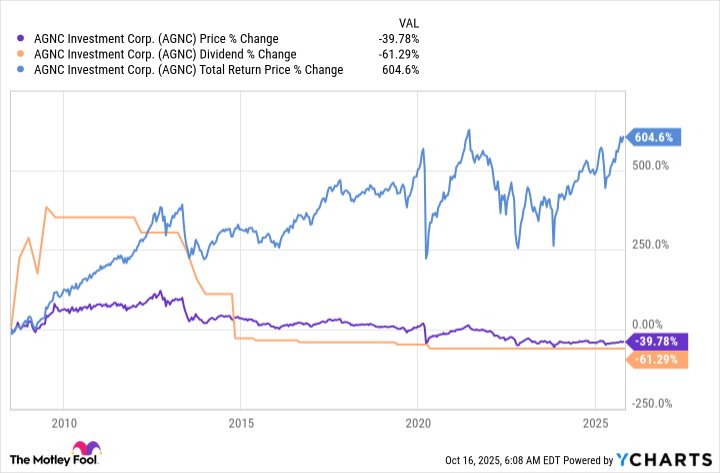

As the chart above highlights, AGNC Investment has done a good job of achieving its goal of providing total return. However, the dividend and the stock price have been highly volatile and fallen steadily over time.

If an investor didn't reinvest that huge dividend, they'd have ended up with less income and less capital. That's about the worst possible outcome for an investor trying to live off of dividends.

It's important to highlight that AGNC Investment isn't a bad company. The key distinction here is about which type of investor might want to own it.

If you're trying to find a reliable dividend stock, AGNC Investment probably won't work for you, even though it offers a massive 14% dividend yield. It's far more appropriate for investors who look at total return and could be a very good option for investors using an asset allocation approach.

Don't get lured in by the big yield

AGNC Investment is a complex dividend stock. While it's a REIT, a business structure meant to pass income on to shareholders in a tax-efficient manner, it's not a traditional REIT by any stretch of the imagination.

AGNC Investment is an example of why it's so important to understand the businesses you're buying. If you're trying to live off of your dividends, tread with extreme caution. History suggests that AGNC Investment's dividend could be a big letdown.